Nov 1, 2013 | ETFs, trading strategies

A lot of U.S investors have come to realize in recent years that there are many trading opportunities outside the USA. This creates something of a bad news, good news, bad news, good news situation.

-The bad news is that picking individual stocks is never an easy thing even if you focus only on domestic U.S. companies. For the average investor to successfully pick and choose among individual stocks around the globe is simply too much to expect.

-The good news is that the proliferation of international ETFs – Single country funds, regional funds, global funds, etc. – has made it much easier for investors to diversify across the globe than it used to be.

-The bad news is that the proliferation of ETFs has also reached a point where choosing an international ETF is getting to be almost as confusing as choosing a phone plan.

-The good news is that there are ways to simplify and systematize things.

So let’s take a look at “one way” to play the international stocks game.

BRIC vs. SPX

BRIC refers to an index comprised of stocks from Brazil, Russia, India and China. For the purposes of this article I will demonstrate a simple method for switching between BRIC and the S&P 500 Index.

The Vehicles:

For calculating switches I will use:

1) An index I created using AIQ TradingExpert. I refer to it as BRICINDX and it is comprised of single-country ETF tickers EWZ (Brazil), RSX (Russia), INP (India) and FXI (China).

Figure 1 – Jay’s BRICINDEX

2) Ticker SPX (i.e., the S&P 50 Index)

For actual trading purposes there are a few choices that I will discuss a little later.

The Method:

I will use a method I learned a long time ago from David Vomund, President of Vomund Investment Management, LLC and the author of “ETF Strategies Revealed.” The measure calculates the relative strength between two assets on a weekly basis. When the trend of relative strength reverses in a particular direction for two consecutive weeks it signals a switch into the stronger index.

The Test:

We start our test on 10/26/01 simple because that is the first time we can get a good reading using back data. Each week we look at the relative strength of my BRICINDX versus the S&P 500 Index (ticker SPX). If the RSMD rises for two consecutive weeks we want to switch into the BRICINDX and if the RSMD declines for two consecutive weeks we want to switch into the S&P 500 Index.

Figure 2 displays the switches over the past several years.

Figure 2 – BRICINDEX (vs. SPX; lower clip)

When an “Up” arrow occurs in Figure 2, the system switches into BRICINDX, when a “Down” arrow occurs in Figure 2 the system switches into ticker SPY. The results of this “System” are displayed in Figure 3. Note the two columns at the far right:

Switch: The growth of $1,000 using the system

Split: The growth of $1,000 split evenly between BRICINDX and SPY.

|

|

|

BRIC |

SPY |

Switch |

Split |

Switch |

Split |

| Date |

Date |

Index |

%+(-) |

%+(-) |

%+(-) |

%+(-) |

$1,000 |

$1,000 |

| 10/26/01 |

2/8/02 |

BRIC |

20.9 |

3.7 |

20.9 |

12.3 |

1,209 |

1,123 |

| 2/8/02 |

2/22/02 |

SPY |

13.9 |

0.0 |

0.0 |

7.0 |

1,209 |

1,201 |

| 2/22/02 |

5/10/02 |

BRIC |

(12.6) |

(3.2) |

(12.6) |

(7.9) |

1,057 |

1,106 |

| 5/10/02 |

7/19/02 |

SPY |

(25.0) |

(23.8) |

(23.8) |

(24.4) |

806 |

837 |

| 7/19/02 |

8/2/02 |

BRIC |

(14.1) |

1.9 |

(14.1) |

(6.1) |

692 |

786 |

| 8/2/02 |

11/1/02 |

SPY |

(0.8) |

8.8 |

8.8 |

4.0 |

753 |

817 |

| 11/1/02 |

6/27/03 |

BRIC |

45.0 |

7.1 |

45.0 |

26.0 |

1,091 |

1,030 |

| 6/27/03 |

8/29/03 |

SPY |

18.3 |

5.3 |

5.3 |

11.8 |

1,000 |

1,000 |

| 8/29/03 |

11/14/03 |

BRIC |

10.9 |

2.1 |

10.9 |

6.5 |

1,109 |

1,065 |

| 11/14/03 |

12/12/03 |

SPY |

11.9 |

2.5 |

2.5 |

7.2 |

1,137 |

1,142 |

| 12/12/03 |

1/23/04 |

BRIC |

16.4 |

7.7 |

16.4 |

12.1 |

1,324 |

1,280 |

| 1/23/04 |

7/2/04 |

SPY |

(18.5) |

(3.4) |

(3.4) |

(10.9) |

1,279 |

1,140 |

| 7/2/04 |

11/5/04 |

BRIC |

29.0 |

4.7 |

29.0 |

16.8 |

1,650 |

1,331 |

| 11/5/04 |

12/3/04 |

SPY |

9.0 |

1.8 |

1.8 |

5.4 |

1,679 |

1,403 |

| 12/3/04 |

12/31/04 |

BRIC |

(0.2) |

0.9 |

(0.2) |

0.3 |

1,675 |

1,408 |

| 12/31/04 |

2/11/05 |

SPY |

5.4 |

0.3 |

0.3 |

2.9 |

1,681 |

1,449 |

| 2/11/05 |

3/25/05 |

BRIC |

(4.3) |

(2.8) |

(4.3) |

(3.5) |

1,609 |

1,398 |

| 3/25/05 |

7/1/05 |

SPY |

8.1 |

2.7 |

2.7 |

5.4 |

1,653 |

1,473 |

| 7/1/05 |

10/21/05 |

BRIC |

13.9 |

(0.4) |

13.9 |

6.7 |

1,882 |

1,572 |

| 10/21/05 |

1/13/06 |

SPY |

18.3 |

7.6 |

7.6 |

12.9 |

2,024 |

1,776 |

| 1/13/06 |

3/17/06 |

BRIC |

9.6 |

1.6 |

9.6 |

5.6 |

2,219 |

1,876 |

| 3/17/06 |

4/28/06 |

SPY |

9.0 |

(0.0) |

(0.0) |

4.5 |

2,219 |

1,961 |

| 4/28/06 |

5/26/06 |

BRIC |

(13.5) |

(3.3) |

(13.5) |

(8.4) |

1,920 |

1,796 |

| 5/26/06 |

8/4/06 |

SPY |

9.2 |

1.5 |

1.5 |

5.4 |

1,948 |

1,892 |

| 8/4/06 |

9/1/06 |

BRIC |

2.1 |

2.9 |

2.1 |

2.5 |

1,988 |

1,939 |

| 9/1/06 |

10/20/06 |

SPY |

4.2 |

4.4 |

4.4 |

4.3 |

2,076 |

2,023 |

| 10/20/06 |

2/16/07 |

BRIC |

23.4 |

6.2 |

23.4 |

14.8 |

2,561 |

2,322 |

| 2/16/07 |

4/13/07 |

SPY |

5.2 |

0.5 |

0.5 |

2.8 |

2,573 |

2,387 |

| 4/13/07 |

8/17/07 |

BRIC |

5.0 |

(1.4) |

5.0 |

1.8 |

2,700 |

2,430 |

| 8/17/07 |

9/7/07 |

SPY |

11.2 |

0.8 |

0.8 |

6.0 |

2,722 |

2,576 |

| 9/7/07 |

12/21/07 |

BRIC |

35.8 |

2.4 |

35.8 |

19.1 |

3,696 |

3,067 |

| 12/21/07 |

4/25/08 |

SPY |

(9.3) |

(6.4) |

(6.4) |

(7.9) |

3,458 |

2,826 |

| 4/25/08 |

6/13/08 |

BRIC |

(3.0) |

(2.4) |

(3.0) |

(2.7) |

3,353 |

2,749 |

| 6/13/08 |

12/5/08 |

SPY |

(57.0) |

(35.5) |

(35.5) |

(46.2) |

2,164 |

1,478 |

| 12/5/08 |

6/26/09 |

BRIC |

53.1 |

5.4 |

53.1 |

29.3 |

3,314 |

1,911 |

| 6/26/09 |

10/2/09 |

SPY |

20.4 |

12.2 |

12.2 |

16.3 |

3,719 |

2,223 |

| 10/2/09 |

11/6/09 |

BRIC |

9.6 |

5.3 |

9.6 |

7.5 |

4,076 |

2,388 |

| 11/6/09 |

4/9/10 |

SPY |

5.6 |

9.3 |

9.3 |

7.5 |

4,454 |

2,567 |

| 4/9/10 |

4/23/10 |

BRIC |

(2.0) |

1.3 |

(2.0) |

(0.3) |

4,365 |

2,558 |

| 4/23/10 |

6/18/10 |

SPY |

(6.2) |

(8.2) |

(8.2) |

(7.2) |

4,008 |

2,374 |

| 6/18/10 |

11/19/10 |

BRIC |

11.7 |

7.9 |

11.7 |

9.8 |

4,475 |

2,606 |

| 11/19/10 |

3/11/11 |

SPY |

(0.1) |

8.2 |

8.2 |

4.0 |

4,843 |

2,712 |

| 3/11/11 |

5/6/11 |

BRIC |

(0.4) |

3.6 |

(0.4) |

1.6 |

4,823 |

2,755 |

| 5/6/11 |

6/10/11 |

SPY |

(1.9) |

(5.2) |

(5.2) |

(3.6) |

4,571 |

2,656 |

| 6/10/11 |

7/15/11 |

BRIC |

(1.7) |

2.3 |

(1.7) |

0.3 |

4,494 |

2,664 |

| 7/15/11 |

11/4/11 |

SPY |

(11.7) |

(3.3) |

(3.3) |

(7.5) |

4,344 |

2,463 |

| 11/4/11 |

12/16/11 |

BRIC |

(15.3) |

(4.7) |

(15.3) |

(10.0) |

3,678 |

2,216 |

| 12/16/11 |

1/20/12 |

SPY |

16.0 |

9.4 |

9.4 |

12.7 |

4,024 |

2,497 |

| 1/20/12 |

3/23/12 |

BRIC |

2.4 |

7.6 |

2.4 |

5.0 |

4,121 |

2,623 |

| 3/23/12 |

7/6/12 |

SPY |

(15.3) |

(4.4) |

(4.4) |

(9.9) |

3,938 |

2,363 |

| 7/6/12 |

2/1/13 |

BRIC |

17.5 |

10.5 |

17.5 |

14.0 |

4,628 |

2,694 |

| 2/1/13 |

7/26/13 |

SPY |

(15.2) |

12.7 |

12.7 |

(1.3) |

5,216 |

2,660 |

| 7/26/13 |

|

BRIC |

13.1 |

4.4 |

13.1 |

8.8 |

5,900 |

2,893 |

Figure 3 – BRICINDX vs. SPY

Figure 4 displays the trade-by-trade result in graphical form.

Figure 4 – Jay’s BRIC/SPY System (blue line) versus Split/Buy-and-Hold

A Few Performance Notes

-An investor who had split $1,000 between BRICINDX and SPY in 2001 would now have $2,893, a gain of 189.3%

-An investor who had utilized this switching system starting with $1000 in 2001 would now have $5,900, a gain of 490%.

So you clearly see the potential long-term benefit.

-Long-term is the key phrase. While the system clearly outperformed over time, over any trade or series of trades there is no guarantee that that will be the case.

-One other thing to note is that this particular system is allows long the stock market, either foreign or domestic. This means that if there is a global bear market (such as 2008) this system will suffer. Therefore, aggressive investors might consider building in some sort of market timing in order to avoid some of the downside.

A Few Trading Notes

For actual trading purposes a trader can emulate my BRICINDEX by splitting money between the four ETFs that comprise the index. There are other, easier alternatives including:

-Ticker VWO: Vanguard Emerging Markets ETF does not track these four funds exactly but has a correlation of roughly 97% with the BRICINDX and enjoys active trading volume.

-Ticker BKF: iShares BRIC Index Fund is the fund most closely correlated to my BRICINDX, however, trading is very thin.

-Ticker DXELX: This is the Direxion 2x leveraged Emerging Markets open end mutual fund. The leverage creates more profit potential (with commensurate downside risk) and this is a good choice for someone who would rather trade a standard mutual fund than an ETF.

-Ticker EDC: I am leery of 3x leveraged ETFs, but someone looking to “go for the gusto”, -Direxion Emerging Markets 3x ETF offers a lot of upside potential (but also a great deal of downside risk)

Summary

The “system” I’ve detailed here isn’t necessarily something that you should rush out and start trading right this very minute. Still, it does illustrate a few things:

-It is possible to “beat the market” (in this case, the “market” is defined as a portfolio evenly split between foreign and domestic stock indexes) over time using a mechanical approach.

-It is possible to profit from global stock market trends without becoming an expert in Chinese stocks or Russian stocks (or whatever country’s stocks).

-Demonstrating the discipline to follow an objective approach to investing is one of the keys to long-term success.

All in all it’s just another, well, you can sing the rest of it yourself……

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://aiq.com) client

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Oct 30, 2013 | Uncategorized

They say that complacency is the enemy of the stock market. If so, the action of ticker VXX – the exchange-traded fund designed to track the VIX Index – may be of interest.

The indicator known as “Narrow Range 7”, or NR7 for short was first introduced by Toby Crabel some time back in the 1980’s or 1990’s. The theory is that when the difference between today’s high price and low price for a given security is the smallest it’s been over the past 7 trading days, that security is said to be “contracting” or “compressing.” The theory goes that – just as ying follows yang – once the compression is over there should be an “expansion”, – i.e., a meaningful price movement.

Now this is not always necessarily the case – i.e., a security can remain mired in a range for a good long while. In addition, a simple NR7 gives no indication on its own as to whether the ensuing price expansion will be to the upside or to the downside. Still, please note the chart in Figure 1. This extreme compression DOES NOT guarantee or even imply that the stock market is about to decline. But it sure does seem to signal a whole lot of complacency among investors.

Figure 1 – Ticker VXX has registered seven consecutive days of narrower and narrower ranges (Courtesy: AIQ TradingExpert)

In all candor I am not entirely sure what this means. My gut tells me that following the whole “shutdown/debt limit” crisis, and with QE2IB (Quantitative Easing to Infinity and Beyond) set to feed liquidity to the market until the end of time, it is pretty much assumed that the stock market has nowhere to go but higher.

Complicating this for me personally is that most of my indicators are bullish, so I am not inclined to pound the table and shout “the end is near!” (although it is kind of fun to see the looks on people’s faces when I do it just for fun.)

Still, it is not a stretch to think that we could be setting up for a nasty surprise in the near-term (i.e., sometime in the next several weeks) which would certainly surprise the heck out of most investors. People who are inclined to hedge might consider buying VXX December 13 strike price call options (as I write, it is $99 for a 1-lot, with the futures suggesting that stock indexes will open higher, i.e., that VXX will open lower).

Figure 2 – VXX December 13 call (Courtesy: ww.OptionsAnalysis.com)

Figure 3 – VXX December 13 Call (Courtesy: ww.OptionsAnalysis.com)

Summary

Everything – trend-following, seasonal, liquidity – seems to point to a bullish trend in the stock market. And I am not one to stand in the way. But historically when everything “looks good” for the stock market, one of two things happens: Either the stock market:

a) trends higher based on the bullish confluence of indicators, or,

b) the market surprises the daylights out of the majority with a nasty surprise.

$99 to insure against b seems like a reasonable price to pay.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://aiq.com) client

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Oct 30, 2013 | options, trading strategies, volatility

They say that complacency is the enemy of the stock market. If so, the action of ticker VXX – the exchange-traded fund designed to track the VIX Index – may be of interest.

The indicator known as “Narrow Range 7”, or NR7 for short was first introduced by Toby Crabel some time back in the 1980’s or 1990’s. The theory is that when the difference between today’s high price and low price for a given security is the smallest it’s been over the past 7 trading days, that security is said to be “contracting” or “compressing.” The theory goes that – just as ying follows yang – once the compression is over there should be an “expansion”, – i.e., a meaningful price movement.

Now this is not always necessarily the case – i.e., a security can remain mired in a range for a good long while. In addition, a simple NR7 gives no indication on its own as to whether the ensuing price expansion will be to the upside or to the downside. Still, please note the chart in Figure 1. This extreme compression DOES NOT guarantee or even imply that the stock market is about to decline. But it sure does seem to signal a whole lot of complacency among investors.

Figure 1 – Ticker VXX has registered seven consecutive days of narrower and narrower ranges (Courtesy: AIQ TradingExpert)

In all candor I am not entirely sure what this means. My gut tells me that following the whole “shutdown/debt limit” crisis, and with QE2IB (Quantitative Easing to Infinity and Beyond) set to feed liquidity to the market until the end of time, it is pretty much assumed that the stock market has nowhere to go but higher.

Complicating this for me personally is that most of my indicators are bullish, so I am not inclined to pound the table and shout “the end is near!” (although it is kind of fun to see the looks on people’s faces when I do it just for fun.)

Still, it is not a stretch to think that we could be setting up for a nasty surprise in the near-term (i.e., sometime in the next several weeks) which would certainly surprise the heck out of most investors. People who are inclined to hedge might consider buying VXX December 13 strike price call options (as I write, it is $99 for a 1-lot, with the futures suggesting that stock indexes will open higher, i.e., that VXX will open lower).

Figure 2 – VXX December 13 call (Courtesy: ww.OptionsAnalysis.com)

Figure 3 – VXX December 13 Call (Courtesy: ww.OptionsAnalysis.com)

Summary

Everything – trend-following, seasonal, liquidity – seems to point to a bullish trend in the stock market. And I am not one to stand in the way. But historically when everything “looks good” for the stock market, one of two things happens: Either the stock market:

a) trends higher based on the bullish confluence of indicators, or,

b) the market surprises the daylights out of the majority with a nasty surprise.

$99 to insure against b seems like a reasonable price to pay.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://aiq.com) client

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Oct 25, 2013 | Uncategorized

I am a fan of “simple” strategies. For the record, yes, I have multiplied the standard deviation of the regression line times the implied volatility of the 90+ day options in order to, in order to, um, well, I seem to recall that there was a really important reason why I did it at the time. Or so it seemed. Still, I am reminded of:

Jay’s Trading Maxim #316: When it comes to analyzing markets and indicators, multiplying (or dividing) two numbers just “because you can”, is not necessarily helpful.

So again, I generally try to keep things simple. Which is great, because the idea in this piece is something I first discovered in the 1990’s, and “trading systems” (such as it is, in this case) don’t get much simpler. So here goes.

When to Own Retailing Stocks

The “system” I discovered in the 1990’s for retailing stocks works like this:

-Buy and hold retailing stocks during the months of February, March, October and November.

That’s it.

As with most things in life there is some good news and some bad news. Let’s start with the bad news. Like a lot of things, this “system” got crushed during the 2008 meltdown, suffering a -48% drawdown.

For those of you who are about to stop reading because of that last figure, just let me say DO NOT STOP READING!

The good news is that despite being fully invested in retailing stocks during the worst meltdown in modern history, the system has since soared to much higher new highs and has outperformed a buy and hold approach by 40% (+791% for the system vs. +562% for buy and hold) since December 1989.

What this means in a nutshell is that if you held retailing stocks only during all eight of the other months every year since 1990, you would actually have lost about -26%. This dichotomy of performance would not seem evident from a cursory glance at Figure 1.

Figure 1 – FSRPX Monthly Bar Chart (Courtesy AIQ TradingExpert)

Figure 2 displays the growth of $1,000 invested in Fidelity Select Retailing fund (ticker FRSPX) only during the months of February, March, October and November, starting in December 1989.

Figure 2 – Growth of $1,000 invested in FSRPX during “bullish” four months (since December 1989)

Again, the good news and bad news is fairly obvious. For the most part the system was a model of equity growth consistency – OK, except of course for the 2007-2008 “Express Elevator to Hell” period. Still, it is instructive to consider what would have happened had you simply skipped these four month every year and invested in retailing stocks only during all of the other eight months of the year. These results appear in Figure 3.

Figure 3 – Growth of $1,000 invested in FSRPX during all other months (since December 1989)

Figure 4 displays the performance of FSRPX during the four “favorable” months (i.e., the “system”) versus the performance of FSRPX during all other months (i.e., the “Anti System”) on an annual basis. The results are fairly striking

Figure 4 – Systems results versus “Anti System” Results

Figure 5 – Systems results versus “Anti System” Results

A few things to note:

-The System has showed a gain 21 out of 24 years.

-The Anti System showed a gain in only 11 years.

-The System outperformed the Anti System 75% of the time.

-The System showed a net gain of +794%.

-The Anti System showed a net loss of -30%.

Summary

Obviously during some years retailing stocks will rally outside of our four “favorable” months (for example, this year). But the long-term results suggest that investors would do well to focus on retailing stocks during February, March, October and November.

A Note for Option Traders

One less expensive way to make this play is to buy a deep-in-the-money call option on ticker XRT (SPDR Retail ETF). Here is an example:

-On 9/30/2013 a trader could have purchased 400 shares of XRT at $82.01 a share. The cost of this trade would be $32,804. The net delta of this position is 400.

-An option trader could have bought 5 December XRT 76 call option at $6.90. The cost of this trade would be $3,450. This option has a delta of 81.29, so buying 5 contracts yields a net delta of 401.26. In other words, this position will behave just like the stock position, but at a fraction of the cost ($3,450 versus $32,804).

Figure 6 –XRT December 76 call option as a replacement for stock shares (Courtesy: www.OptionsAnalysis.com)

Figure 6 –XRT December 76 call option as a replacement for stock shares (Courtesy: www.OptionsAnalysis.com)

As this is written:

-400 XRT shares are up 2% on an investment of $32,804 since 9/30.

-5 XRT December 76 calls options are up 13% on an investment of $3,450 since 9/30.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://aiq.com) client

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Oct 25, 2013 | retail stocks, Seasonality, trading strategies

I am a fan of “simple” strategies. For the record, yes, I have multiplied the standard deviation of the regression line times the implied volatility of the 90+ day options in order to, in order to, um, well, I seem to recall that there was a really important reason why I did it at the time. Or so it seemed. Still, I am reminded of:

Jay’s Trading Maxim #316: When it comes to analyzing markets and indicators, multiplying (or dividing) two numbers just “because you can”, is not necessarily helpful.

So again, I generally try to keep things simple. Which is great, because the idea in this piece is something I first discovered in the 1990’s, and “trading systems” (such as it is, in this case) don’t get much simpler. So here goes.

When to Own Retailing Stocks

The “system” I discovered in the 1990’s for retailing stocks works like this:

-Buy and hold retailing stocks during the months of February, March, October and November.

That’s it.

As with most things in life there is some good news and some bad news. Let’s start with the bad news. Like a lot of things, this “system” got crushed during the 2008 meltdown, suffering a -48% drawdown.

For those of you who are about to stop reading because of that last figure, just let me say DO NOT STOP READING!

The good news is that despite being fully invested in retailing stocks during the worst meltdown in modern history, the system has since soared to much higher new highs and has outperformed a buy and hold approach by 40% (+791% for the system vs. +562% for buy and hold) since December 1989.

What this means in a nutshell is that if you held retailing stocks only during all eight of the other months every year since 1990, you would actually have lost about -26%. This dichotomy of performance would not seem evident from a cursory glance at Figure 1.

Figure 1 – FSRPX Monthly Bar Chart (Courtesy AIQ TradingExpert)

Figure 2 displays the growth of $1,000 invested in Fidelity Select Retailing fund (ticker FRSPX) only during the months of February, March, October and November, starting in December 1989.

Figure 2 – Growth of $1,000 invested in FSRPX during “bullish” four months (since December 1989)

Again, the good news and bad news is fairly obvious. For the most part the system was a model of equity growth consistency – OK, except of course for the 2007-2008 “Express Elevator to Hell” period. Still, it is instructive to consider what would have happened had you simply skipped these four month every year and invested in retailing stocks only during all of the other eight months of the year. These results appear in Figure 3.

Figure 3 – Growth of $1,000 invested in FSRPX during all other months (since December 1989)

Figure 4 displays the performance of FSRPX during the four “favorable” months (i.e., the “system”) versus the performance of FSRPX during all other months (i.e., the “Anti System”) on an annual basis. The results are fairly striking

Figure 4 – Systems results versus “Anti System” Results

Figure 5 – Systems results versus “Anti System” Results

A few things to note:

-The System has showed a gain 21 out of 24 years.

-The Anti System showed a gain in only 11 years.

-The System outperformed the Anti System 75% of the time.

-The System showed a net gain of +794%.

-The Anti System showed a net loss of -30%.

Summary

Obviously during some years retailing stocks will rally outside of our four “favorable” months (for example, this year). But the long-term results suggest that investors would do well to focus on retailing stocks during February, March, October and November.

A Note for Option Traders

One less expensive way to make this play is to buy a deep-in-the-money call option on ticker XRT (SPDR Retail ETF). Here is an example:

-On 9/30/2013 a trader could have purchased 400 shares of XRT at $82.01 a share. The cost of this trade would be $32,804. The net delta of this position is 400.

-An option trader could have bought 5 December XRT 76 call option at $6.90. The cost of this trade would be $3,450. This option has a delta of 81.29, so buying 5 contracts yields a net delta of 401.26. In other words, this position will behave just like the stock position, but at a fraction of the cost ($3,450 versus $32,804).

Figure 6 –XRT December 76 call option as a replacement for stock shares (Courtesy: www.OptionsAnalysis.com)

As this is written:

-400 XRT shares are up 2% on an investment of $32,804 since 9/30.

-5 XRT December 76 calls options are up 13% on an investment of $3,450 since 9/30.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://aiq.com) client

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Oct 21, 2013 | Uncategorized

The Stock Trader’s Almanac, put out each year by the Hirsch Organization, is one of my favorite publications. Interesting ideas are one thing. Interesting ideas that actually work are entirely something else. And the Almanac is chock full of just that.

Of course, some of us are not content to leave well enough alone (Hi, my name is Jay). One system that I follow involves using the Almanac’s “Nasdaq’s Best Eight Months Strategy” with MACD Timing. However, instead of buying a stock index I focus on the top performing Fidelity Select Sector Funds.

The method works like this:

-Starting on October first, track the action of the MACD indicator for the Nasdaq Composite Index using MACD parameter values of 8/17/9.

-When the fast line crosses above the slow line – or if the fast line is already above the slow line on 10/1, a buy signal occurs.

Figure 1 displays the most recent buy signal which occurred at the close on 10/15/13.

Figure 1 – MACD Buy Signal (Chart courtesy of AIQ TradingExpert)

-Then find the five top Fidelity Select sector funds.

There are a number of different ways to do this. The method I use is to run AIQ TradingExpert Relative Strength report over the past 240 trading days. This routine looks at the performance of each fund over 240 trading days but gives extra weight to the most recent 120 days. You can use different variables, or you can simply look at raw price change over the previous 6 months to come up with a list of “Top Select Sector Performers.” The list for 10/15/13 appears in Figure 2.

Figure 2 – High Relative Fidelity Select Sector Funds (Courtesy AIQ TradingExpert)

-Buy the top five Select Sector funds the next day.

-Starting on June 1st of the next year, track the action off the MACD indicator for the Nasdaq Composite Index using MACD parameter values of 12/25/9.

When the fast line crosses below the slow line – or if the fast line is already above the slow line on 6/1, then sell the Fidelity Select sector funds on the next trading day.

Repeat.

Results

The test period used here starts in October of 1998. The year-by-year results of this system during the Favorable eight month period versus the performance of the S&P 500 Index during the same time appears in Figure 3.

Figure 3 – Year-By-Year Bullish Eight Months (System vs. SPX)

|

Measure

|

System

|

S&P 500 Index

|

|

Number of times UP

|

14 (93%)

|

11 (73%)

|

|

Number Times Down

|

1(7%)

|

4 (27%)

|

|

Number time better performer

|

11

|

4

|

|

Average % +(-)

|

+14.1%

|

+6.2%

|

|

Worst %+(-)

|

(-0.8%)

|

(-10.9%)

|

Figure 4 – System versus S&P 500 during “Bullish Eight Months”

Summary

As you can see, this relatively simple system has registered a gain in 14 of the past 15 “bullish” eight month periods. On average it has outperformed the S&P 500 by a factor of 2.27-to-1.

So does any of this mean that a portfolio of FSAVX/FBIOX/FBSOX/FSCSX/FSESX is sure to make money and outperform the S&P 500 between now and June of 2014? Sadly, no.

I guess I’ll just have to take my chances.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro client

http://jayonthemarkets.com/

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Oct 21, 2013 | ETFs, group sector rotation, Seasonality, sector funds, trading strategies

The Stock Trader’s Almanac, put out each year by the Hirsch Organization, is one of my favorite publications. Interesting ideas are one thing. Interesting ideas that actually work are entirely something else. And the Almanac is chock full of just that.

Of course, some of us are not content to leave well enough alone (Hi, my name is Jay). One system that I follow involves using the Almanac’s “Nasdaq’s Best Eight Months Strategy” with MACD Timing. However, instead of buying a stock index I focus on the top performing Fidelity Select Sector Funds.

The method works like this:

-Starting on October first, track the action of the MACD indicator for the Nasdaq Composite Index using MACD parameter values of 8/17/9.

-When the fast line crosses above the slow line – or if the fast line is already above the slow line on 10/1, a buy signal occurs.

Figure 1 displays the most recent buy signal which occurred at the close on 10/15/13.

Figure 1 – MACD Buy Signal (Chart courtesy of AIQ TradingExpert)

-Then find the five top Fidelity Select sector funds.

There are a number of different ways to do this. The method I use is to run AIQ TradingExpert Relative Strength report over the past 240 trading days. This routine looks at the performance of each fund over 240 trading days but gives extra weight to the most recent 120 days. You can use different variables, or you can simply look at raw price change over the previous 6 months to come up with a list of “Top Select Sector Performers.” The list for 10/15/13 appears in Figure 2.

Figure 2 – High Relative Fidelity Select Sector Funds (Courtesy AIQ TradingExpert)

-Buy the top five Select Sector funds the next day.

-Starting on June 1st of the next year, track the action off the MACD indicator for the Nasdaq Composite Index using MACD parameter values of 12/25/9.

When the fast line crosses below the slow line – or if the fast line is already above the slow line on 6/1, then sell the Fidelity Select sector funds on the next trading day.

Repeat.

Results

The test period used here starts in October of 1998. The year-by-year results of this system during the Favorable eight month period versus the performance of the S&P 500 Index during the same time appears in Figure 3.

Figure 3 – Year-By-Year Bullish Eight Months (System vs. SPX)

|

Measure

|

System

|

S&P 500 Index

|

|

Number of times UP

|

14 (93%)

|

11 (73%)

|

|

Number Times Down

|

1(7%)

|

4 (27%)

|

|

Number time better performer

|

11

|

4

|

|

Average % +(-)

|

+14.1%

|

+6.2%

|

|

Worst %+(-)

|

(-0.8%)

|

(-10.9%)

|

Figure 4 – System versus S&P 500 during “Bullish Eight Months”

Summary

As you can see, this relatively simple system has registered a gain in 14 of the past 15 “bullish” eight month periods. On average it has outperformed the S&P 500 by a factor of 2.27-to-1.

So does any of this mean that a portfolio of FSAVX/FBIOX/FBSOX/FSCSX/FSESX is sure to make money and outperform the S&P 500 between now and June of 2014? Sadly, no.

I guess I’ll just have to take my chances.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro client

http://jayonthemarkets.com/

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Oct 17, 2013 | Uncategorized

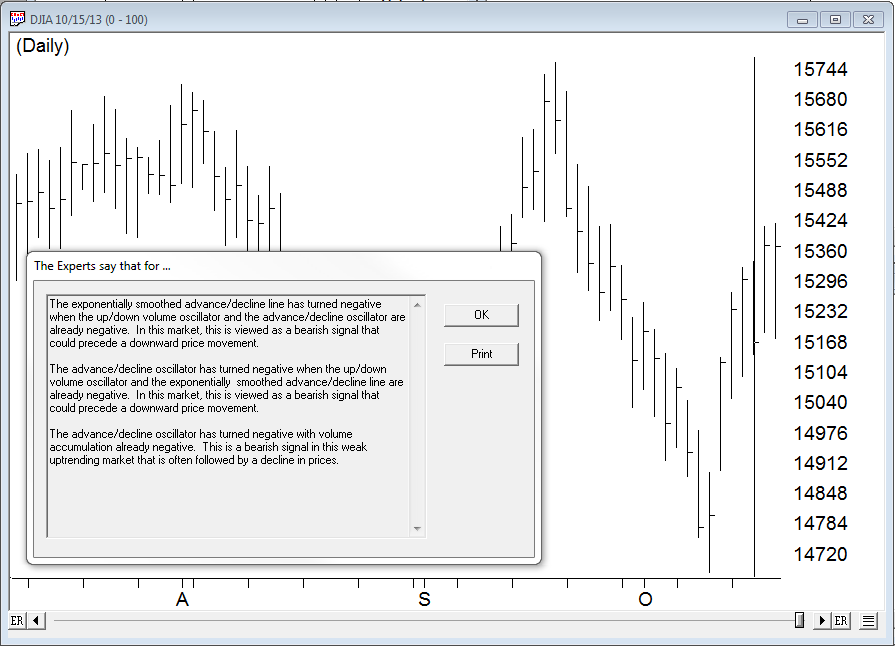

On Tuesday 10-15-2013 our AI market expert system fired a 0-100, that indicates a heavy weighting to the downside on the technical indicators. This is what the AI said

“The exponentially smoothed advance/decline line has turned negative wh…en the up/down volume oscillator and the advance/decline oscillator are already negative. In this market, this is viewed as a bearish signal that could precede a downward price movement.

The advance/decline oscillator has turned negative when the up/down volume oscillator and the exponentially smoothed advance/decline line are already negative. In this market, this is viewed as a bearish signal that could precede a downward price movement.

The advance/decline oscillator has turned negative with volume accumulation already negative. This is a bearish signal in this weak uptrending market that is often followed by a decline in prices. “

http://aiqsystems.com/

Oct 17, 2013 | expert ratings

On Tuesday 10-15-2013 our AI market expert system fired a 0-100, that indicates a heavy weighting to the downside on the technical indicators. This is what the AI said

“The exponentially smoothed advance/decline line has turned negative wh…en the up/down volume oscillator and the advance/decline oscillator are already negative. In this market, this is viewed as a bearish signal that could precede a downward price movement.

The advance/decline oscillator has turned negative when the up/down volume oscillator and the exponentially smoothed advance/decline line are already negative. In this market, this is viewed as a bearish signal that could precede a downward price movement.

The advance/decline oscillator has turned negative with volume accumulation already negative. This is a bearish signal in this weak uptrending market that is often followed by a decline in prices. “

http://aiqsystems.com/

Oct 8, 2013 | Uncategorized

Well according to reports that I have read, we are a little over a week away from Financial Armageddon, or at least that is what we are told will unfold if Congress does not raise the debt limit by October 17th. For if the debt limit is not raised by that time then the Fed will be unable to pay its bills (the 17 trillion dollars of debt that we have already raked up only means that up to now we have simply been “unwilling” to pay our bills – which apparently is different than “unable”), which means the U.S. Government may default and that the whole “Full Faith and Credit” thing will suddenly become worth approximately “a bucket of warm spit.” OK, that’s the Bad (granted, Very Bad) News. But there are two pieces of good news.

First, the financial markets are so far taking financial Armageddon pretty darn calmly. Sure the stock market is down a little bit of late, but overall it appears to be doing its best Alfred E. Nuemann (“What, Me Worry?”) impersonation. As a side note, I can’t quite figure out what the “Flight to Quality” crowd will do once the treasury defaults. I can’t help but think that half of them will buy treasury bonds anyway just as a reflex and because they don’t know what else to do (Old dogs, new tricks, if you get my drift).

The other piece of good news is that our elected politicians are “hard at work” attempting to solve this problem (Granted our elected officials appear to have a “slightly” different definition of “Hard at Work” than the rest of us shlubs). Whatever else you can say about them, our politicians are definitely busy engaging in politics these days. Nothing that will do any of us any good, granted, but hey, this whole “We the People” thing is getting just about as outdated as that whole “Full Faith and Credit” thing. So perhaps they are simply planning to wipe out both of these “antiquated” concepts in one fell swoop (at least that’s the only explanation that comes to mind).

When I think of our president and Congress I keep envisioning that image of those guys playing poker in the lounge of the Titanic. Sitting there at a 45 (and ever increasing) degree angle, they remain focused on what they considered to be the most important thing – “Hey, I think I can win this hand!”

Of course as we all know, all of this is completely and entirely the fault of [your least favorite political party here]. And no one can tell anyone otherwise.

What to Do, What to Do

Needless to say, everyone is pretty much assuming that something will happen at the 11th hour that will allow us to avoid “Shock and Awe, and Not in a Good Way” to our economy. Otherwise there might be just a tad more concern being reflected in the financial markets. Still it might be wise to think things through just a bit and to avoid “the conditioned response.”

Some of you may recall the utter “fear and loathing” that preceded the heavily anticipated “Fiscal Cliff” that we were going to plunge off of on January 1st of 2013. How did that work out? With a 20%+ gain in the stock market in the ensuing 8 months, of course. So there is a certain part of us that is now conditioned to believe that “potentially economically catastrophic events” lead to “above average returns”, which I am not entirely sure is the proper lesson. If nothing else, it’s a pretty small sample size.

So should investors simply take solace and assume that “things will work out?” Or is some sort of “defensive action” in order? At this point I think it is wise to invoke that age old bit of wisdom that states, “Hope for the Best, Prepare for the Worst.” At this point there are two basic theoretical scenarios:

1. A deal is reached to avoid a U.S. default and stocks bounce and bonds do not collapse.

2. The U.S. does default and stocks and U.S. treasury securities tank.

If you are a typical investor with a typical allocation of your portfolio to stocks then you don’t really need to “do” anything to take advantage of scenario #1. So that was easy.

Scenario #2 is “a little trickier”. There is a school of thought that states (probably accurately) that if the U.S. does default on its debt there will be far bigger problems than your stock portfolio. And that may be true. But in this worst case scenario it is not like the stock market will close down for good, the economy will (immediately) grind to a halt and we will all begin just “living off the land.” So “just in case”, it might make sense to “hedge.”

One Possibility

As I have written about recently, my new favorite hedging tool (for hedging specifically against an adverse move in the stock market) are call options on ticker VXX, the exchange-traded fund that ostensibly tracks futures contracts on the VIX Index.

The bottom line is simple to understand:

-When the stock market goes down, the VIX Index goes up.

-And the harder the stock market falls, the more quickly the VIX Index “spikes”.

So if you have concerns about a stock market decline then a cheap VXX call option can offer some pretty good upside potential. A trade that I highlighted recently involving VXX call options appears in Figures 1 and 2. (http://jayonthemarkets.com/2013/09/17/looking-to-vxx-just-in-case/)

Figure 1 – VXX Nov 14 Call Option (courtesy www.OptionsAnalysis.com)

Figure 1 – VXX Nov 14 Call Option (courtesy www.OptionsAnalysis.com)

Figure 2 – VXX Nov 14 Call Option Risk Curves (courtesy www.OptionsAnalysis.com)

Figure 2 – VXX Nov 14 Call Option Risk Curves (courtesy www.OptionsAnalysis.com)

As you can see in Figure 3, VXX has rallied from 13.84 to 16.21, or +17%. In the same time the VXX call option shown in Figures 1 and 2 have advanced +116%. This clearly illustrates the potential benefit of leverage in the options market.

Figure 3 – Ticker VXX (exchange=traded fund) bounces recently (courtesy AIQ TradingExpert)

Figure 3 – Ticker VXX (exchange=traded fund) bounces recently (courtesy AIQ TradingExpert)

How high could VXX go if the U.S. somehow manages to default? Figure 4 displays the longer-term history of the VIX Index itself.

Figure 4 – The VIX Index; How High Can it Go? (courtesy AIQ TradingExpert)

Figure 4 – The VIX Index; How High Can it Go? (courtesy AIQ TradingExpert)

Just to “go to extremes”, if we had another meltdown along the line of 2008 and if ticker VXX rallied to 80, the November 14 VXX call option would be worth $66 a contract, or a gain of about +5,000% from the initial price on 9/20 (about +2,265% from current levels).

The Irony

The ironic part is that as exciting as a potential gain of 2,000 to 5,000% sounds, we absolutely, positively hope that it doesn’t happen. In fact, in the overall best case scenario these VXX call options expire worthless as the stock market rallies and volatility subsides.

What we hope is that our esteemed elected officials will get their act together and come up with a solid long-term plan to put the U.S. back on solid financial footing.

Or at the very least, that they avoid making us Thelma to their Louise.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro client

http://jayonthemarkets.com/

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.