Jan 9, 2014 | Moving averages, Stocks & Commodities Traders Tips

Original article by Ajay Pankhania

AIQ Code by Richard Denning

The code for John Ehlers’ article is not provided for AIQ. Instead I substituted an article from the September 2013 Stocks and Commodities issue by Ajay Pankhania, “Muscle Up Those Averages”.

I thought this basic code might be useful to beginning AIQ Expert Design Studio users as it illustrates how to code multiple versions of the simple and the exponential moving averages as well as the MACD indicator. Also the simple moving average crossover system and the MACD crossover systems are coded.

EDS Code:

!MUSCLE UP THOSE AVERAGES

!Author: Ajay Pankhania, TASC Sept 2013

!Coded by: Richard Denning 11/10/2013

!www.TradersEdgeSystems.com

!INPUTS:

price is [close].

smaLen1 is 50.

smaLen2 is 200.

emaLen1 is 12.

emaLen2 is 26.

emaLen3 is 9.

!CODE FOR SIMPLE MOVING AVERAGE OF PRICE:

SMA1 is simpleavg(price,smaLen1).

SMA2 is simpleavg(price,smaLen2).

!CODE FOR CROSSOVER SYSTEM:

BuySMA if SMA1 > SMA2 and valrule(SMA1 < SMA2,1).

SellSMA if SMA1 < SMA2 and valrule(SMA1 > SMA2,1).

!CODE FOR EXPONENTIAL MOVING AVERAGES (FOR MACD):

EMA1 is expavg(price,emaLen1).

EMA2 is expavg(price,emaLen2).

!CODE FOR MACD:

Fast is EMA1 – EMA2.

Signal is expavg(Fast,emaLen3).

!CODE FOR MACD SYSTEM:

BuyMACD if Fast > Signal and valrule(Fast < Signal,1).

SellMACD if Fast < Signal and valrule(Fast > Signal,1).

Jan 7, 2014 | Uncategorized

If there is one is universally true statement that I can make about trading systems in general and in specific, it is this – they sure are fun when they work.

When I first started trading – back in what I longingly refer to as the “Hair Era” in my life – I figured that I would be a “gut” trader – i.e., I was determined to rely on my keen instincts and intuitive reasoning to decide when to buy and sell based on current market conditions.

That was not fun. After continually getting sucked into the swirling vortex of emotion – not to mention the abject fear associated with seeing your money disappear – I found that I was getting the, um, back of my front so to speak, burned so many times that I was having difficulty, um, sitting down, so to speak.

Eventually I evolved into a systematic trader. Now I am able to sit down much more often. A few strategies that I have developed over the years have stood the test of time and become something of “bread and butter” strategies. And they sure are fun when they work. To wit….

Jay’s Pure Momentum System

In 2001, I published an article in “Technical Analysis of Stocks and Commodities” magazine titled “Trade Sector Funds with Pure Momentum”, which detailed one specific and simple trading method. While in fact this is only one of many sector trading systems that I have developed over the years – and not necessarily the best one – it remains one of my favorites. Probably because it is just so gosh darn simple. When I was young my Momma told me to be a simple kind of man (or was it a Freebird she told me to be?). Well, in any event, here are the “simple kind of rules” using Fidelity Select Sector funds:

– After the close of the last trading day of the month identify the five Fidelity Select Sector funds that have the largest gain over the previous 240 trading days.

– For this system, ignore Select Gold (ticker FSAGX). If FSAGX appears in the top 5 funds then skip it and include the 6th highest rated funds.

– If fewer than five funds showed a gain over the previous 240 trading days, then hold cash in that portion of the portfolio (i.e., if only 3 funds showed a gain, then 60% of the portfolio would be in those funds and 40% of the portfolio would be in cash).

– If you sell more than one fund at the end of a month, then rebalance the proceeds in the new funds being purchased (example, you are selling Funds A and B and buying Funds C and D. You have $12,000 in Fund A and $10,000 in Fund B. Split the difference and put $11,000 each into funds C and D).

And that’s all there is to it.

The Results

Figure 1 displays the annual results of this method.

Figure 1 – Jay’s Pure Momentum Annual Results

Figure 2 displays the current portfolio.

Figure 2 – Jay’s Pure Momentum Current Portfolio

My opinion as to why this system has performed well over the years is, well – what else – simple. The effects of a positive change in the fundamentals for a given industry or sector typically take a long time to play out. Thus, by finding the sectors that are performing well you very often find the sectors that are most likely to continue to perform well for a while.

Figure 3 – 12/31/13 Test (Courtesy: AIQ TradingExpert)

Figure 3 – 12/31/13 Test (Courtesy: AIQ TradingExpert) Figure 4 – Several Current Sector Fund Holdings (Courtesy: AIQ TradingExpert)

Summary

Obviously 2013 was a banner year for this system. There is nothing like a rip roaring bull market to help things along. A couple of caveats:

*First off, sometimes people new to momentum investing will look at the charts in Figure 4 and say “Whoa, these things have already rallied sharply, I’m not jumping into those.” That’s something you’ll have to get over to use this system.

*Secondly, while the long-term yearly numbers look pretty good, there was about a 45% drawdown along the way in 2008. So it is not for the faint of heart.

*One other danger is that some people see +48.8% for the year in 2013 and get it in their head that this will occur again often. History suggests otherwise.

Still, an average annual return of +20.7% since 1990 (versus +8.9% for the S&P 500) isn’t bad – especially for a “Simple Kind of System.”

Best of Good Fortune in 2014.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://www.aiq.com) client

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Jan 7, 2014 | group sector rotation, sector funds

If there is one is universally true statement that I can make about trading systems in general and in specific, it is this – they sure are fun when they work.

When I first started trading – back in what I longingly refer to as the “Hair Era” in my life – I figured that I would be a “gut” trader – i.e., I was determined to rely on my keen instincts and intuitive reasoning to decide when to buy and sell based on current market conditions.

That was not fun. After continually getting sucked into the swirling vortex of emotion – not to mention the abject fear associated with seeing your money disappear – I found that I was getting the, um, back of my front so to speak, burned so many times that I was having difficulty, um, sitting down, so to speak.

Eventually I evolved into a systematic trader. Now I am able to sit down much more often. A few strategies that I have developed over the years have stood the test of time and become something of “bread and butter” strategies. And they sure are fun when they work. To wit….

Jay’s Pure Momentum System

In 2001, I published an article in “Technical Analysis of Stocks and Commodities” magazine titled “Trade Sector Funds with Pure Momentum”, which detailed one specific and simple trading method. While in fact this is only one of many sector trading systems that I have developed over the years – and not necessarily the best one – it remains one of my favorites. Probably because it is just so gosh darn simple. When I was young my Momma told me to be a simple kind of man (or was it a Freebird she told me to be?). Well, in any event, here are the “simple kind of rules” using Fidelity Select Sector funds:

– After the close of the last trading day of the month identify the five Fidelity Select Sector funds that have the largest gain over the previous 240 trading days.

– For this system, ignore Select Gold (ticker FSAGX). If FSAGX appears in the top 5 funds then skip it and include the 6th highest rated funds.

– If fewer than five funds showed a gain over the previous 240 trading days, then hold cash in that portion of the portfolio (i.e., if only 3 funds showed a gain, then 60% of the portfolio would be in those funds and 40% of the portfolio would be in cash).

– If you sell more than one fund at the end of a month, then rebalance the proceeds in the new funds being purchased (example, you are selling Funds A and B and buying Funds C and D. You have $12,000 in Fund A and $10,000 in Fund B. Split the difference and put $11,000 each into funds C and D).

And that’s all there is to it.

The Results

Figure 1 displays the annual results of this method.

Figure 1 – Jay’s Pure Momentum Annual Results

Figure 2 displays the current portfolio.

Figure 2 – Jay’s Pure Momentum Current Portfolio

My opinion as to why this system has performed well over the years is, well – what else – simple. The effects of a positive change in the fundamentals for a given industry or sector typically take a long time to play out. Thus, by finding the sectors that are performing well you very often find the sectors that are most likely to continue to perform well for a while.

Figure 3 – 12/31/13 Test (Courtesy: AIQ TradingExpert)

Figure 4 – Several Current Sector Fund Holdings (Courtesy: AIQ TradingExpert)

Summary

Obviously 2013 was a banner year for this system. There is nothing like a rip roaring bull market to help things along. A couple of caveats:

*First off, sometimes people new to momentum investing will look at the charts in Figure 4 and say “Whoa, these things have already rallied sharply, I’m not jumping into those.” That’s something you’ll have to get over to use this system.

*Secondly, while the long-term yearly numbers look pretty good, there was about a 45% drawdown along the way in 2008. So it is not for the faint of heart.

*One other danger is that some people see +48.8% for the year in 2013 and get it in their head that this will occur again often. History suggests otherwise.

Still, an average annual return of +20.7% since 1990 (versus +8.9% for the S&P 500) isn’t bad – especially for a “Simple Kind of System.”

Best of Good Fortune in 2014.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://www.aiq.com) client

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Jan 7, 2014 | Uncategorized

I usually run a seasonal analysis at the beginning of the trading month to look for consistent seasonal behavior in stocks. I also run this same analysis for the Santa Claus rally and other notable seasonal times.

To be brief. I look at the remainder of the January’s trading for my database of stocks. I look back 8 years to see if there are any stocks that consistent trade the same way during the analysis period for each of the 8 years. I compare to the SPY for the same period, so I can be sure there’s little or no market bias (SPY average for this test period was -1.07%)

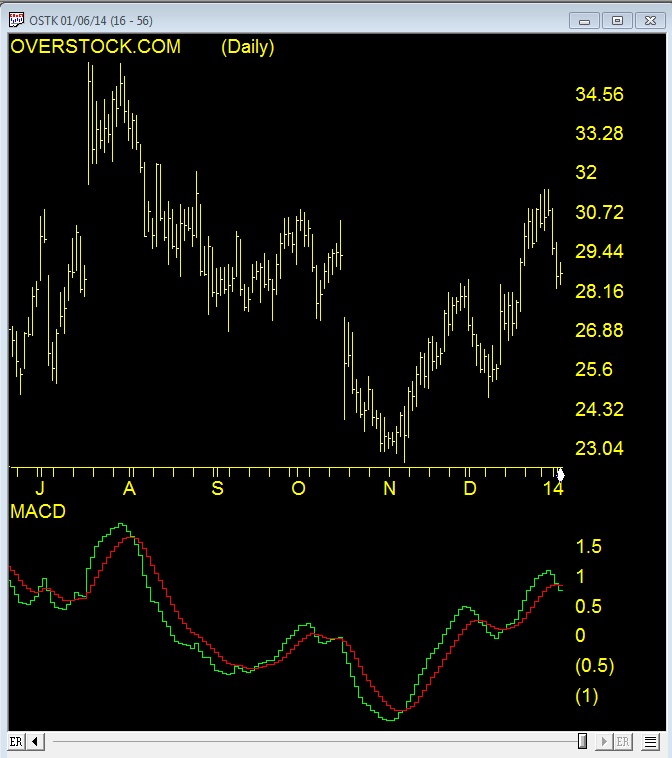

For the remainder of January, only one stock made it to the list on the negative side. This stock was down for the remainder of January for each of the last 8 years. The stock is Overstock.com [OSTK].

Here are the results

OSTK return for the remainder of January

Jan-13 -10.28

Jan-12 -13.65

Jan-11 -7.05

Jan-10 -10.99

Jan-09 -0.18

Jan-08 -30.93

Jan-07 -1.22

Jan-06 -14.13

avg -11.16

I’m always cautious when there are extreme figures in one or two years, as these distort the average. The median for OSTK though is roughly -10% so that still makes it attractive to me. Of course there are no guarantees but so far January 2014 has started as a loser for OSTK

Jan 7, 2014 | retail stocks, Seasonality

I usually run a seasonal analysis at the beginning of the trading month to look for consistent seasonal behavior in stocks. I also run this same analysis for the Santa Claus rally and other notable seasonal times.

To be brief. I look at the remainder of the January’s trading for my database of stocks. I look back 8 years to see if there are any stocks that consistent trade the same way during the analysis period for each of the 8 years. I compare to the SPY for the same period, so I can be sure there’s little or no market bias (SPY average for this test period was -1.07%)

For the remainder of January, only one stock made it to the list on the negative side. This stock was down for the remainder of January for each of the last 8 years. The stock is Overstock.com [OSTK].

Here are the results

OSTK return for the remainder of January

Jan-13 -10.28

Jan-12 -13.65

Jan-11 -7.05

Jan-10 -10.99

Jan-09 -0.18

Jan-08 -30.93

Jan-07 -1.22

Jan-06 -14.13

avg -11.16

I’m always cautious when there are extreme figures in one or two years, as these distort the average. The median for OSTK though is roughly -10% so that still makes it attractive to me. Of course there are no guarantees but so far January 2014 has started as a loser for OSTK

Jan 6, 2014 | Uncategorized

The treasury bond market has showed a strong seasonal tendency to perform poorly during the early part of the year. People often ask me “why” this would be so. In fact I get that question often enough to make me wish I had a good answer. Alas, as a proud graduate of “The School of Whatever Works”, I can only repeat our school motto, which is “Whatever!”

Two Early Year Trends in T-Bonds: Part 1

First let’s look at the performance of t-bond futures between the end of the first trading day of the new year and the 14th trading day of February starting in 1978. Figure 1 displays the performance achieved by an (extremely stubborn and not terribly astute) investor who held a long position in t-bond futures during this time period every year.

Figure 1 – Long t-bond futures from on January Trading Day 1 through February Trading Day 14 (1978-present)

Figure 1 – Long t-bond futures from on January Trading Day 1 through February Trading Day 14 (1978-present)

All told, the loss came to -$49,511 (excluding any slippage and/or commissions). Of course, like all seasonal trends there is never any guarantee that the trend will hold true the next time around. For the record the Jan TD 1 through Feb TD 14 period saw T-bonds:

– Gain 10 times

– Lose 25 times

– Breakeven 1 time

Each point movement in t-bond futures is worth $1,000

– The median gain during up years was +$2,234

– The median loss during down years was -$2,406

– The largest gain was $6,937 in 2000.

– The largest loss was -$15,281 in 1980.

So basically, t-bonds gained 28% of the time, and lost or broke even 72% of the time, and the median loss was slightly greater than the median gain.

Two Early Year Trend in T-Bonds: Part 2

Let’s look next at the net performance for t-bonds during the first four months of the calendar year. Typically, after bonds sink into mid-February there is a bounce in the second half of February. But for our test we will just consider the results achieved by holding a long position in t-bonds from December 31st each year through the end of April. These results appear in Figure 2.

Figure 2 – Long t-bond futures December 31st through April 31st

Figure 2 – Long t-bond futures December 31st through April 31st

All told, the loss came to -$66,389 (excluding any slippage and/or commissions). Of course, like all seasonal trends there is never any guarantee that the trend will hold true the next time around. For the record the Dec 31st to Apr 30th period saw T-bonds:

– Gain 16 times

– Lose 20 times

Each point movement in t-bond futures is worth $1,000

– The median gain during up years was +$1,797

– The median loss during down years was -$4,813

– The largest gain was $13,968 in 1986.

– The largest loss was -$11,313 in 1994.

In reality, the January through April time frame has seen t-bonds show a loss only 56% of the time. So this trend is absolutely by no means a sure thing, so the one thing you should absolutely not do is get it in your head that t-bonds are bound to decline between now and the end of April.

The key thing to note regarding this trend is that the median “down” year has witnessed a decline that is 2.7 times larger than the median gain shown during the “up” years. So the key is simply to recognize the potential danger.

Summary

With t-bonds presently quite oversold, it is a little difficult to jump on the bearish bandwagon at the moment (in fact, bonds are rallying nicely as I write here on the first trading day of the year). And as I have tried to make clear, a decline in t-bond prices during either of both of the highlighted periods is by no means a sure thing. Still, this little bit of history suggests that getting wildly bullish on t-bonds may not be the best strategy.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://www.aiq.com) client

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Jan 6, 2014 | bonds

The treasury bond market has showed a strong seasonal tendency to perform poorly during the early part of the year. People often ask me “why” this would be so. In fact I get that question often enough to make me wish I had a good answer. Alas, as a proud graduate of “The School of Whatever Works”, I can only repeat our school motto, which is “Whatever!”

Two Early Year Trends in T-Bonds: Part 1

First let’s look at the performance of t-bond futures between the end of the first trading day of the new year and the 14th trading day of February starting in 1978. Figure 1 displays the performance achieved by an (extremely stubborn and not terribly astute) investor who held a long position in t-bond futures during this time period every year.

Figure 1 – Long t-bond futures from on January Trading Day 1 through February Trading Day 14 (1978-present)

All told, the loss came to -$49,511 (excluding any slippage and/or commissions). Of course, like all seasonal trends there is never any guarantee that the trend will hold true the next time around. For the record the Jan TD 1 through Feb TD 14 period saw T-bonds:

– Gain 10 times

– Lose 25 times

– Breakeven 1 time

Each point movement in t-bond futures is worth $1,000

– The median gain during up years was +$2,234

– The median loss during down years was -$2,406

– The largest gain was $6,937 in 2000.

– The largest loss was -$15,281 in 1980.

So basically, t-bonds gained 28% of the time, and lost or broke even 72% of the time, and the median loss was slightly greater than the median gain.

Two Early Year Trend in T-Bonds: Part 2

Let’s look next at the net performance for t-bonds during the first four months of the calendar year. Typically, after bonds sink into mid-February there is a bounce in the second half of February. But for our test we will just consider the results achieved by holding a long position in t-bonds from December 31st each year through the end of April. These results appear in Figure 2.

Figure 2 – Long t-bond futures December 31st through April 31st

All told, the loss came to -$66,389 (excluding any slippage and/or commissions). Of course, like all seasonal trends there is never any guarantee that the trend will hold true the next time around. For the record the Dec 31st to Apr 30th period saw T-bonds:

– Gain 16 times

– Lose 20 times

Each point movement in t-bond futures is worth $1,000

– The median gain during up years was +$1,797

– The median loss during down years was -$4,813

– The largest gain was $13,968 in 1986.

– The largest loss was -$11,313 in 1994.

In reality, the January through April time frame has seen t-bonds show a loss only 56% of the time. So this trend is absolutely by no means a sure thing, so the one thing you should absolutely not do is get it in your head that t-bonds are bound to decline between now and the end of April.

The key thing to note regarding this trend is that the median “down” year has witnessed a decline that is 2.7 times larger than the median gain shown during the “up” years. So the key is simply to recognize the potential danger.

Summary

With t-bonds presently quite oversold, it is a little difficult to jump on the bearish bandwagon at the moment (in fact, bonds are rallying nicely as I write here on the first trading day of the year). And as I have tried to make clear, a decline in t-bond prices during either of both of the highlighted periods is by no means a sure thing. Still, this little bit of history suggests that getting wildly bullish on t-bonds may not be the best strategy.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://www.aiq.com) client

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Dec 26, 2013 | Uncategorized

Some seasonal trends have shown a tendency to persist through time (hence the use of the word “trend”, I guess). As it turns out we are at the cusp of one of “those times” right now. It is sitting there like a wrapped gift under the tree with our name on it – so let’s not waste any time diving in.

December-January Changeover

The period we will look at encompasses the last 4 trading days of December and the first 3 trading days of the following January. In other words, a contiguous 7 day trading period during which the stock market has showed a tendency to behave in a bullish manner.

Now given the persistence of the recent market run up, many may be a little leery of diving in here. Which I understand. Still, the numbers are what they are, so let’s take a look.

The Test

So as not to make it easy on ourselves, this test begins in December 1933, i.e., in the early days off the great Depression. We will buy the Dow Jones industrials Average at the close of the fifth to last trading day of the year and sell at the close of the third trading day of January. This test assumes no interest is earned while out of the market so that we measure only the performance during the supposedly bullish period.

The Results

Figure 1 displays the growth of $1,000 invested in the Dow every year since 1933 during the seven trading days just described.

Figure 1 – Growth of $1,000 invested in Dow Industrials during bullish 7-day period (1933-present)

Two anecdotal comments from a quick perusal of the graph in Figure 1:

-There is clearly a lower left to upper right trend, which is what we want to see in any equity curve

-It is by no means “perfect”, so a little closer analysis of the numbers may be useful in convincing ourselves that this trend might actually be useful. So in order to gain some perspective, let’s compare the performance of the Dow during this time period versus Dow performance for all trading days.

A few figures of note:

-System average daily performance is +0.22% versus +0.03% for all trading days (7.53 times greater).

-System median daily performance is +0.17% versus +0.03% for all trading days (4.00 times greater).

-338 out of 560 system trading days showed a gain (60.4%).

-10,946 out of all 20,922 trading days showed a gain (52.3%).

-Average 7-day return only during system days = +1.55%.

-Average 7-day return for all trading days = +0.20%.

-The 7-day system period has showed a gain in 62 of the past 80 years (or 77.5% of the time)

One other thing to note is that returns (and albeit risk) is enhanced by trading leveraged funds such as ticker UDPIX (Profunds UltraDow) or UDOW (ProShares UltraDow30 ETF).

Summary

So is the Dow destined to be higher at the close on January 6, 2014 than it was at the close on December 24th, 2013? Not necessarily. But that would seem to be the way to bet.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://www.aiq.com) client

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Dec 26, 2013 | Seasonality

Some seasonal trends have shown a tendency to persist through time (hence the use of the word “trend”, I guess). As it turns out we are at the cusp of one of “those times” right now. It is sitting there like a wrapped gift under the tree with our name on it – so let’s not waste any time diving in.

December-January Changeover

The period we will look at encompasses the last 4 trading days of December and the first 3 trading days of the following January. In other words, a contiguous 7 day trading period during which the stock market has showed a tendency to behave in a bullish manner.

Now given the persistence of the recent market run up, many may be a little leery of diving in here. Which I understand. Still, the numbers are what they are, so let’s take a look.

The Test

So as not to make it easy on ourselves, this test begins in December 1933, i.e., in the early days off the great Depression. We will buy the Dow Jones industrials Average at the close of the fifth to last trading day of the year and sell at the close of the third trading day of January. This test assumes no interest is earned while out of the market so that we measure only the performance during the supposedly bullish period.

The Results

Figure 1 displays the growth of $1,000 invested in the Dow every year since 1933 during the seven trading days just described.

Figure 1 – Growth of $1,000 invested in Dow Industrials during bullish 7-day period (1933-present)

Two anecdotal comments from a quick perusal of the graph in Figure 1:

-There is clearly a lower left to upper right trend, which is what we want to see in any equity curve

-It is by no means “perfect”, so a little closer analysis of the numbers may be useful in convincing ourselves that this trend might actually be useful. So in order to gain some perspective, let’s compare the performance of the Dow during this time period versus Dow performance for all trading days.

A few figures of note:

-System average daily performance is +0.22% versus +0.03% for all trading days (7.53 times greater).

-System median daily performance is +0.17% versus +0.03% for all trading days (4.00 times greater).

-338 out of 560 system trading days showed a gain (60.4%).

-10,946 out of all 20,922 trading days showed a gain (52.3%).

-Average 7-day return only during system days = +1.55%.

-Average 7-day return for all trading days = +0.20%.

-The 7-day system period has showed a gain in 62 of the past 80 years (or 77.5% of the time)

One other thing to note is that returns (and albeit risk) is enhanced by trading leveraged funds such as ticker UDPIX (Profunds UltraDow) or UDOW (ProShares UltraDow30 ETF).

Summary

So is the Dow destined to be higher at the close on January 6, 2014 than it was at the close on December 24th, 2013? Not necessarily. But that would seem to be the way to bet.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://www.aiq.com) client

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Dec 21, 2013 | Uncategorized

This article presents another twist to the one I posted a few days ago titled “A Trader’s Guide to Buying the Dips”. This article presents a variation known as “Jay’s Pullback System”

First let’s look at the building blocks:

A = S&P 500 daily close

B = 10-day simple moving average of S&P 500 daily close

C = (A – B)

Buy Signal = Variable C declines for 3 or more consecutive days

In a nutshell, if the difference between the S&P 500 index (SPX) and its own 10-day moving average declines for 3 straight days we consider this to be a “pullback”, and thus a buying opportunity.

Trading Rules for Basic System:

When Variable C declines for 3 straight days, buy and hold the S&P 500 Index for 5 trading days. If the decline in Variable C extends itself one or more days, then extend the holding period for that many trading days.

So for example, if Variable C declined for 5 straight trading days, one would buy at the close of the third trading day and then hold for seven trading days

Day Variable C Action Position

1 Down

2 Down

3 Down Buy at close (hold for 5 days)

4 Down Hold (Var. C down again; hold for 5 days) Long

5 Down Hold (Var. C down again; hold for 5 days) Long

6 Up Hold (for 4 days) Long

7 Down Hold (for 3 days) Long

8 Up Hold (for 2 days) Long

9 Down Hold (for 1 day) Long

10 Up Sell at close Long; Flat at close

Figure 1 displays “bullish days for SPX in green. In the lower clip we see the difference between the close and the 10-day moving average (i.e., Variable C). A “bullish” period is signaled when that value declines for 3 straight days

Figure 1 – Basic System bullish days for SPX (Courtesy AIQ TradingExpert)

Figure 1 – Basic System bullish days for SPX (Courtesy AIQ TradingExpert)

Results:

This is a very rudimentary “system” and not suitable for many traders (note this raw system includes no stop-loss provision and does not attempt to filter for and trade with the major trend).

In any event, let’s look at what would have happened if one had followed the rules and held the S&P 500 for 5 trading days following every decline in Variable C of 3 days or more, and earned 1% of annual interest while out of the market. Those results are displayed (along with the growth of $1,000 achieved by buying and holding the S&P 500 Index) in Figure 2.

Figure 2 – Simple Pullback Systems (blue line) versus Buy and Hold (red line) Dec 1987 to present

Figure 2 – Simple Pullback Systems (blue line) versus Buy and Hold (red line) Dec 1987 to present

Results:

-$1,000 invested using this system grew to $13,249 (+1,225%)

-$1,000 invested using buy-and-hold grew to $7,208 (+621%)

So we can reasonably state that these results are pretty good. Can they be improved? Let’s see.

Jay’s Pullback System

With this system we will filter for the trend and at times use leverage.

First we will note if the daily close for the S&P 500 Index is above or below its own 250-day moving average.

If Variable C above declines in value 3 straight days:

-If SPX > 250-day moving average we will buy using leverage of 2-to-1

-If SPX < 250-day moving average we will buy using no leverage

-Interest of 1% per year will be assumed when out of the market.

The results of this test appear in Figure 3.

Figure 3 – Jay’s Pullback System: Growth of $1,000 (blue line) versus buy and hold (red line; Dec 1987-present

Figure 3 – Jay’s Pullback System: Growth of $1,000 (blue line) versus buy and hold (red line; Dec 1987-presentResults:

-$1,000 invested using Jay’s Pullback System grew to $44,541 (+4.354%)

-$1,000 invested using buy-and-hold grew to $7,208 (+621%)

Funds to Use

Mutual Fund: Profunds ticker BLPIX (S&P x 1)

Mutual Fund: Profunds ticker ULPIX (S&P x 2)

ETF: Ticker SPY (S&P 500 x 1)

ETF: Ticker SSO (S&P 500 x 2)

Summary

While the numbers for the leveraged system look pretty good, it should be noted that there are no stop-loss provisions incorporated. Before you decide to run off and trade any system – particularly one that may use leveraged funds or ETFs, you ought to do some homework and make sure you fully understand and can tolerate the risks involved.

Still, the real point of all of this is simply to note that buying on dips is a valid approach to trade the stocks markets.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://www.aiq.com) client

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.