In this video I’ve covered the last 6 months of up and down Market ratings generated by the Artificial Intelligence system in our TradingExpert Pro analysis platform.

You might also be interested in:

Learn key Technical Skills Essential to Trading Success

6 Video Series – nearly 4 hours of in-depth materials

Includes Seminar Notes in PDF on all sessions except Live Trading

+ BONUS eBook Mind Over Markets

6 in-depth videos

Video 1 – Darren’s Indicators

(56 Minutes).

Case Studies Of Some Of Darren’s Favourite Indicators Focusing On How Each Can Be Used As A Part Of Your Overall Stock Selection Strategy. Stoch12 WinWay, RSi WInWay And MACD WinWay Will Be Covered.

Video 2 – Sector Rotation Overview

(18 Minutes).

The Concept Of Market Sector Rotation Is Widely Accepted. Certain Segments Of The Market Are In Favour During Bull, Bear Market Topping, And Market Bottoming Phases.

Video 3 – Leverage Sector Rotation

(52 Minutes).

We’ll Use WinWayCharts Sector Tools Both To Help Determine Market Direction And To Make Stock Trading Decisions.

Video 4 – Mind Over Markets

(33 Minutes).

In This Session, We’ll Give You The Checklist Of Must-Do’s Required To Trade Successfully And Show You How To Avoid The Pitfalls Of An Undisciplined Trader.

Video 5 – Finding Long And Short ETFs

(18 Minutes).

Using Various Tools And Scans In WinWayCharts You’ll Learn How To Find ETFs In Different Market Segments Both Long And Short. There Are ETFs For Each Sector Of The Market And For Markets Themselves. These Are Often Available On The Long And Short Side Of The Market Or Segment. Less Risky Than Stocks And Yet Still Providing Good Liquidity They Are The Darlings Of The Stock Market.

Session 6 – Live Analysis And Trading

(56 Minutes).

WinWayCharts Putting It All Together This Was a Live Analysis Session Looking For Trading Candidates, Confirming Our Selections With Darren’s Indicators, And Placing Trades And Stops In A Real Trading Account.

As we reflect on the incredible journey of the past 17 years, we’re excited to share a milestone with you. It all began when Darren commissioned the creation of the WinWayCharts TradingExpert Pro trading analysis suite, and since then, we’ve been dedicated to enhancing your trading journey.

We’re thrilled to announce the official release of the new WinWayCharts TradingExpert Pro End-of-day version 2.55! After an extensive testing period with our dedicated testers, we’re confident this upgrade will elevate your trading experience.

Some of you who recently joined us may already have the new version, so no need to download the upgrade again. For others, this is an opportunity to embrace the latest enhancements.

Key Features of TradingExpert Pro 2.55:

Introducing the new Heiken Ashi charting feature

For detailed insights and a step-by-step demonstration, check out the upgrade page on our website

And the best part? This upgrade is entirely FREE of charge!

We’re committed to providing you with tools that not only enhance your client experience but also equip you for success in trading. Here’s to a year of prosperity and successful trading ahead!

The importable EDS file based on John Ehlers’ article in the March 2023 issue of Stocks & Commodities, “Every Little Bit Helps,” can be obtained on request via rdencpa@gmail.com. John notes ‘It’s simple but makes a noticeable improvement: You can reduce noise in the data by using an average of the open and close instead of using only the closing price.’ The code is also available below.

!Every Little Bit Helps

!Author: John F. Ehlers, TASC Mar 2023

!Coded by: Richard Denning, 1/12/2023

!Data Sampling Test

!(c) John Ehlers 2022

!INPUTS:

W1 is 14. !Wilder RSI length

W2 is 14. !Ehlers RSI length

!RSI Wilder code:

U is [close]-val([close],1).

D is val([close],1)-[close].

L1 is 2 * W1 – 1.

AvgU is ExpAvg(iff(U>0,U,0),L1).

AvgD is ExpAvg(iff(D>=0,D,0),L1).

RSIwilder is 100-(100/(1+(AvgU/AvgD))).

!Ehlers RSI code:

OCavg is ([open] + [close])/2.

Uoc is OCavg-valresult(OCavg,1).

Doc is valresult(OCavg,1)-OCavg.

L2 is 2 * W2 – 1.

AvgU2 is ExpAvg(iff(Uoc>0,Uoc,0),L2).

AvgD2 is ExpAvg(iff(Doc>=0,Doc,0),L2).

RSIoc is 100-(100/(1+(AvgU2/AvgD2))).

!CTest is RSIwilder.

!OCTest is RSIoc.

BuyRSIwilder if RSIwilder < 20 and valrule(RSIwilder >= 20,1).

ExitRSIwilder if RSIwilder > 80 or {Position days}>=20.

BuyRSIoc if RSIoc < 20 and valrule(RSIoc >= 20,1).

ExitRSIoc if RSIoc > 80 or {Position days}>=20.

Code for the author’s indicators are set up in the EDS code file. Figure 7 shows the EDS module backtest results using the RSI original indicator. Figure 8 shows the EDS module backtest results using the modified version of the RSI indicator over a 10-year period using NASDAQ 100 stocks. The comparison suggests that some of the metrics improve using the modified version and a few are worse.

The system rules are:

Buy when the RSI crosses down below 20

Sell when the RSI crosses above 80 or after 20 trading days

FIGURE 7: AIQ. This shows example backtest results for classic RSI trading system rules, based on closing data, over a 10-year period using NASDAQ 100 stocks.FIGURE 8: AIQ. This shows example backtest results for the RSI trading system rules, this time based on data that averages the open and close instead of using just the closing price data, over a 10-year period using NASDAQ 100 stocks.

The importable EDS file based on Scott Cong’s article in the May 2023 issue of Stocks & Commodities magazine, “An Adaptive Moving Average For Swing Trading,” can be obtained on request via rdencpa@gmail.com.

In this article, Scott proposes a new adaptive moving average (AMA). It adjusts its parameters automatically according to the volatility of market, tracking price closely in trending movement, and staying flat in congestion areas. The new AMA is well-suited for swing trading.

The code is also available below.

Code for the author’s indicator as shown below is set up in the downloadable EDS code file.

!ADAPTIVE MOVING AVERAGE FOR SWING TRADING

!Author: Scott Cong, TASC May 2023

!Coded by: Richard Denning, 03/14/2023

!INPUTS:

Len is 20.

!CODING ABREVIATIONS:

H is [high].

L is [low].

C is [close].

C1 is val([close],1).

TR is Max(H-L,max(abs(C1-L),abs(C1-H))).

Effort is sum(TR,Len).

Result is highresult(H,Len) – lowresult(L,Len).

alpha is Result / Effort.

beta is 1 – alpha.

DaysInto is ReportDate() – RuleDate().

Stop if DaysInto > Len*2.

stopAMA is iff(stop,C, AMA).

AMA is alpha * [close] + beta * valresult( stopAMA, 1).

ESA is expavg(C,Len).

The figure below shows a chart of Broadcom (AVGO) along with the AMA[20] indicator (the red jagged line) and an exponential moving average indicator [20] (the green smooth line).

If you missed this April 27, 2023 Zoom event, don’t worry, the recording is now available from the link at the end of this post. (FYI it expires on May 10th).

In this 2-hour session, Ray Foreman, UK Director of WinWayCharts covered

Getting Started Right with WinWayCharts – Making the Most of Your WinWayCharts – An hour-long session with UK Director Ray Foreman covering the power features in your WinWayCharts platform – great for new clients and those getting started.

In the second half Steve Hill, founder of WinWayChartss built a list of ETFs to trade just about everything and ran it through analytical tools.

Steve also created data files and list files for the ETFS. These are zipped and available below

ETF data files are here – unzip to your /wintes32/tdata folder. Then go to Data Manager, Utilities, Rebuild Master Ticker List.

ETF List files are here – unzip these files to your /wintes32 folder.

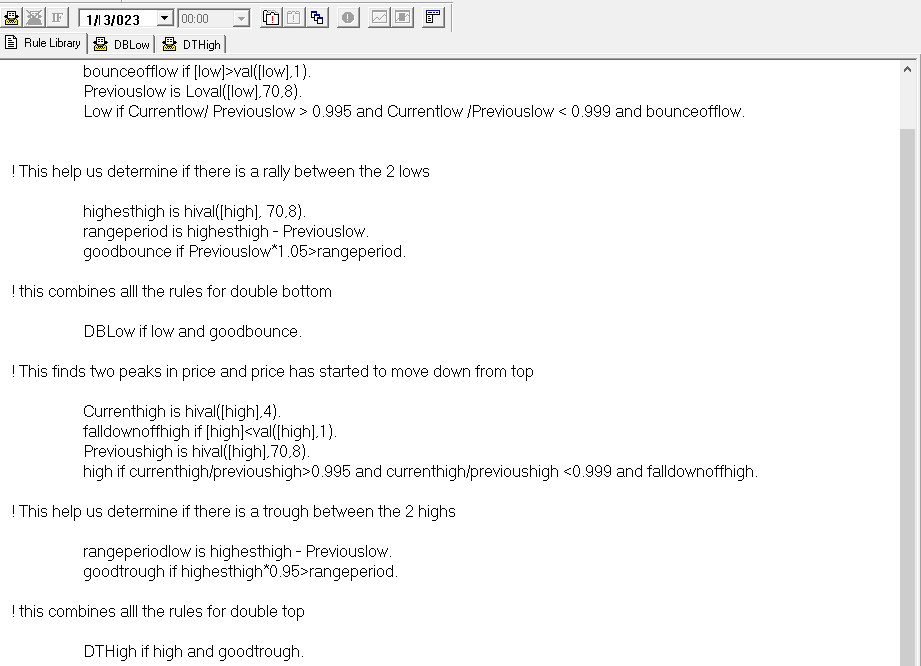

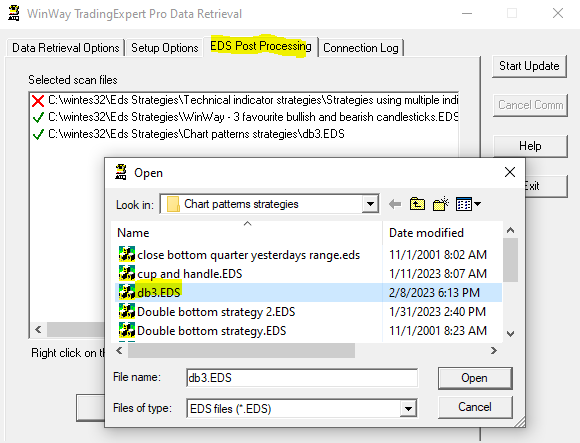

Thank you for your continued support of WinWayCharts services. Recently we have been working on an EDS scan to find double tops and bottoms. We’d like to share with you the progress and how to add this to your WinWayCharts. This is the code used in the scan (you don’t need to know the code but it’s there for your information).

There’s always room for improvement, but you can get a hold of this scan. This file is available for download from here

This may save to a download folder on your system. We suggest you move it to the path C:/wintes32/EDS strategies/Chart Pattern Strategies folder.

To run this strategy automatically after your nightly download of data

– Open Data Retrieval, and select the EDS Post Processing tab.

– Select add, and in the Open, Look in C:/wintes32/EDS strategies/Chart Pattern Strategies folder for db3.EDS

– Select Open and the strategy will run every night for you.

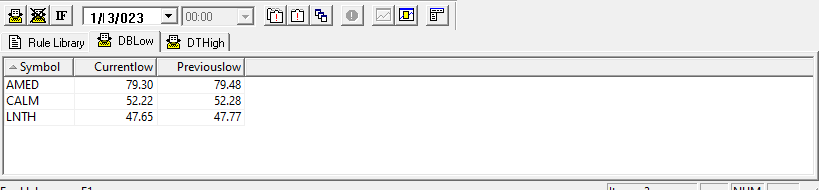

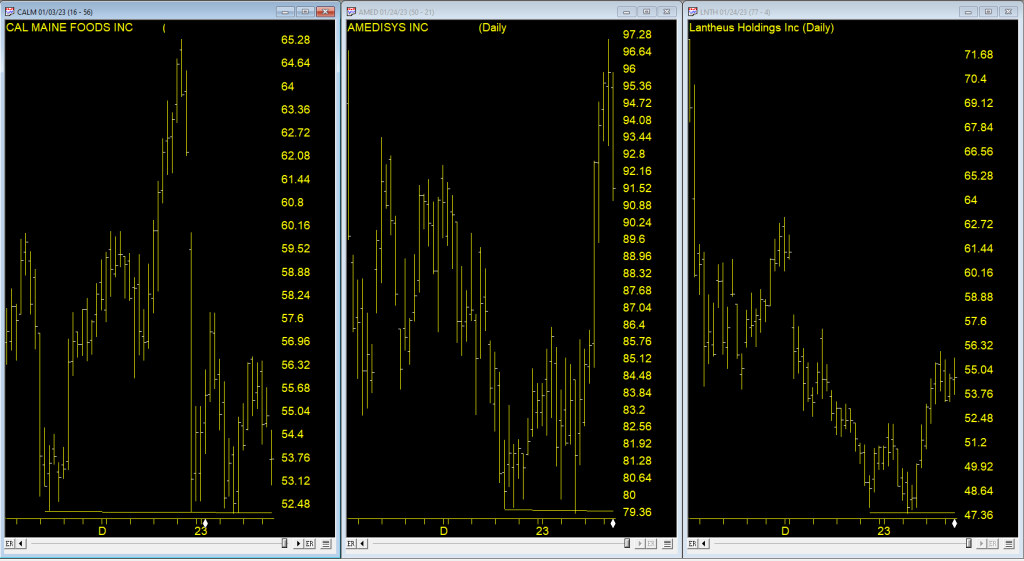

Here’s the results on the Sp1500 run on 1/3/2023

While not perfect, we hope this scan will be of use to you in your trading process.

In her article in the December 2022 issue of Stocks and Commodities, “Short-Term Continuation And Reversal Signals,” Barbara Star describes modifications to the classic directional movement indicator (DMI) and commodity channel index (CCI) that can aid in more easily identifying price reversals and continuations in a trend. Traditionally, the DMI is comprised of two lines: a positive line (+DI) and negative line (−DI).

In her article, Star creates a DMI oscillator by subtracting −DI from +DI. Historically, the DMI uses a default length of 14. In the article, this has been shortened to 10. The CCI has also been adjusted in the article to use a length of 13 instead of the usual 14 or 20. The oscillator is setup using an AIQ Color Study

The importable WinWayCharts EDS file can be obtained on request via email to info@TradersEdgeSystems.com. The code is also shown here:

! Short-Term Continuation And Reversal Signals

! Author: Barbara Star, TASC Dec 2022 ! Coded by: Richard Denning, 10/21/2022

C is [close].

H is [high].

L is [low].

H1 is valresult(H,1).

H2 is valresult(H,2).

L1 is valresult(L,1).

L2 is valresult(L,2).

GreenDMI if [DirMov] > 0.

RedDMI if [DirMov] < 0.

StartOfDownTrend if C < simpleavg(C,18) and [DirMov] < 0 and H < H1 and H1 > H2.

StartOfUpTrend if C >= simpleavg(C,18) and [DirMov] >= 0 and L > L1 and L1 < L2.

GreenTrend if C >= simpleavg(C,18) and [DirMov] >= 0.

RedTrend if C < simpleavg(C,18) and [DirMov] < 0.

Code for the author’s color study is set up in the WinWayCharts EDS code file. Figure 7 shows the color studies set up in the charts module. Figure 8 shows the color studies on a chart of Apple, Inc. (AAPL). The black bars are potential entry points in the downtrend.

FIGURE 7: WinWayCharts. The color bar setup in the charts module is demonstrated.

FIGURE 8: WinWayCharts This shows an example of the color studies applied to a chart of Apple, Inc. (AAPL) with a DMI histogram and an 18-bar simple moving average.

it’s been a challenging market this year, and making trading decisions has never been easy. Which direction the market is likely to move plays a huge part in stock trading decisions.

The Expert Rating system on the market with its combination of 400 rules on the Dow 30 index and the NYSE internals has always provided us an early indication of direction changes.

No system is infallible, and when the Expert System on the market was created, we noticed that ratings of 95 or higher to the upside or downside (maximum rating is 100 btw) were significant. We also noticed a marked improvement in the accuracy of the ratings if we used a confirmation technique with a momentum indicator.

After much research, we discovered that the Phase Indicator (a version of a MACD histogram) was the most accurate tool to confirm high ratings.

*** Here’s how we use Phase to confirm a high Expert Rating. ***

When a rating of 95 up or 95 down is triggered on the market, we look for the Phase histogram to change direction. The change in direction must be to the direction of the rating. This change does not have to happen on the day of the rating, but it must occur within 2 to 3 days on either side of the rating day.

If the Phase does not change direction, the rating is considered not confirmed.

This short video analysis of the last 4 ratings shows this process in action.

In this recent Zoom video Steve Hill, founder of WinWayCharts discusses the Group and Sector Reports, using them to identify groups that are moving up. He then uses Darren’s indicators to focus in on potential stock candidates within these groups.

The WinWay TradingExpert Pro Market Timing signals are not a perfect system. If they were no doubt the founders would have kept it secret and traded the signals themselves.

The signals that give us early waring of a change in direction of the market are proprietary. The 400 rules that are used by the Artificial Intelligence inference engine to determine change of market direction use many of the widely known technical tools, read review here.

The rating calculation and the indicators contributing to the ratings have not been changed for many years. A decision was made some years ago to avoid constantly moving the goalposts as the constant optimizing or back fitting erodes the validity of the system.

High ratings to the upside or downside of notice have to be 95 or greater (the maximum is 100). the ratings are considered confirmed when the Phase indicator that is outside of the AI system, changes in the direction of the high rating.

So ratings have fired in the last few months how do we confirm them?

We look for the Phase indicator ( a derivative of MACD) to change in the direction of the signal. This needs to occur within a 3 day window before or after the rating.

The last 2 market timing signals illustrate this nicely.

August 18, 2022 97-2 up signal on the market

The up signal occurred during a a 3 day down period on the uptrend, however the Phase indicator did not change direction (it would need to turn up after going down) within the window for confirmation. This signal is therefore unconfirmed by Phase.

August 22, 2022 down signal on the market

The down signal occurred on 8-22-22. 100 down is the strongest signal the market timing generates. In this case the Phase turned down after a prolonged upward move, on the day before the signal. This is considered a confirmed down signal on the market.

The rules that contributed to 0-100 down on the market

The 100 down signal is the strongest signal the AI system generates. Here are the major technical events that contribute to this rating.

Trend Status has changed to a strong down trend. This indicates that a downward trend has started that may continue in this direction. This is a moderate bearish signal.

The 21 day stochastic has declined below the 80% line and the price phase indicator is decreasing. In this strongly downtrending market this is an indication that the downtrend will continue.

Volume accumulation percentage is decreasing and the 21 day stochastic has moved below the 80% line. In this strongly down market, this is taken as a very strong bearish signal that could be followed by a downward price movement.

The exponentially smoothed advance/decline line has turned negative when the up/down volume oscillator and the advance/decline oscillator are already negative. In this market, this is viewed as a bearish signal that could precede a downward price movement.

The up/down volume oscillator has turned negative when the exponentially smoothed advance/decline line and the advance/decline oscillator are already negative. In this market, this is viewed as a bearish signal that could precede a downward price movement.

The new high/new low indicator has reversed to the downside. This is a reliable bearish signal that is often followed by an downward price movement. In this market a continued strong downtrend can be expected.

If you missed this April 27, 2023 Zoom event, don’t worry, the recording is now available from the link at the end of this post. (FYI it expires on May 10th).

If you missed this April 27, 2023 Zoom event, don’t worry, the recording is now available from the link at the end of this post. (FYI it expires on May 10th).