The Dow Jones Industrial Average just changed — Alphabet replaced Verizon on June 29. The Transportation Average changed too — FedEx Freight replaced American Airlines on June 1.

And while the “Industrials” sit at record highs, the Transports are roughly 12% off their peak, hammered by oil back above $100 a barrel.

Charles Dow Had a Name for This

Non-confirmation. It preceded the 1973 top. It preceded the 2000 top.

It also fired plenty of false alarms.

So which is it this time — warning or noise?

Opinions are cheap. Signals are testable. In 45 minutes, Steve Hill shows you how to read this divergence with rules, not guesswork.

What You’ll Walk Away With

01 · The 2026 Dow, Decoded

Exactly what changed in the Dow 30 and TRAN this year, and why “Industrial” is now mostly a nickname — Goldman, Nvidia, and Apple drive this index.

02 · Dow Theory in Plain English

What a DJIA/TRAN non-confirmation actually signals, when it has mattered historically, and when it hasn’t.

03 · The Oil Overlay

Why $100 crude hits the 20 Transports stocks directly (4 airlines, heavy trucking) while barely touching today’s Dow 30 — and making a group of fuel-sensitive names in TradingExpert Pro.

Steve Hill, Founder of WinWayCharts and CEO AIQ Systems, conducted a 45-minute Zoom session demonstrating how to use AI, specifically Claude by Anthropic, to create trading strategies and indicators within the TradingExpert Pro Expert Design Studio.

Steve showed how Claude can generate custom indicators and strategies from scratch, including a volume-weighted momentum indicator and a consecutive close filter indicator, which were successfully implemented and tested in the system.

He explained the process of creating these indicators, including debugging and testing them, and demonstrated how the AI-generated strategies could be backtested on a database of stocks.

Steve emphasized that while AI tools like Claude can significantly speed up the development process and create new indicators not previously available in the system, traders still need to validate and test the effectiveness of these strategies through backtesting and further refinement.

The last few weeks have been a gut-check: the Dow shed over 800 points in a session, the Nasdaq dropped 4% as the semiconductors rolled over, the VIX is spiking, and roughly a trillion dollars of market value has evaporated.

This is exactly the environment that separates disciplined traders from emotional ones.

Join Steve Hill,founder of WinWayCharts and CEO of AIQ Systems, as He Covers

01 · Before the Drop

What AIQ’s Market Timing model and Expert Rating were signaling before the drop

02 · Calling the Turn

How MACD divergence and Phase Analysis called the turn in the semiconductors

03 · Finding the Leaders

An EDS screen to surface the stocks quietly holding up while everything else sells off

It’s a demonstration of reacting to the rules instead of the noise — the whole point of trading a system.

Watch Steve Hill break down market internals — and reveal why the S&P 500’s biggest moves are hiding inside just one sector.

The market is sending mixed signals. The Dow hits new highs. But under the surface, most sectors are going nowhere.

In this free video session, WinWayChart’s Steve Hill walks you through exactly what’s happening right now — and how TradingExpert Pro’s Expert Rating is helping traders cut through the noise.

In This Session You’ll See

01 · The Warning Before the Noise

How two Expert Rating down signals in May flagged the warning before most traders noticed

02 · One Sector, 30% of the Move

Why the technology sector now drives 30% of S&P 500 movement — and what that means for your timing

03 · Sector Breadth, Rebuilt

The new sector breadth analysis approach using 11 S&P 500 segments to pinpoint where opportunity is building

04 · Early Buy Signals

Which sectors — healthcare, materials — are flashing early buy signals right now

05 · The Catch-Up Question

Why the equal-weighted S&P 500 is lagging badly — and what it takes for the broader market to play catch-up

Steve Hill just wrapped a fast-paced 10-minute deep dive into something most traders have never seen done before: using sector ETF breadth data inside TradingExpert Pro to spot market rotation before it shows up in price.

Here’s why this is different from anything else out there:

Most breadth analysis stops at the NYSE or NASDAQ level. You see advancing vs. declining stocks, and you get a general sense of market health. That’s useful — but it’s incomplete.

When you break the S&P 500 down into its eleven sectors and track each one’s internal breadth data, something remarkable happens. You can see which sectors are quietly leading… and which are fading, even when the headline index looks fine.

Steve walks you through exactly how to set this up in TradingExpert Pro using special sector ETF tickers — and how to read the combined picture to spot high-probability rotation opportunities.

This is institutional-level analysis, built right into the software. Here are the files to make it happen. Don’t have AIQ? There’s a $1 trial offer below for you to check it out.

The 11 SP500 Sector markets are available in this zip file, unzip these to your wintes32/mdata folder

The 11 State Street ETFs are likely already in your AIQ database but are available in this zip file, unzip these to your /wintes32/tdata folder.

The list file for the 11 SP500 Sector markets is here, save to your wintes32 folder.

Make sure you go to Data Manager and under Utilities perform a Rebuild Master Ticker List. Also when updating your data each day, select Update Breadth Tickers and Compute Markets are selected.

The Zweig Thrust was also used on this video, the EDS file for this is here, save to your /wintes32/EDS Strategies folder. In Charts go to Chart, Settings, Indicator Library, EDS Indicators. Add the location to the Zweig EDS file, and for indicator type select one line with upper/lower support. Upper support set to 61, lower support to 40.

Markets in March 2026 were doing what markets do best — confusing people. Prices were pulling back. Headlines were negative. The majority of traders were uncertain, defensive, or on the sidelines.

But inside TradingExpert Pro, the market timing model was building a case. Not based on opinion. Not based on news. Based on the systematic, rule-by-rule analysis that AIQ has refined over three decades. And by the end of March, that case was overwhelming.

Here’s exactly what the system saw — and what it meant.

March 18 & 19 — The Opening Signal

On March 18, the AIQ market timing model issued an Expert Rating of 96 — Up. The following day, March 19, it fired again: another 96 — Up.

Back-to-back readings above 95 in consecutive sessions are not noise. An Expert Rating above 95 represents a high-conviction bullish technical condition — the system telling you, in its clearest language, that the weight of technical evidence favours higher prices. When that reading repeats on consecutive days, the model is reinforcing its own conclusion.

At this point, the disciplined AIQ trader is already paying close attention.

March 25 — Phase Analysis Confirms the Direction

4 days later, on March 25, Phase Analysis confirmed what the Expert Rating had been signalling.

The market Phase changed to Up.

This is a pivotal moment in any signal sequence. The Expert Rating identifies the condition; Phase Analysis identifies the trend cycle. When a high Expert Rating is followed by a Phase change in the same direction, the two most important components of the AIQ market timing model are in full agreement. The signal is no longer early — it is confirmed.

March 31 — The Full Picture

March 31 produced the most powerful single-day reading in the sequence — an Expert Rating of 98 — Up, arriving with Phase already turned upward. The individual timing rules that fired during this sequence tell a story that every AIQ trader should understand, because they illustrate precisely how the system thinks.

Rule 1: 21-Day Low Intraday Price with Positive Volume Accumulation

Intraday low prices declined to a 21-day low — a reading that, on the surface, looks bearish. But volume accumulation percentage was positive. In AIQ’s market timing logic, this non-confirmation is a weak bullish signal. Price is making new lows, but money is not leaving the market. That divergence matters.

Rule 2: 21-Day Low Closing Price with Rising Advance/Decline Breadth

Closing prices also reached a 21-day low. Again, superficially bearish. But market breadth — measured by advances versus declines — was increasing. When prices fall to new lows but more stocks are advancing than declining, the selling is not broad-based. This non-confirmation is a bullish signal indicating a possible upward price movement. The majority of the market is quietly holding up while the index prints a low.

Rule 3: 21-Day Low Closing Price with Rising Advance/Decline Oscillator

A third rule reinforced the same theme: closing prices at a 21-day low, but the advance/decline oscillator increasing. Another non-confirmation. Another bullish signal. Three separate breadth and price divergence rules all pointing the same direction — up.

Rule 4: 21-Day Stochastic Crossing the 20% Line with Rising Price Phase

The 21-day stochastic advanced and crossed the 20% line, while the price phase indicator was also increasing. In a weakly downtrending market, AIQ classifies this combination as a strong bullish signal suggesting an increase in prices. The stochastic crossing 20% from below is a classic oversold recovery signal — but paired with a rising price phase, it carries significantly more weight.

Rule 5: Rising Volume Accumulation with 21-Day Stochastic Above 20%

Volume accumulation percentage was increasing while the 21-day stochastic moved above the 20% line. In a downtrending market, AIQ rates this a strong bullish signal. Volume accumulation captures the relationship between buying and selling pressure over time. When it starts rising in a downtrend while momentum is recovering from oversold levels, the path of least resistance is shifting.

Rule 6: Negative Price Phase with Rising Volume Accumulation

Finally, even with the price phase still registering negative, volume accumulation had started to advance. In AIQ’s rules, this non-confirmation — volume diverging positively from a negative price phase — is a bullish signal regardless of market type. It doesn’t matter what the trend classification is. When volume accumulation turns up against a negative phase, the model says: the market is preparing to move higher.

What the Full Sequence Tells Us

Step back and look at this sequence as a whole.

March 18: Expert Rating 96 — Up. March 19: Expert Rating 96 — Up, confirmed. March 25: Phase changes to Up, validating both prior signals. March 31: Expert Rating 98 — Up, with six individual timing rules all firing bullish simultaneously, spanning price divergence, breadth divergence, volume accumulation, stochastic recovery, and phase analysis.

Every single component of the AIQ market timing model was in agreement. Rules that look at price. Rules that look at breadth. Rules that look at volume. Rules that look at momentum. All saying the same thing at the same time.

This is exactly the kind of multi-confirmation environment that the system is designed to identify — and that individual traders, relying on headlines or gut instinct, almost always miss. When prices are making 21-day lows and geopolitical news is negative, the human instinct is to step back. The AIQ system, by contrast, was reading below the surface and identifying that the internal structure of the market was quietly rebuilding.

The Lesson

Price can lie. Headlines always lie. But when multiple independent technical rules — breadth, volume, momentum, phase — all non-confirm a price low at the same time, the market is telling you something important: the selling is exhausted, and the buyers are already at work beneath the surface.

The March 2026 signal sequence is a textbook demonstration of why systematic, rule-based market timing produces results that emotional, discretionary trading cannot replicate. You don’t need to know whether the Iran conflict resolves or whether the Fed changes course. You need to know what the internals of the market are doing — and let a proven system tell you.

On March 18, the system said up. On March 19, it said it again. On March 25, Phase confirmed it. On March 31, rules piled on with a 98-rated exclamation mark.

The traders who followed the signals were on the right side of the move. That’s what systematic market timing is built for.

How Five Market Timing Signals Captured 4,500 Points While Avoiding Two Major Declines

One of the most common questions we hear from traders is: “Can a systematic approach really identify market turning points in real-time?” The answer is yes—when you have the right tools and a disciplined, rule-based methodology.

Let me show you exactly how AIQ Market Timing navigated a volatile 2.5-month period from October 2025 through January 2026, capturing three significant rallies totaling 4,500 points while protecting capital during two major reversals totaling over 3,000 points of decline.

The Setup: Multiple Bullish Confirmations (October 20, 2025)

On October 20th, AIQ Market Timing issued a 98 UP signal at 46,707 on the Dow Jones Industrial Average. But this wasn’t just a single indicator flashing green—it was a confluence of five critical rules firing simultaneously:

Rule #1: Trend Status Confirmation

Trend Status changed to a weak upward trend

This indicated an upward trend was starting that could continue

Classification: Moderate bullish signal

Rule #2: Exponentially Smoothed A/D Line

The smoothed advance/decline line turned positive

Key factor: The UD volume oscillator and A/D oscillator were ALREADY positive

This alignment is viewed as bullish, often preceding upward price movement

Rule #3: Up/Down Volume Oscillator

The UD volume oscillator turned positive

Confirmation: A/D oscillator and smoothed A/D line were already positive

This convergence signaled institutional buying was building

Rule #4: Advance/Decline Oscillator

The A/D oscillator turned positive

Supporting indicators: UD volume and smoothed A/D line already positive

Multiple breadth measures confirming the move

Rule #5: Volume Accumulation Alignment

A/D oscillator turned positive with volume accumulation already positive

In a weak upward market, this signals prices could continue rising

Professional money was accumulating positions

The Result: +1,333 Points in 8 Days

The market moved from 46,707 on October 21st to 48,040 on October 29th—a gain of 1,333 points (+2.85%) in just eight trading days.

This is the power of waiting for multiple confirming indicators rather than jumping on single signals. The system identified strong internal market momentum that wasn’t yet obvious to casual observers.

The Top: System Catches the Reversal (October 30, 2025)

Just one day after the market high, on October 30th at 47,659, AIQ Market Timing 98 issued a DOWN signal. The system caught the top within just 11 points of the absolute high (48,040 vs. 47,659).

Two Critical Bearish Rules Fired:

Rule #1: Breadth Deterioration

The exponentially smoothed A/D line turned negative

Warning sign: UD volume oscillator and A/D oscillator were already negative

This indicated institutional distribution was underway

Rule #2: Volume Accumulation Breakdown

Volume accumulation turned negative

The A/D oscillator was already negative

In a downtrending market, this bearish signal often precedes price declines

Initial Decline: -1,164 Points in 7 Days

From the October 31st level of 47,659, the market dropped to 46,495 by November 7th—a decline of 1,164 points (-2.44%) in seven trading days.

Traders following these signals would have been long for the +2.85% rally and either flat or profitably short for the -2.44% decline.

The Confirmation: Second Down Signal (November 4, 2025)

On November 4th, while the market was still declining, AIQ Market Timing 98 issued a second DOWN signal, reinforcing the bearish outlook. This is where systematic trading truly shines—when multiple signals confirm the trend in real-time.

Three Additional Bearish Rules Fired:

Rule #1: Trend Status Reversal

Trend Status changed to a weak downward trend

This confirmed the downward trend was likely to continue

Classification: Moderate bearish signal

Rule #2: Stochastic and Volume Divergence

Volume accumulation percentage was decreasing

The 21-day stochastic moved below the 80% line

In a downtrending market: Strong bearish signal

This combination often precedes significant downward price movement

Rule #3: UD Volume Oscillator Breakdown

The UD volume oscillator turned negative

Critical context: Smoothed A/D line and A/D oscillator were already negative

This confirmed selling pressure was intensifying

Signal #3: Back to Bullish (November 10, 2025)

On November 10th at 47,368, AIQ Market Timing issued an UP signal (97), indicating the correction had run its course and a new upward move was beginning.

Four Powerful Bullish Rules Fired:

Rule #1: Exponentially Smoothed A/D Line

Turned positive with UD volume oscillator and A/D oscillator already positive

This alignment indicated strong bullish internal momentum building

Rule #2: Advance/Decline Oscillator Confirmation

Turned positive with UD volume oscillator and smoothed A/D line already positive

Multiple breadth measures confirming the new uptrend

Rule #3: Volume Accumulation Alignment

A/D oscillator turned positive with volume accumulation already positive

In a sideways market, this signals prices could begin upward movement

Professional buying was returning

Rule #4: New High/New Low Reversal

The NH/NL indicator reversed to the upside

Classification: Reliable bullish signal

Often followed by upward price movement

In a sideways market, an uptrend could start shortly

The Rally: +1,063 Points in 3 Days

The market surged from 47,384 on November 11th to 48,431 on November 13th—a gain of 1,040 points (+2.22%) in just three trading days.

Signal #4: The Top Again (November 13, 2025)

At the market high of 48,233, AIQ Market Timing issued a DOWN signal (100), once again catching the reversal with precision.

Five Bearish Rules Fired:

Rule #1: Stochastic and Price Phase Weakness

21-day stochastic declined below the 80% line

Price phase indicator also decreasing

In the uptrending market: Weak bearish signal indicating possible near-term decline

Rule #2: Smoothed A/D Line Breakdown

Turned negative with UD volume and A/D oscillator already negative

Clear sign of breadth deterioration

Rule #3: UD Volume Oscillator Reversal

Turned negative with smoothed A/D line and A/D oscillator already negative

Institutional selling was intensifying

Rule #4: A/D Oscillator Breakdown

Turned negative with UD volume and smoothed A/D line already negative

All breadth measures aligned bearishly

Rule #5: New High/New Low Reversal

The NH/NL indicator reversed to the downside

Classification: Reliable bearish signal

Often followed by downward price movement

In an uptrending market, a trend reversal could occur

The Decline: -1,500 Points in 7 Days

From November 14th’s open of 47222, the market plunged to 45,728 on November 20th—a drop of nearly 1500 points (3.16%) in five trading days.

This was a significant correction that caught many traders off guard. But AIQ Market Timing identified it precisely at the top.

Signal #5: The Current Rally (November 18, 2025 – Present)

On November 18th at 46,091, AIQ Market Timing issued an UP signal (96), catching the bottom of the correction and positioning traders for what would become a powerful sustained rally.

The Rally Continues: over 3000 Points and Counting

From the November 19th entry at 46,138, the market has surged to 49,616 as of January 13, 2026—a gain of over 3,300 points (+7.0%) that is STILL RUNNING.

This ongoing rally has already lasted 45 days and shows the power of staying with a trend when the system confirms the move.

The Complete Picture: What This Teaches Us

Over a 2.5-month period from October 21, 2025 to January 9, 2026, AIQ Market Timing issued five signals:

The Numbers Are Staggering

Total gains captured: over 5,000 points across three rallies Total declines avoided: over 3,000 points across two corrections Current position: Still long in a rally that has gained 7.0%

Compare this to buy-and-hold over the same period:

Started: 46,707 (Oct 21)

Current: 49,504 (Jan 9)

Buy-and-hold gain: +2,797 points (+5.99%)

This sequence demonstrates several critical principles of successful systematic trading:

1. Confirmation Over Single Indicators

Every up signal had multiple rules firing together—not weak, isolated signals but powerful confluences showing aligned market internals. Signal #1 had five rules, Signal #3 had four rules including the reliable NH/NL indicator.

2. Speed Matters

The system caught reversals with remarkable precision: one day after the October high, right at the November 13th high. Manual observation would have missed these turning points.

3. Internal Strength vs. Price Action

The breadth indicators (A/D measures, volume accumulation, UD volume, NH/NL) detected shifts in market character before they became obvious in price alone.

4. Consistency Across Different Market Conditions

This wasn’t a lucky streak. The system worked in:

Weak upward trends (October)

Weak downward trends (early November)

Sideways markets (mid-November)

Strong sustained uptrends (late November – January)

5. Multiple Cycles Compound Returns

Notice how the system didn’t just catch ONE move—it navigated FIVE distinct market phases. This is where systematic trading truly shines: the ability to stay on the right side of the market through multiple cycles.

6. Reliable Indicators Add Conviction

The New High/New Low indicator appeared in both Signal #3 (bullish reversal) and Signal #4 (bearish reversal), classified as “reliable” both times. When these high-probability signals appear, they deserve attention. Adding in the Phase indicator, confirmation was present for all the signals and is considered a valid confirmation within +/- 3 days of the signal.

7. Both Sides of the Market

This wasn’t just about catching rallies. The system protected capital by identifying when conditions changed, allowing traders to exit longs, stay in cash, or even profit from declines totaling 3,669 points.

Multiply this advantage over weeks, months, and years, and you begin to understand why systematic, rule-based trading provides such a significant edge.

The Bottom Line

AIQ Market Timing isn’t about predictions or gut feelings. It’s about:

Objective rules that fire based on market internals

Multiple confirming indicators that reduce false signals

Real-time alerts that keep you informed as conditions change

Historical validation proving the methodology works across different market environments

Consistent performance across multiple market cycles

Are you ready to trade with this level of systematic precision? $1 trial available

Learn more about AIQ Market Timing 98 and other professional-grade technical analysis tools at AIQ Systems.

Past performance does not guarantee future results. All trading involves risk. The examples shown are for educational purposes and represent act

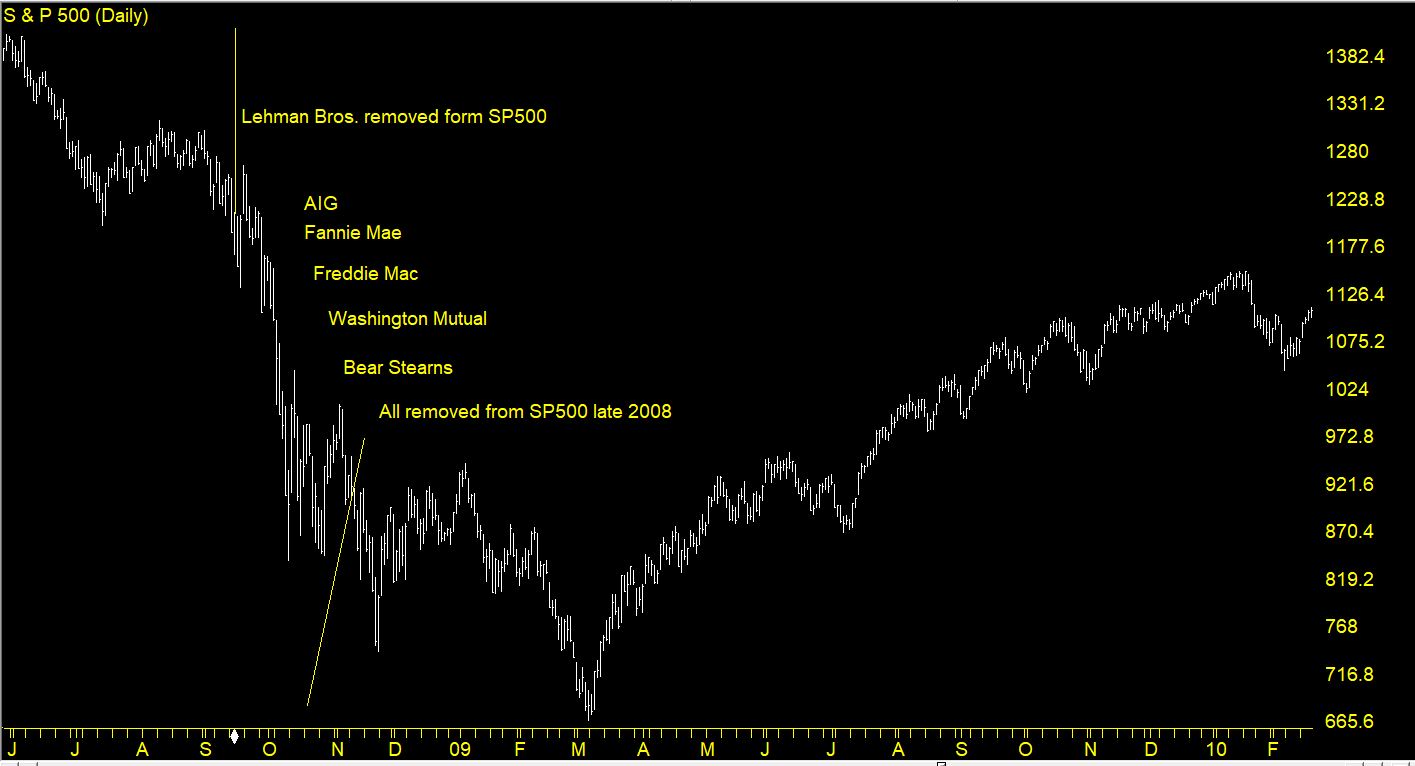

When traders look at long-term index performance charts, it’s tempting to assume they reflect the “true” experience of investors over time. But there’s a hidden distortion baked into indices like the S&P 500 and Russell 2000: survivorship bias. This bias occurs because failing companies are regularly removed and replaced by stronger firms, making historical index performance look healthier than what an actual buy-and-hold investor might have experienced.

How Survivorship Bias Skews the S&P 500

The S&P 500 is marketed as a snapshot of the 500 largest U.S. companies, but the membership list is far from static. Every year, dozens of names are swapped in and out. Companies that go bankrupt or underperform are removed, while stronger or fast-growing companies are added.

The SP500 index with major stocks removed at the height of the financial crisis

Consider the S&P 500 in 2007. Back then, financial giants like Lehman Brothers, Bear Stearns, and Washington Mutual were all part of the index—until the financial crisis exposed their fragility. Those stocks went to zero, but the historical chart of the S&P 500 smooths over their collapse because new leaders like Amazon, Nvidia, and Tesla later replaced them. The result: the long-term S&P 500 chart looks like a steady upward march, when in reality, an investor in the 2007 version of the index would have faced far more volatility and permanent capital loss in certain holdings.

This explains why the index’s backward-looking return can feel disconnected from the lived experience of investors who actually held the stocks in those earlier lineups.

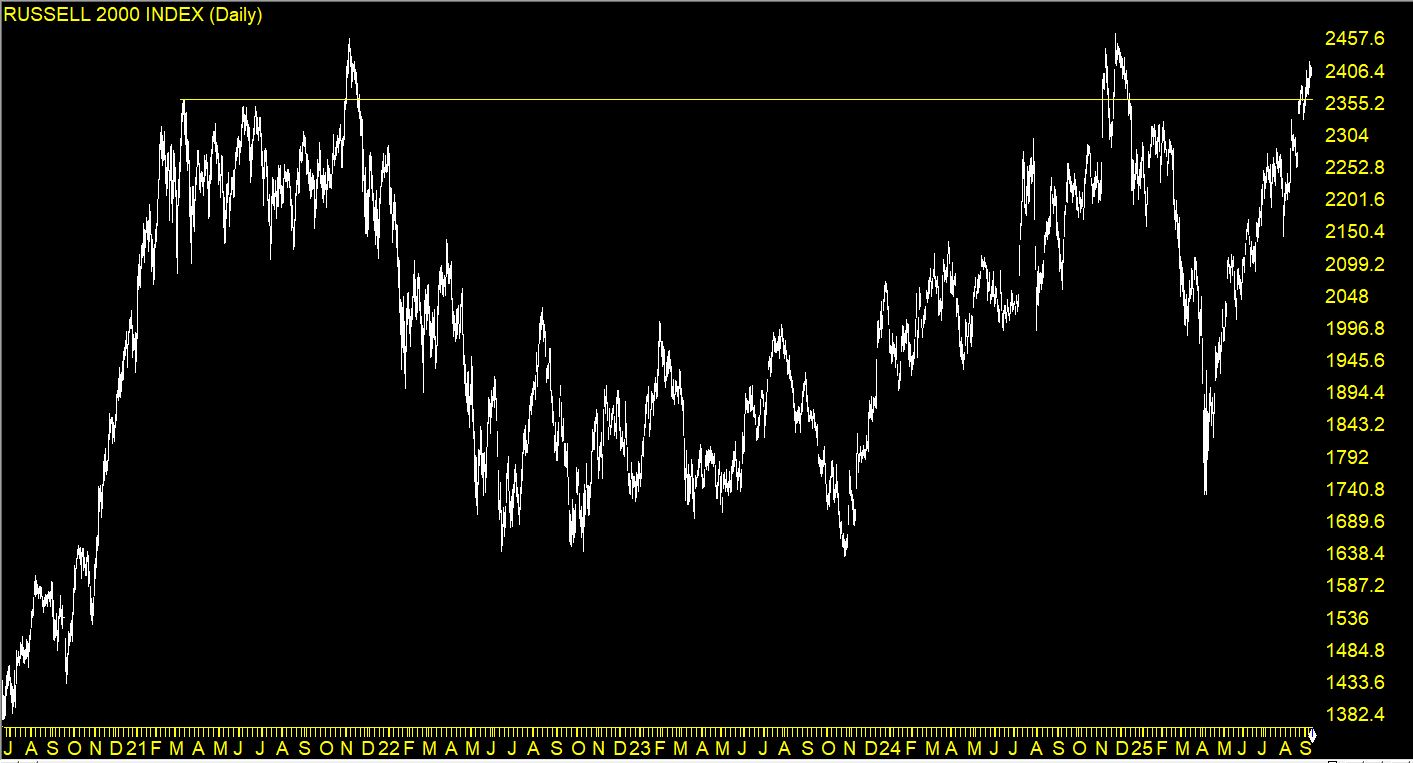

The Russell 2000: Why It’s Barely Moved in 5 Years

The Russell 200 chart from late 2020 to current

The Russell 2000 highlights survivorship bias in another way. Unlike the S&P 500, which rotates in stronger companies, the Russell is composed of small-cap stocks, many of which don’t survive or struggle to grow consistently.

Over the past five years, the Russell 2000 has barely moved, stuck in a sideways range, even while the S&P 500 has marched higher. Why? Because many small caps in the Russell 2000 face structural challenges—thin margins, high debt, vulnerability to rising interest rates—that prevent them from compounding like large-cap tech stocks. Although the Russell swaps out some names, the sheer number of struggling companies means the index reflects more of the “grind” of small-cap reality. Survivorship bias here doesn’t create the same illusion of strength—it highlights stagnation instead.

Why This Matters for Traders

Survivorship bias creates a dangerous blind spot: it makes past returns look better than what an investor might have achieved if they actually owned the index’s constituents at the time.

For the S&P 500, it means that long-term performance charts hide the graveyard of failed companies. The winners dominate the narrative, but the losers were just as real for investors who held them.

For the Russell 2000, it means traders need to be aware that many of its members are structurally weak, which can cap index-level returns despite occasional rallies.

How Traders Can Navigate Survivorship Bias

Dig Into Index Components – Don’t just look at the headline number. Study which sectors and companies are driving the gains or stagnation.

Use Equal-Weight Alternatives – The S&P 500 Equal Weight Index provides a different perspective, diluting the effect of mega-cap leaders and better reflecting the average stock’s performance.

Blend With Sector/ETF Analysis – Instead of relying only on broad indices, drill down into sector ETFs or specific trading groups to uncover true leadership and laggards.

Keep Survivorship in Mind – When backtesting or studying history, remember the S&P 500 of 2007 is not the same as today’s. Adjust your expectations accordingly.

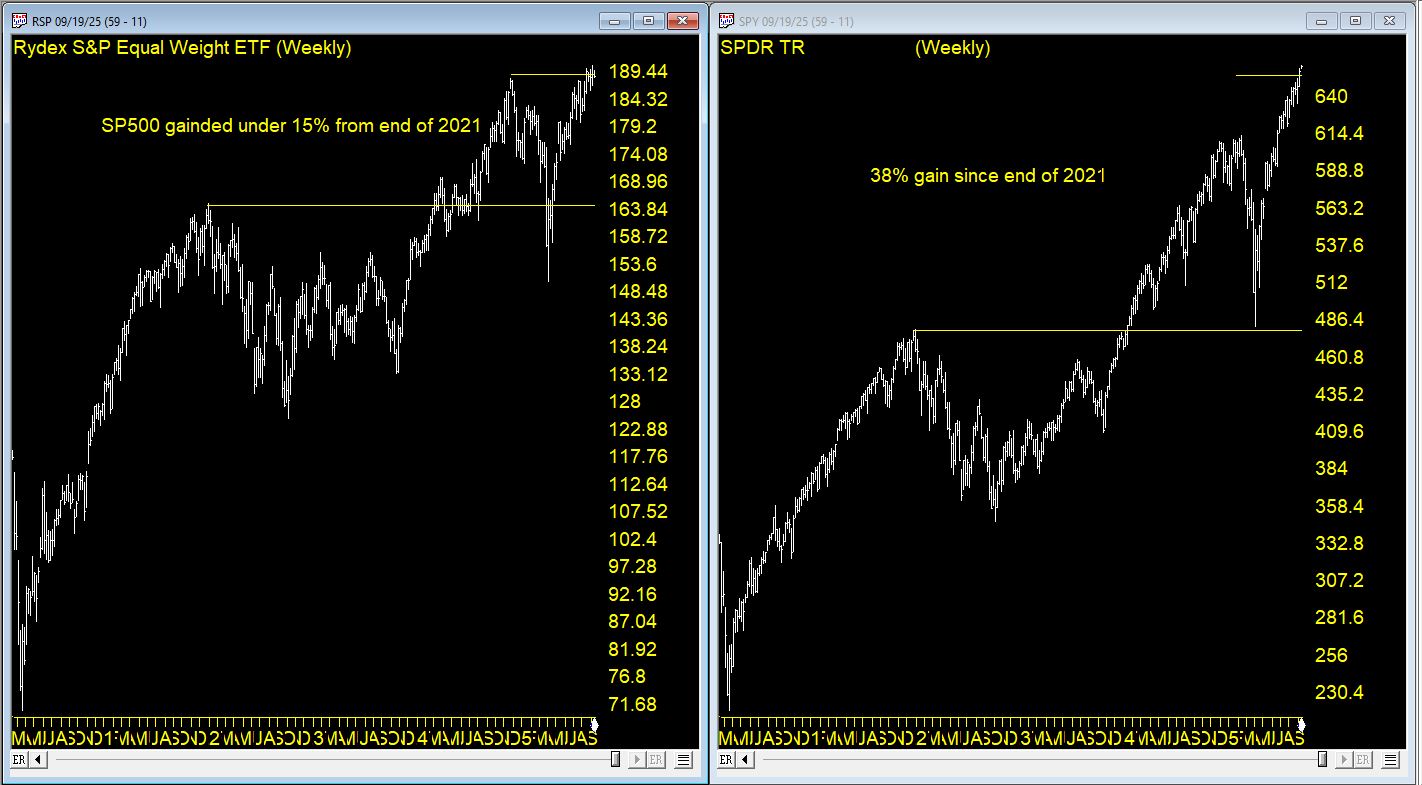

Equal-Weighted vs Cap-Weighted Indices: Why the Difference Matters

Most traders are familiar with the standard S&P 500, but fewer realize it’s a market-cap weighted index. That means larger companies (like Apple, Microsoft, Nvidia, and Amazon) dominate its movements. A 5% swing in Apple carries far more weight than a 5% move in a mid-cap stock buried deep in the index. Over time, this weighting system concentrates returns in a handful of mega-cap leaders, amplifying the survivorship bias effect: the winners shape the chart, while the losers fade into irrelevance.

By contrast, the S&P 500 Equal Weight Index treats every company the same, regardless of size. Each stock counts for 0.2% of the index at rebalancing. This approach provides a more balanced view of how the average stock in the S&P is performing. During periods when mega-cap tech leads the market (like the last several years), the equal-weight index lags behind the cap-weighted S&P. But in broad-based rallies where many sectors participate, the equal-weight version often outperforms.

This chart compares the SPY ETF, a perfect surrogate for the SP500 index vs RSP, the Rydex SP500 Equal Weighted ETF. Total return for SPY from the end of 2021 was around 38%. For the RSP it was 15% for the same period.

Why This Matters for Traders

Cap-Weighted Bias – The standard S&P 500 often hides the struggles of most companies because the top 5–10 stocks drive the majority of returns.

Equal-Weight Reality Check – Equal weighting exposes whether the rally is broad or narrow. If the equal-weight index is flat while the cap-weighted index surges, it’s a sign that leadership is very concentrated.

Practical Application – Traders can compare the two versions (SPX vs RSP) to gauge market health. A wide gap between them signals that survivorship bias and concentration are distorting the headline numbers.

Final Thoughts

Market indices are invaluable tools, but they aren’t perfect mirrors of reality. Survivorship bias smooths over failures, amplifies winners, and sometimes hides the real risks of buy-and-hold investing. By understanding how indices evolve—and by analyzing beneath the surface—traders can avoid being lulled into a false sense of security and make smarter, more grounded trading decisions.

WinWayCharts Market Timing Expert Ratings compress hundreds of technical conditions into a single, actionable score. Use 95+ up or down ratings as “of-notice” events, then confirm direction with the Price Phase indicator before acting. This simple two-step process keeps you aligned with the dominant swing while filtering many head fakes.

What the Market Timing Expert Rating Really Is

Under the hood, the Expert System evaluates ~400+ indicator states through an inference engine (decision-tree style) and outputs a daily market rating—from neutral to powerful up/down signals. You’ll also see these ratings plotted directly on historical charts in TradingExpert Pro.

Why that matters: Instead of juggling dozens of internals, you get a unified, explainable read of market conditions that has been kept methodologically stable for years (no goal-post shifting or perpetual re-optimization). That stability helps make the historical behavior of the signals more comparable across cycles.

Market Timing signals with confirmation by Phase Jan – May 2025

The Confirmation Key: WinWayCharts Price Phase Indicator

WinWayCharts explicitly recommends using the Price Phase Indicator (“Phase”) as the primary filter for Expert Ratings. When Phase direction agrees with a high Expert Rating signal, the signal is considered confirmed. In other words:

Strong Up Rating (≥95) → look for Phase turning up or already rising to confirm.

Strong Down Rating (≥95) → look for Phase turning down or already falling to confirm.

This is purposeful: Expert Ratings often fire early—giving you a heads-up—while Phase helps you avoid acting too soon. Think of Ratings as the alert and Phase as the green light.

Interpreting the Score: When Does “High” Mean “Actionable”?

Per guidance, 95 or greater to the upside or downside is the zone “of notice.” That’s when you should lean in, check Phase, and consider entries/exits or hedges—not when readings are middling or neutral. Most days are neutral; the edge lives in waiting for 95+ and confirming with Phase.

WinWayCharts Market Timing signals with confirmation by Phase May – Aug 2025

Where to See It in TradingExpert Pro

On your WinWayCharts Main Menu, select Market Charts, and plot Price Phase in a lower pane. This combination is designed for side-by-side evaluation.

If you prefer a visual “state” view, Heikin-Ashi-mode bars with Phase underneath are often used in WinWayCharts’s examples to highlight trend persistence.

How to Read the 2025 Chart (Step-by-Step Playbook)

Spot the Spike

Scan for 95+ up/down ratings. Put a small flag on each to review.

Check Phase Direction

If the rating is Up (≥95), is Phase rising or just turned up?

If Down (≥95), is Phase falling or just turned down? Match = Confirmation. No match? Put it on watch—often the earliest ratings need a bar or two before Phase confirms.

Plan Entries/Exits

For confirmed Up: consider scaling into risk-defined long exposure, tightening shorts.

For confirmed Down: consider trimming longs, or tactical shorts—again, with risk clearly defined.

Manage the Hold

Historical AIQ studies often show swing-length holds rather than ultra-short scalps (average holds are one week to several weeks), but your trade horizon should match your strategy.

Best Practices (That Save You from Heartache)

Don’t front-run Phase on big ratings. Early feels clever until it doesn’t. Let the filter do its job.

Treat 95 as your attention alarm. Below that, conserve focus; above that, prepare plans.

Neutral = No edge. Most days are noise; your edge is in selectivity.

Common Questions

Q: Are the rules curve-fit over time? A: We deliberately keeps the rating calculation stable, avoiding constant re-tuning. That consistency is part of why the historical behavior is analyzable.

Q: Is Phase the only valid confirmation? A: It’s primary confirmation tool for Expert Ratings and the one used in the official “confirmed” flagging. You can add your own overlays, but Phase remains the recommended filter.

Q: Do signals work on intraday charts? A: The Market Timing ratings are generated daily. You can time entries intraday after a daily confirmation, but the signal itself is evaluated on the daily close framework.

Final Word

WinWayCharts Market Timing Expert Ratings give you clean, explainable signals—and the Price Phase indicator gives you the discipline to act only when odds tilt in your favor. Use the 95+ threshold to focus, Phase to confirm, and your risk plan to stay in the game when it counts.

In a recent Zoom meeting, Steve Hill, founder of WinWayCharts, shared Bollinger Bands Setups, Variations & Trade Timing. In this article, we’ll expand on using %B and creating custom indicators to help identify trade setups using Bollinger Bands and %B.

When John Bollinger introduced Bollinger Bands in the 1980s, traders gained a powerful visual tool for understanding market volatility and potential turning points. But tucked away inside the Bollinger Band toolkit is a lesser-known gem: %B.

If Bollinger Bands are the map, %B is the GPS — it tells you exactly where price is, relative to the bands, at any given time. This extra precision can help you spot breakouts, reversals, and trend confirmations faster.

What is %B?

%B measures the position of the last closing price within the Bollinger Band range.

%B = 1.0 → Price is exactly at the upper Bollinger Band.

%B = 0.0 → Price is exactly at the lower Bollinger Band.

%B > 1.0 → Price is above the upper band (potential breakout or overbought).

%B < 0.0 → Price is below the lower band (potential breakdown or oversold).

Why Use %B Instead of Just the Bands?

While the bands themselves are great for visual trading, %B turns them into a precise numeric oscillator that’s perfect for:

Coding trading systems (like in WinWayCharts’s Expert Design Studio).

Screening for setups in thousands of stocks.

Backtesting with exact entry/exit rules rather than “eyeballing” the chart.

Five Ways to Use %B in Trading

1. Overbought/Oversold Mean Reversion

Buy when %B < 0.05 (price hugging lower band) and momentum turns up.

Sell when %B > 0.95 (price hugging upper band) and momentum turns down.

2. Trend Breakouts

Buy when %B crosses above 1.0 (price breaks above upper band in an uptrend).

Sell when %B crosses below 0.0 (price breaks below lower band in a downtrend).

3. Band “Walks”

In strong trends, price can “walk” the band.

In an uptrend, %B will often stay above 0.8 for extended periods.

In a downtrend, %B will often stay below 0.2.

For WinWayCharts TradingExpert Pro, we’ll create an EDS strategy that looks for all these setups and generates two indicators.

%B as a histogram in Charts, and a Walk the BBands indicator, where we’ll create upper and lower thresholds, where we can see %B stays above or below these thresholds for several days.

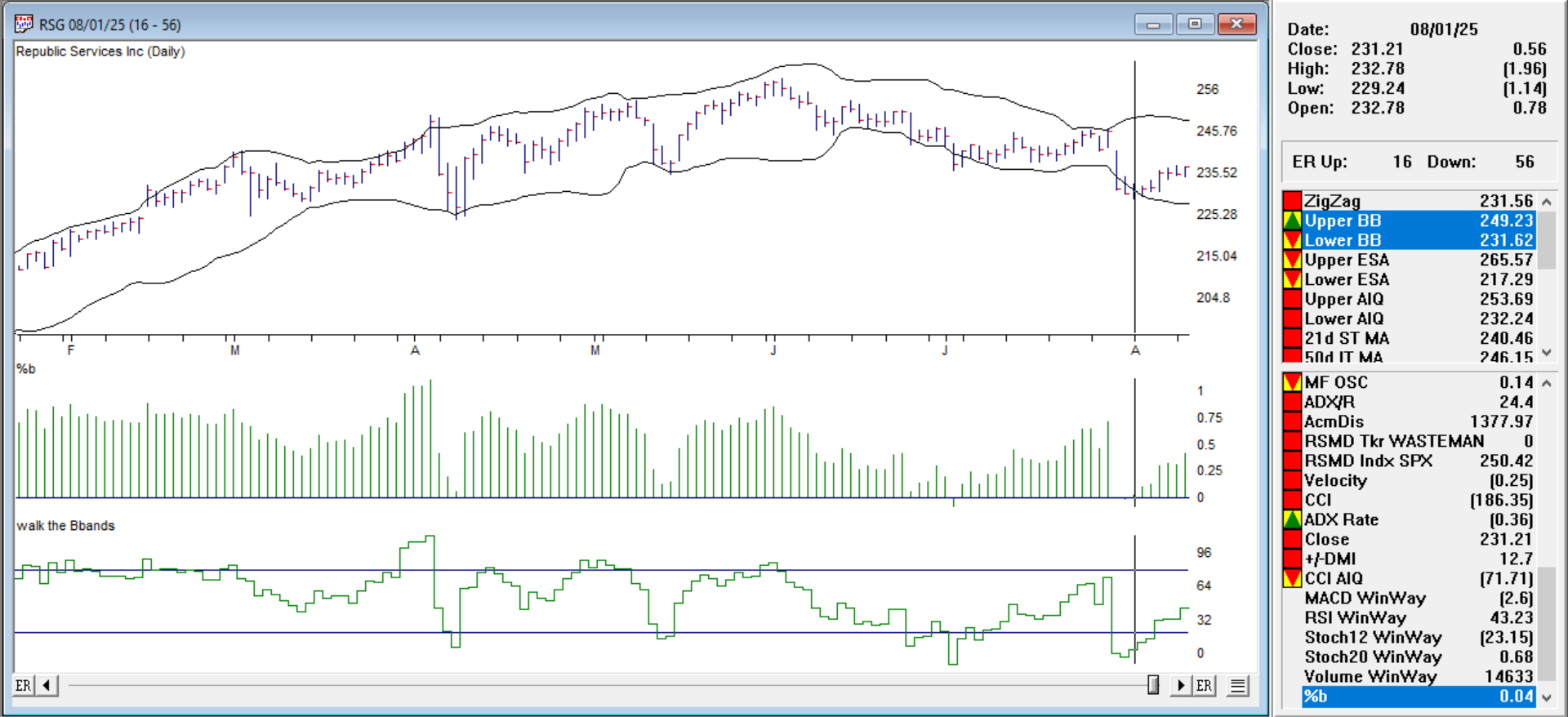

Example Setups from the EDS scan 8-1-2025

Buy when %B < 0.05 (price hugging lower band) and momentum turns up. Ticker RSG %B histogram is 0.05 8-1-25, prices moved moderately up.

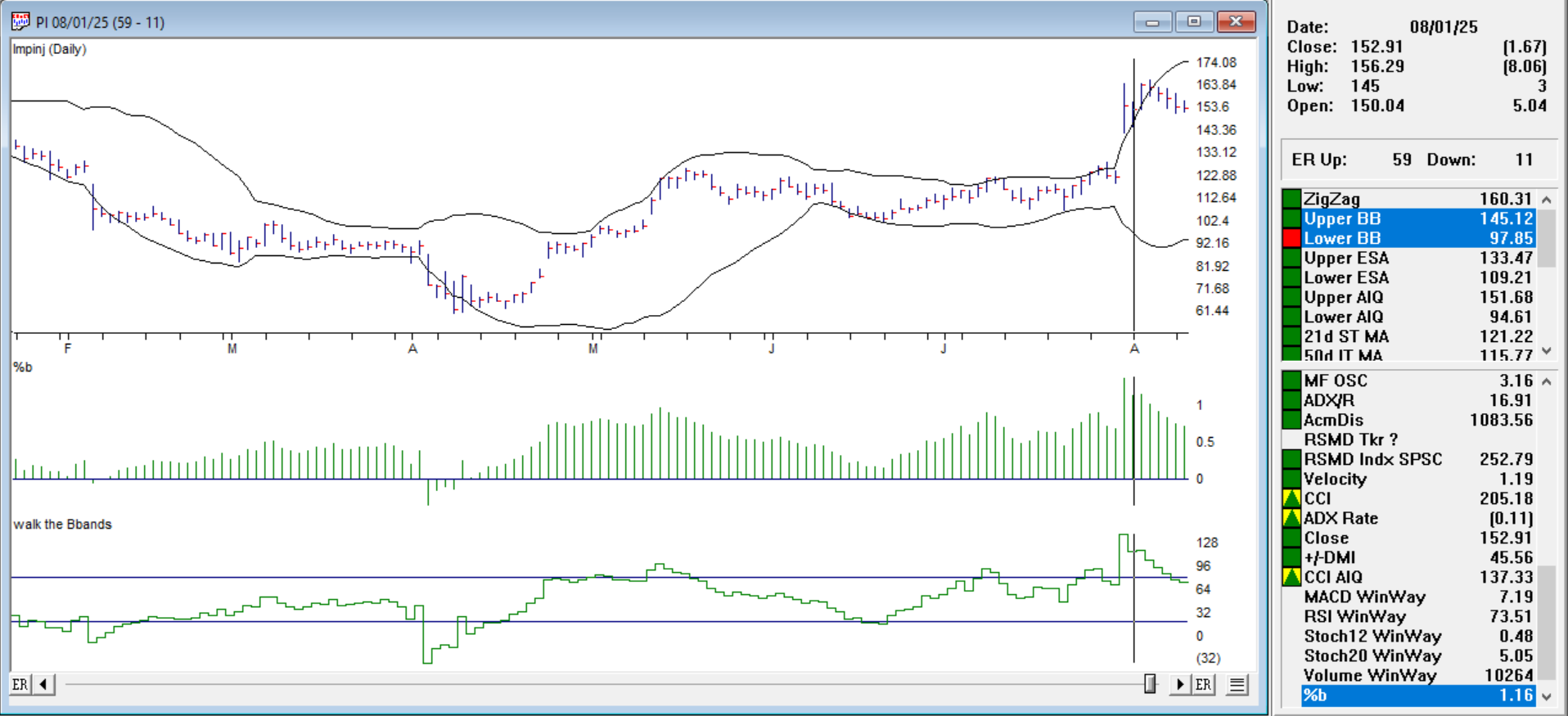

Sell when %B > 0.95 (price hugging upper band) and momentum turns down. Ticker PI %B histogram is 1.16, prices turned down.

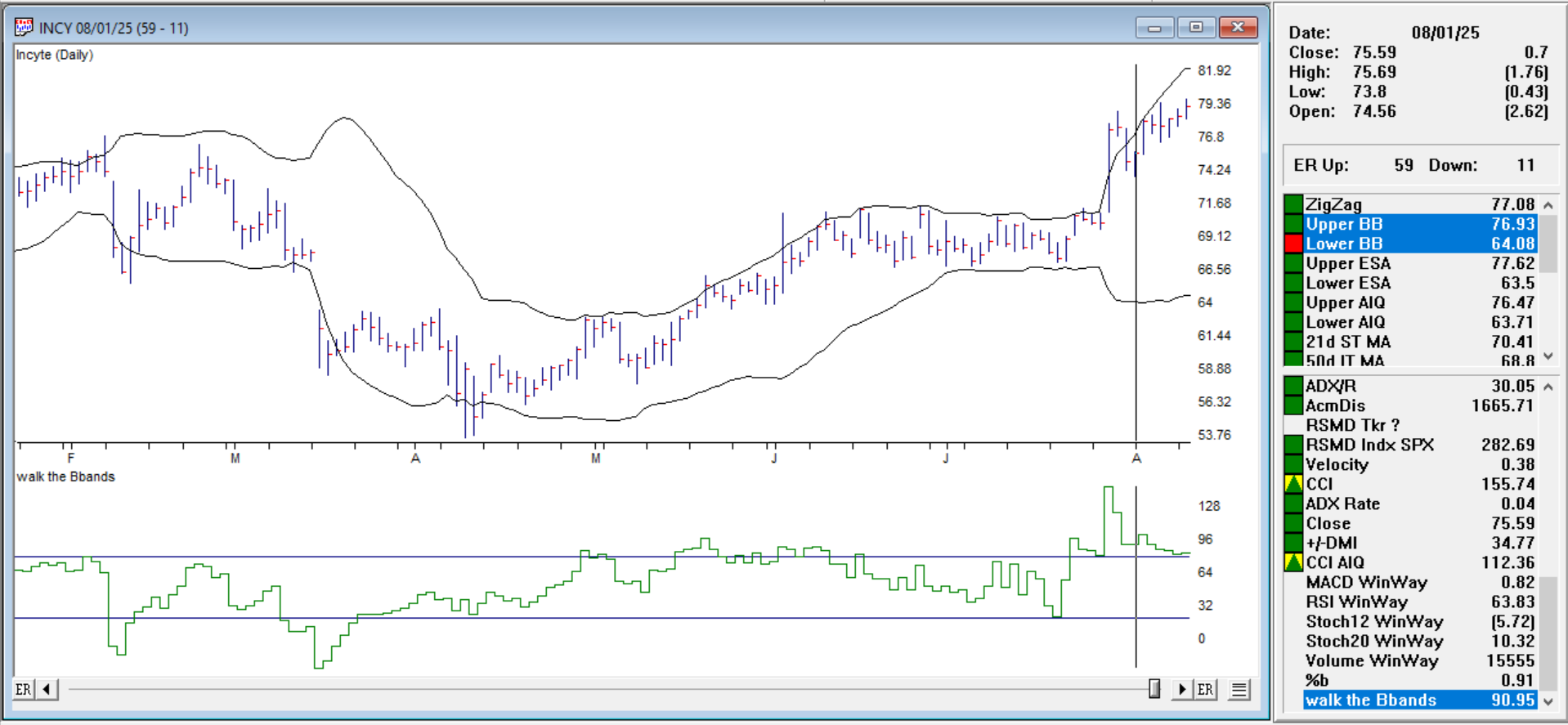

Walk the band up. In an uptrend, %B will often stay above 0.8 for extended periods. Ticker INCY shows above our 80 line in the Walk the BBands indicator and continues to do so.

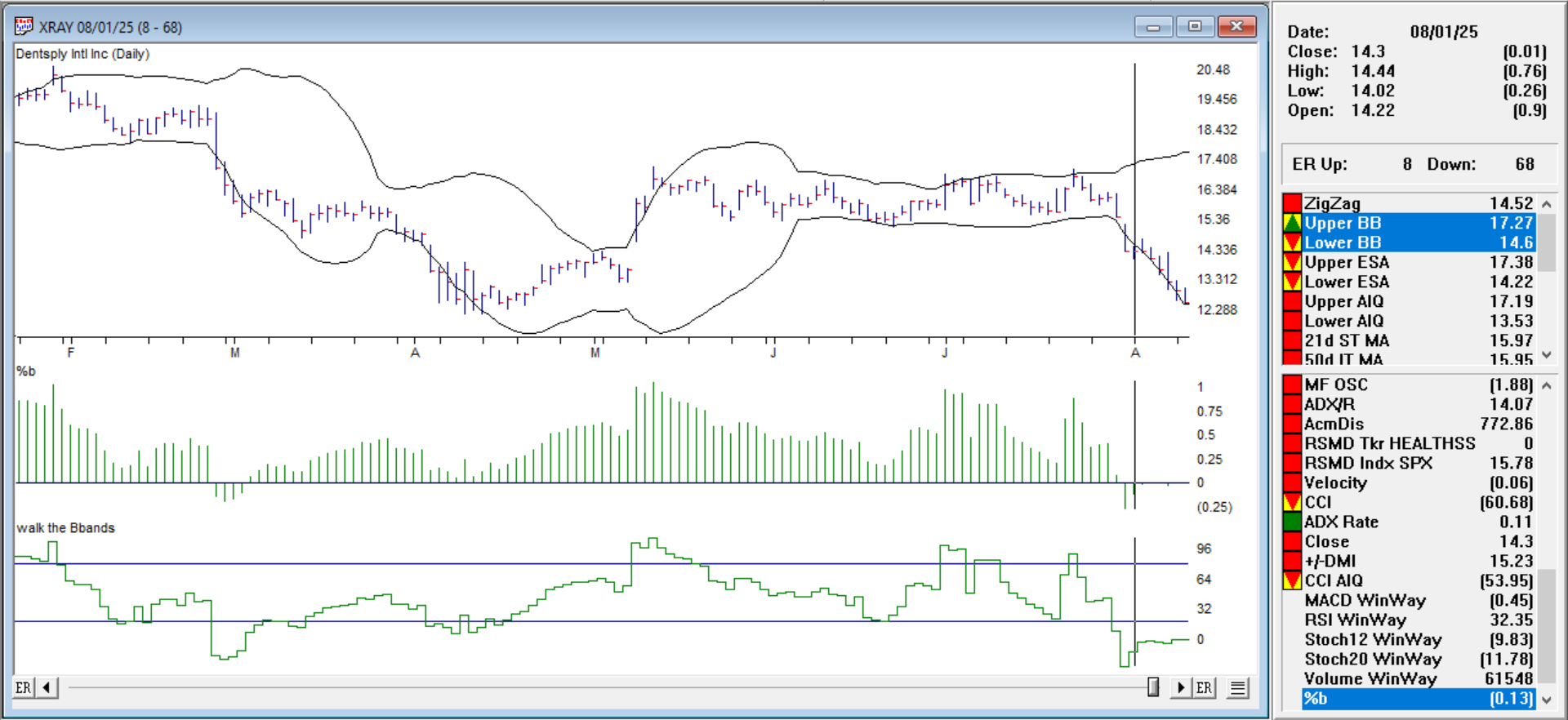

Walk the band down. In a downtrend, %B will often stay below 0.2. Ticker XRAY shows below our 20 line in the Walk the BBands indicator and continues to do so.

Click here to download this zipped EDS file. Locate the Bollinger%25B.zip file usually in your downloads folder and extract the Bollinger%25B.EDS file to your /wintes32/EDS strategies folder.

The code is below

EDS code

! — How to Use the %B Indicator for Smarter Trading

! — When John Bollinger introduced Bollinger Bands in the 1980s, traders gained

! — a powerful visual tool for understanding market volatility and potential turning points.

! — It tells you exactly where price is, relative to the bands, at any given time.

! — This extra precision can help you spot breakouts, reversals, and trend confirmations faster.

Periods is 20.

Multiplier is 2.

! Step 1: Moving Average of Close

MA20 is simpleavg([close],Periods).

! Step 2: Squared Deviations from MA

Deviation is ([close] - MA20) * ([close] - MA20).

! Step 3: Average of Squared Deviations

Var20 is simpleavg(Deviation,Periods).

! Step 4: Square Root to get Standard Deviation

SD20 is sqrt(Var20).

! Step 5: Upper and Lower Bands

UpperBand is MA20 + Multiplier * SD20.

LowerBand is MA20 - Multiplier * SD20.

! Step 6: %B Calculation

PercentB is ([close] - LowerBand) / (UpperBand - LowerBand).

! — Buy when %B < 0.05 (price hugging lower band) and momentum turns up.

BuyReversal if PercentB < 0.05 and [close] > val([close],1).

! — Sell when %B > 0.95 (price hugging upper band) and momentum turns down.

SellReversal if PercentB > 0.95 and [close] < val([close],1).

! — Buy when %B crosses above 1.05 (price breaks above upper band in an uptrend).

BuyBreakout if PercentB > 1.05.

! — Sell when %B crosses below -0.05 (price breaks below lower band in a downtrend).

SellBreakdown if PercentB < -0.05.

! — create an indicator for walking the bands use a one line indicator with upper at 80 lower at 20 by %B x100

walkindicator is PercentB*100.

! — Band “Walks” in strong trends up, price can walk, the band %B will often stay above 0.8 for extended periods.

walkuptoday if walkindicator>80.

walkup1ydy if valresult(walkindicator,1)>80.

walkup2back if valresult(walkindicator,2)>80.

wlkupfor3days if walkuptoday and walkup1ydy and walkup2back.

! — Band “Walks” in strong trends down, price can walk, the band %B will often stay below 0.2 for extended periods.

walkdowntoday if walkindicator<20.

walkdown1ydy if valresult(walkindicator,1)<20.

walkdown2back if valresult(walkindicator,2)<200.

wlkdownfor3days if walkdowntoday and walkdown1ydy and walkdown2back

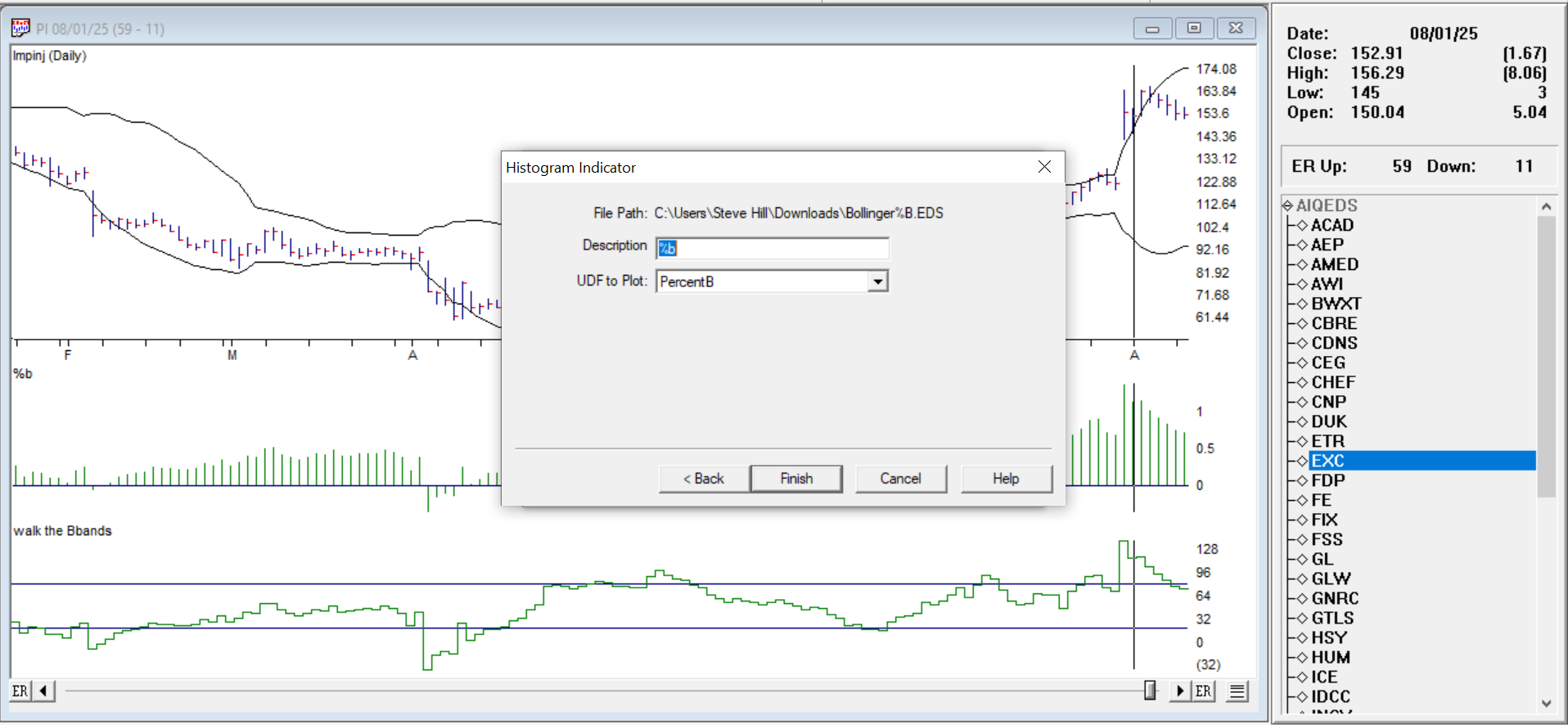

Adding the %B and Walking the BBands Indicator

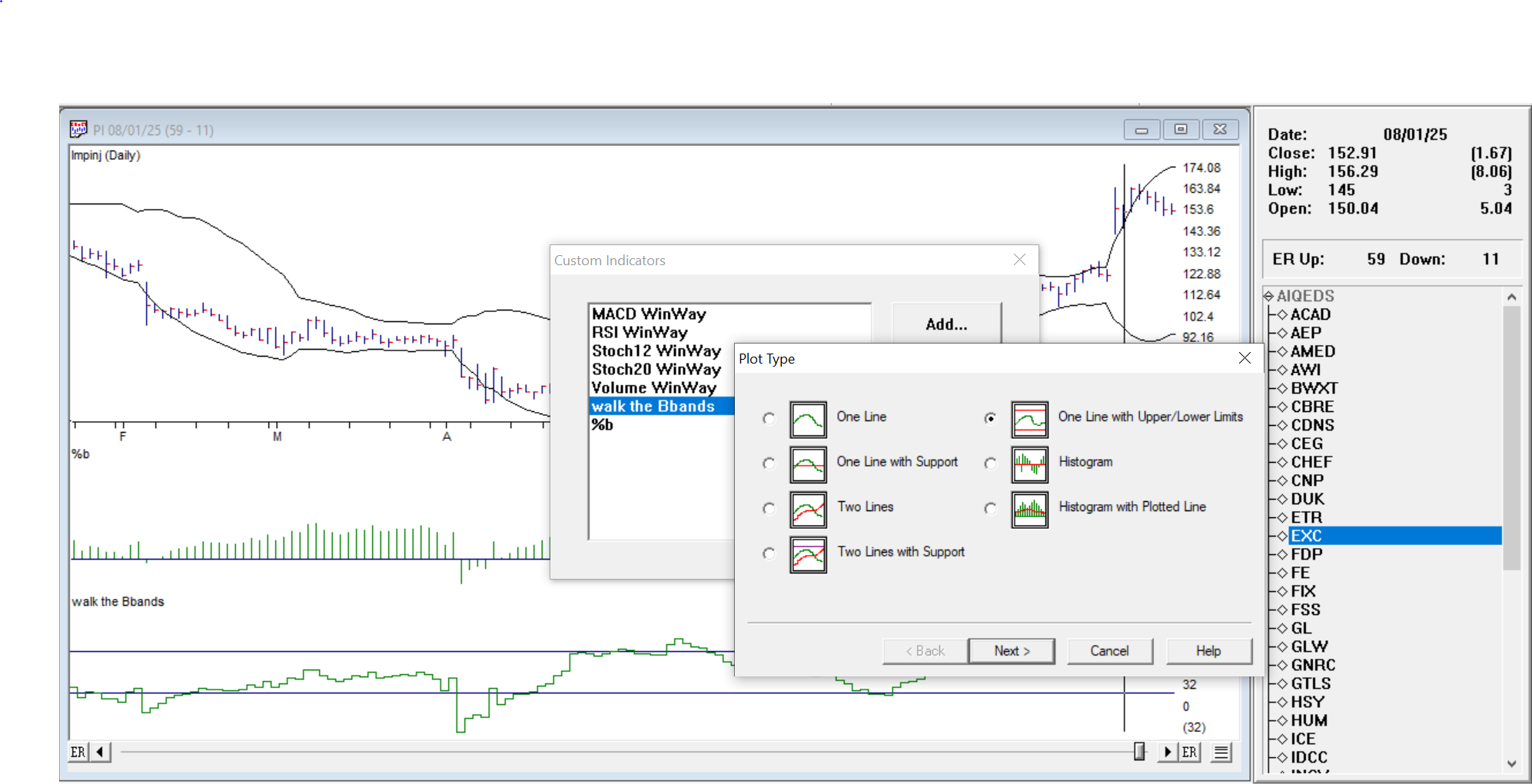

Open WinWayCharts.

Go to Chart → Settings → Indicator Library → EDS Indicators.

Click Add.

Select the Bollinger%25B.EDS file from your /wintes32/EDS strategies folder and click Open.

Choose a Plot Type Histogram for %B

Give it a Description/Name, then choose the UDF to Plot (PercentB).

Click Finish, then Done. Your new indicator now appears in the Indicator Library and can be added to charts like any other study.

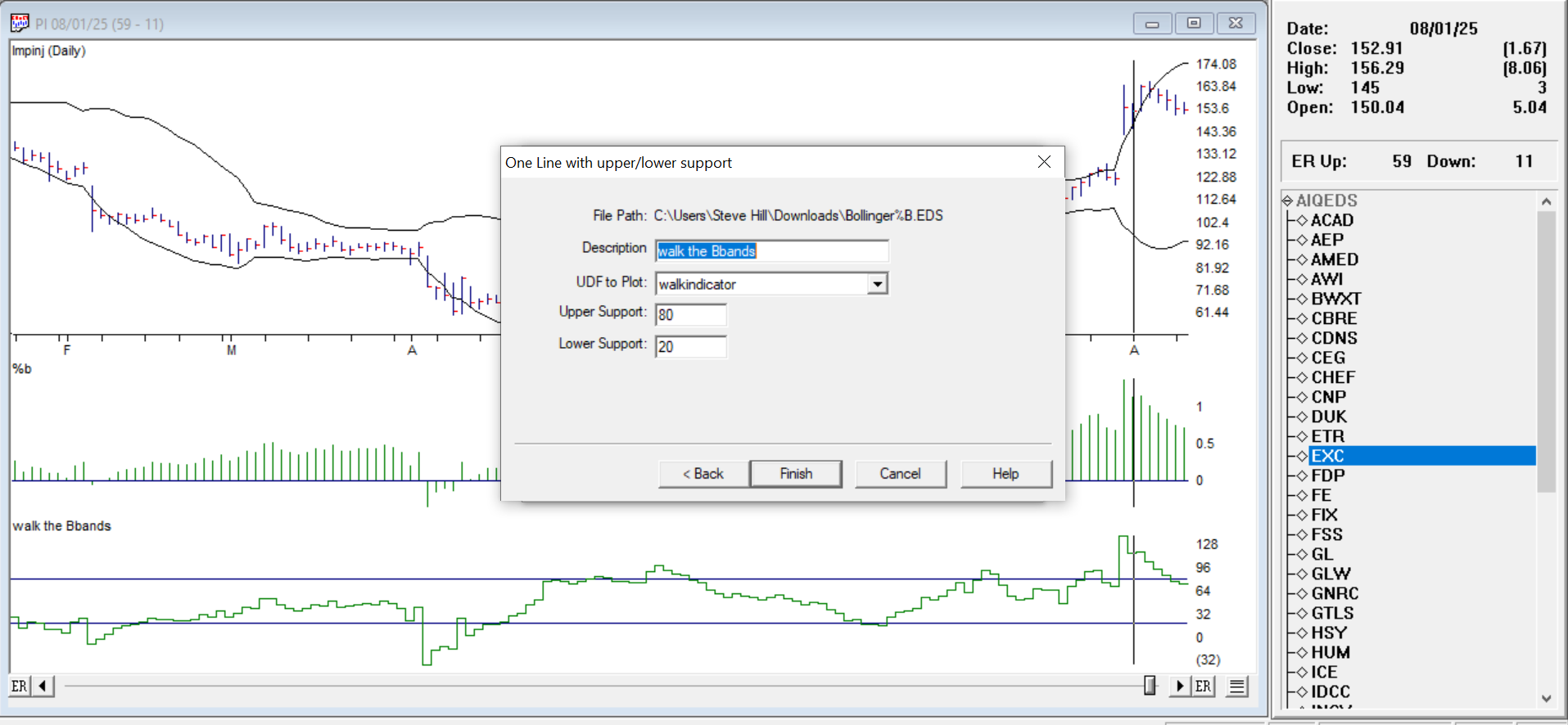

Repeat for the Walk the BBands but select Plot Type One Line with Upper/Lower Limits

Give it a Description/Name, then choose the UDF to Plot (Walkindicator) and select Upper Support 80, Lower Support 20.

Click Finish, then Done. Your new indicator now appears in the Indicator Library and can be added to charts like any other study.

Final Thoughts

%B adds mathematical precision to Bollinger Band analysis. Whether you’re hunting for reversals, breakouts, or just trying to understand volatility better, %B gives you an exact reading of the price’s location in the band structure.