Sep 23, 2013 | Uncategorized

The AIQ code based on Sylvain Vervoort’s article in the September issue of Stocks & Commodities, “Oscillators, Smoothed,” is provided at www.TradersEdgeSystems.com/traderstips.htm and is also shown below.

In the chart of Sanderson Farms (SANF) with a color bar study that shows potential buys (green bars) when both oscillators are moving up and they are both oversold (below 20). It sells (red bars) when both oscillators are moving down and they are both overbought (above 80). The bands shown are based on the modified Bollinger Bands that are used in the calculation of the modified Percent b oscillator. For comparison purposes, I have also provided the formula for John Bollinger’s original Percent b indicator as well as for the original smoothed %K indicator.

!OSCILLATORS, SMOOTHED

!Author: Sylvain Vervoort, TASC Sept 2013

!Coded by: Richard Denning 7/6/13

!www.TradersEdgeSystems.com

!INPUTS:

C is [close].

H is [high].

L is [low].

smaLen is 2.

smoLen is 3.

sdLen is 18.

kLen is 3.

!CODE FOR MODIFIED PERCENT B INDICATOR:

SMA1 is simpleavg(C,smaLen).

SMA2 is simpleavg(SMA1,smaLen).

SMA3 is simpleavg(SMA2,smaLen).

SMA4 is simpleavg(SMA3,smaLen).

SMA5 is simpleavg(SMA4,smaLen).

SMA6 is simpleavg(SMA5,smaLen).

SMA7 is simpleavg(SMA6,smaLen).

SMA8 is simpleavg(SMA7,smaLen).

SMA9 is simpleavg(SMA8,smaLen).

SMA10 is simpleavg(SMA9,smaLen).

rainbow is (5*SMA1 + 4*SMA2 + 3*SMA3 + 2*SMA4

+ SMA5 + SMA6 + SMA7 + SMA8 + SMA9

+SMA10) / 20.

EMA1 is expavg(rainbow,smoLen).

EMA2 is expavg(EMA1,smoLen).

diff is EMA1 – EMA2.

ZLRB is EMA1 + diff.

EMAZ1 is expavg(ZLRB,smoLen).

EMAZ2 is expavg(EMAZ1,smoLen).

EMAZ3 is expavg(EMAZ2,smoLen).

TEMAZ is 3*EMAZ1 – 3*EMAZ2 + EMAZ3.

SDTEMAZ is sqrt(variance(TEMAZ,sdLen)).

TEMAZ18 is valresult(TEMAZ,18).

TEMAZ17 is valresult(TEMAZ,17).

TEMAZ16 is valresult(TEMAZ,16).

TEMAZ15 is valresult(TEMAZ,15).

TEMAZ14 is valresult(TEMAZ,14).

TEMAZ13 is valresult(TEMAZ,13).

TEMAZ12 is valresult(TEMAZ,12).

TEMAZ11 is valresult(TEMAZ,11).

TEMAZ10 is valresult(TEMAZ,10).

TEMAZ9 is valresult(TEMAZ,9).

TEMAZ8 is valresult(TEMAZ,8).

TEMAZ7 is valresult(TEMAZ,7).

TEMAZ6 is valresult(TEMAZ,6).

TEMAZ5 is valresult(TEMAZ,5).

TEMAZ4 is valresult(TEMAZ,4).

TEMAZ3 is valresult(TEMAZ,3).

TEMAZ2 is valresult(TEMAZ,2).

TEMAZ1 is valresult(TEMAZ,1).

WMA18TEMAZ is (18*TEMAZ + 17*TEMAZ1 + 16*TEMAZ2

+ 15*TEMAZ3 + 14*TEMAZ4 + 13*TEMAZ5

+ 12*TEMAZ6 + 11*TEMAZ7 + 10*TEMAZ8

+ 9*TEMAZ9 + 8*TEMAZ10 + 7*TEMAZ11

+ 6*TEMAZ12 + 5*TEMAZ13 + 4*TEMAZ14

+ 3*TEMAZ15 + 2*TEMAZ16 + 1*TEMAZ17 ) /

(18+17+16+15+14+13+12+11+10+9+8+7+6+5+4+3+2+1).

!Plot the following as single line indicator with 50 line:

PBmod is (TEMAZ + 2*SDTEMAZ – WMA18TEMAZ) / (4*SDTEMAZ)*100.

!CODE FOR MODIFIED BOLLIGER BANDS:

BBupMod is TEMAZ + 2*SDTEMAZ. !Plot on chart area

BBdnMod is TEMAZ – 2*SDTEMAZ. !Plot on chart area

!CODE FOR STANDARD PERCENT B:

sdC is sqrt(variance(C,sdLen)).

!For comparison the following is the percent B:

pctB is (C+2*sdC-simpleavg(C,sdLen))/(4*sdC)*100.

!CODE FOR MODIFIED SLOW STOCHASTIC:

typ is (H+L+C)/3.

RBC is (rainbow + typ) / 2.

nom is RBC – lowresult(RBC,kLen).

den is highresult(RBC,kLen) – lowresult(RBC,kLen).

fastKmod is min(100,max(0,100*nom / den)).

Kmod is simpleavg(fastKmod,smoLen).

!CODE FOR STANDARD SLOW STOCHASTIC:

n is (C – lowresult(L,kLen)).

d is (highresult(H,kLen)-lowresult(L,kLen)).

fastK is min(100,max(0,100*n / d)).

slowK is simpleavg(fastK,smoLen).

!COLOR STUDY FOR MODIFIED OSCILLATORS

Green if PBmod > valresult(PBmod,1)

and Kmod > valresult(Kmod,1)

and PBmod < 20 and Kmod < 20.

Red if PBmod < valresult(PBmod,1)

and Kmod < valresult(Kmod,1)

and PBmod > 80 and Kmod > 80.

—Richard Denning

info@TradersEdgeSystems.com

for AIQ Systems

Sep 17, 2013 | Uncategorized

In Figure 1 below you will see a chart of ticker VXX, an ETF that tracks the VIX Index.

Figure 1 – Ticker VXX (Chart courtesy of AIQ TradingExpert)

Given:

- The fact that September and October have historically been the scene of a lot of stock market wreckage.

- That the Fed is due to say “something” about tapering soon

- The fact that VXX is at about its lowest level in years

- And the fact that VXX “spikes” to higher ground when the stock market stumbles.

Does it seem at all possible that VXX might be about ready for its next “spike”? Now understand that that is not a prediction but merely an observation that the possibility seems “ripe”. So it might be time to consider what I sometimes refer to as a “throwaway” trade.

My definition of a “throwaway” trade is one whereby based on the “possibility” of “something” in particular occurring, one enters into a very low cost trade that has the prospect of paying off in a big way based. But do not confuse this with a “lottery ticker” mentality, because the trade is based on some realistic expectation that the “something” might actually occur. Is it really that hard to picture a VIX spike sometime in the September/October timeframe?

So here is one example possibility (though not necessarily a recommendation) using an option on VXX. This trade was found using software at www.OptionsAnalysis.com. It involves simply buying 1 November VXX 14 strike price call option for $161. The particulars appear in Figures 2 and 3.

If VXX were merely to return to its August 30th high of 17.34, this trade would essentially double in value. If “something” really crazy happens and VXX soars to sharply higher levels the profit could be quite a bit more.

Again, I am not saying that VXX is sure to soar between now and the end of November. I’m only saying that I might be willing to risk $161 just in case.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro client

http://jayonthemarkets.com/

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Aug 16, 2013 | Uncategorized

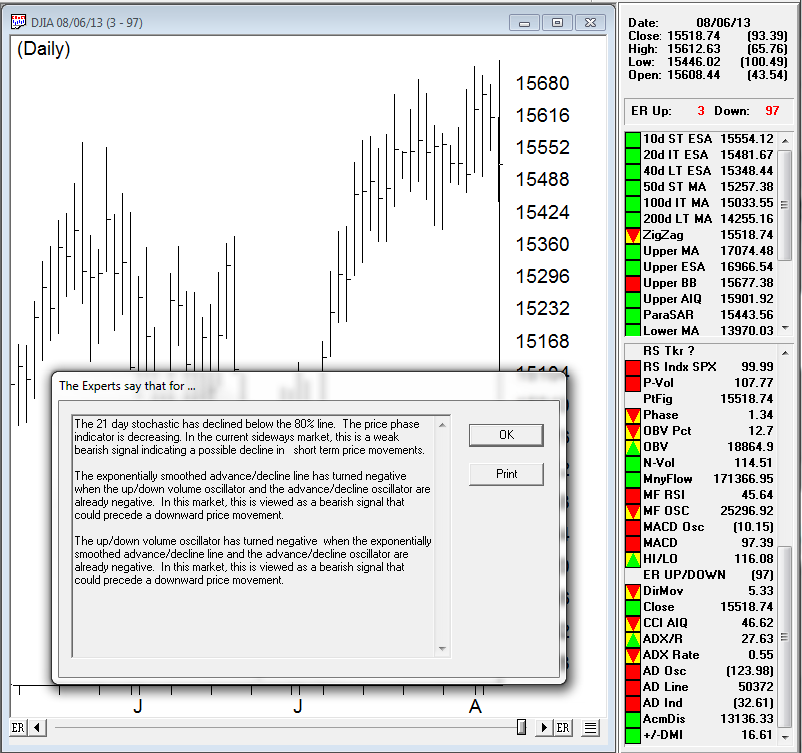

Here’s August 6th chart of the DJIA with the AIQ Experts say…

we had a 3-97 to the downside. The internal technical metrics feeding this rating were as follows

The 21 day stochastic has declined below the 80% line. The price phase indicator is decreasing. In the current sideways market, this is a weak bearish signal indicating a possible decline in short term price movements.

The exponentially smoothed advance/decline line has turned negative when the up/down volume oscillator and the advance/decline oscillator are already negative. In this market, this is viewed as a bearish signal that could precede a downward price movement.

The up/down volume oscillator has turned negative when the exponentially smoothed advance/decline line and the advance/decline oscillator are already negative. In this market, this is viewed as a bearish signal that could precede a downward price movement.

This rating was confirmed by Price Phase indicator moving down the same day. Phase confirmation eliminates rogue ratings as Price Phase is not a part of the AI rating. Sine August 6th the market has corrected more than 400 points, and up ratings were generated, however the Price Phase has continued declining and has not confirmed these ratings.

Jul 17, 2013 | Uncategorized

In Figure 1, I show a chart of CVR Partners LP (UAN) with the setup (yellow circle), the buy signal (green circle) and the exit (red circle). The author indicates that a valid buy signal does not occur unless the closing price has penetrated the lower band and then it closes above the upper band.

On 10/3/11, the close of 20.25 is below the lower band of 20.81 and then we have to wait until 1/3/12 for the close of 26.48 to be above the upper band of 25.36. We would enter the next day at the opening price of 26.57.

We would stay in the trade until the closing price is below the lower band. The exit does not occur for several months on 5/9/12 when the close of 24.45 is below the lower band of 27.76. We would then exit the next day at the open of 24.41 for a loss of $2.07 plus commission and slippage.

The highest close of the trade occurred on 2/2/12, just a few weeks after the entry, for a high open profit of $4.35. The trade would have been profitable if we had used the middle band as the exit. Note that I did not code the suggested trading system as the author indicates that more is to come in future parts of the article series.

Figure 1 – chart of UAN with SVE Volatility Bands and setup (yellow), entry (green) and exit (red) signals for the period 10/3/11 to 5/10/12.

Jul 12, 2013 | Uncategorized

by Hank Swiencinski, AIQ TradingExpert Pro client for over 20 years, founder of ‘The Professor’s One Minute Guide to Stock Management’

Join Hank at a special one hour webinar entitled ‘The Professor’s Rifle Trade’, August 22, 2013. hank will reveal his most powerful position trading technique. Limited audience and early bird pricing. LEARN MORE

The Dow fell 8 points, closing at 15,291. Volume on the NYSE was extremely light on the decline, coming in at only 71 percent of its 10 day average. There were 194 new highs and 36 new lows.

The markets spent most of the day waiting to see what the Fed minutes said about their plans for stimulating the economy. When the minutes came out at 2pm, there was a small rally, but it died quickly leaving the Dow flat into the cloise. However after the close, Bernanke, speaking at a conference sponsored by the National Bureau of Economic Research, stated that the U.S. economy continues to need an accommodative monetary policy. This caused US futures to shoot higher in after market trading, with the Dow futures gaining over 140 points..

There was another small change in the A-D oscillator yesterday, so you could say that the oscillator was predicting the Bernanke move. The Big Move should be enough to push the Dow above the point where the odds favor the scenario that wave ‘c’ up has started. But over the past few months, we have seen several times where a ‘talked up’ markets has come back down to earth, so today’s trading should be very interesting to watch.

Bernanke’s statement also caused several of the world markets to rally overnight, including China’s Hang Seng which gained over 2 percent. So it appears that FXP will make that second low in the Blade that I talked about yesterday. Same for EEV as the Bovespa is currently trading up almost one percent. BTW, the 60s remained negative yesterday on both FXP and EEV, so my Rifle Trade on the ETFs was never triggered.

I spent a few hours last night looking at the volume data on several of the indexes, and what I saw was not pretty picture. The P-Volume, Volume Accumulation Percent and On Balance Volume on the Dow (DIA) remain very negative, despite the past week’s advance. And while two of the three same indicators on the Nasdaq (QQQ) are positive, they are showing significant divergences with price. This problem with volume could all change if the overnight spike rally continues to be supported in the next few days. But right now, it’s very hard for me to believe that the rally will stick on such negative and diverging volume.

Also, the pattern is somewhat troubling to me as well if wave ‘c’ up is starting. Up until last night, the pattern on the Dow looked more like an a-b-c move coming off the 24 June low of 14, 551. But after last night’s spike rally, the c wave of that a-b-c move will start to look impulsive, meaning that it’s starting to appear more like a wave 3 up than a wave c. This too would strongly argue that wave 1 up of wave ’c’ is underway.

The Dow high of 15,542 made on 22 May should provide significant resistance to any rally built on Bernanke’s words. So even if we do pop, I would expect the markets to pull back to form a better pattern before they have enough strength to support a further advance. If the volume starts to improve, and the market pulls back, that’s where I’ll look to go long. Not now.

Remember, wave ‘c’ up should be the final wave in the three wave sequence for Major Wave E up that started back in November 2012. And once this wave completes, there will not be any more up major waves in the Ending Diagonal Pattern for a long time. So please, pay attention to the Dean’s List during the next few months. As long as the Dean remains positive, odds are that the markets will continue to push higher as final wave ‘c’ of Major Wave E starts to unfold.

If this starts to happen, I will be trading this final wave up the same way that I traded the ‘a’ wave that occurred from January into late May with Rifle Trades. As we prepare for this, you might want to take a look at a stock like GILD on the Daily’s. I’m not saying that GILD is the stock I will be looking to trade. It’s only an example of what you should be looking for. Note how GILD has been in a steady Uptrend since April 2012. Notice too how the PT indicators remained positive for most of that time. Then after you have done this, remove all of the PT indicators so your chart just contains the price and a 2-period RSI Wilder. What I want you to see is how many opportunities you had to go ‘hunting’ on GILD. And how many of those trades resulted in profits of 5-6 points.

So don’t worry about today’s spike rally. If it’s part of wave 1 up of ‘c’ up there will be plenty of opportunities to go hunting…at a much lower risk. Right now, all I’m doing is polishing my Rifle.

That’s what I’m doing,

h

Jul 2, 2013 | Uncategorized

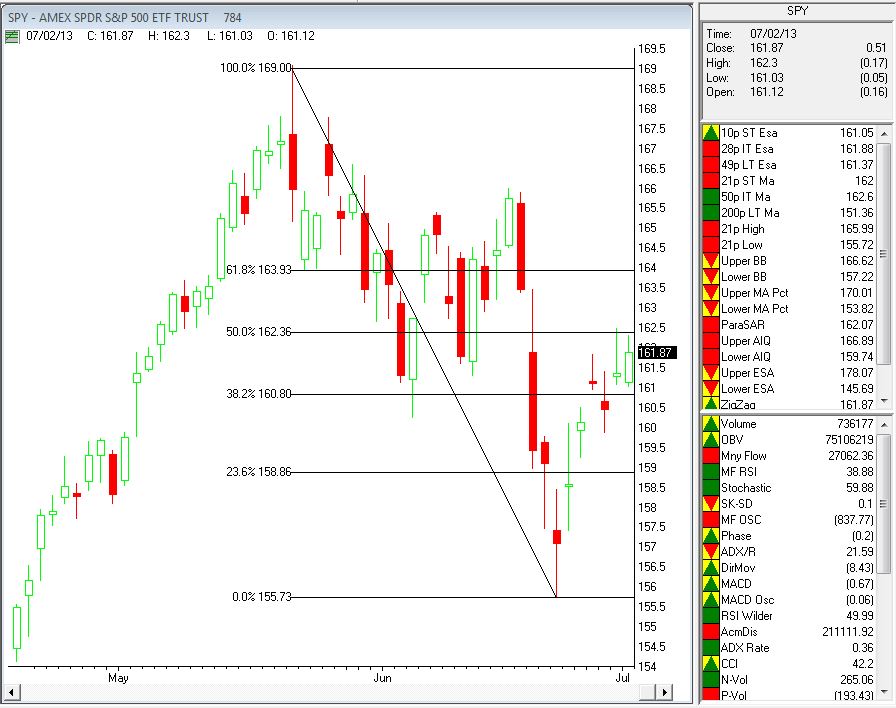

One of my favorite chart tools is Fibonacci Retracements. I find it really useful on retracements both from a high and from a low point.

Here’s what I mean on the SPY July 2, 2013 chart below.

I’ve run the retracement from the high of May 20, 2013 to the recent low on June 24, 2013. The levels generated provide possible resistance levels to the rally from the low. I find the 50% and 61.8% levels most useful. In this example the market is struggling to break through the 50% retracement of this down move at around $162.5. If it does break out, the next level of resistance is at 61.8% or when SPY is around $164. if the rally fails at the 50% retracement then I consider the retracement pattern completed.

Incidentally, I drew this retracement 2 days after the low on June 24, 2013.

This was not the first Fibonacci Retracement I’ve drawn since the high of May 20, 2013. On June 6, 2013 when prices reached a low of $160.25 and rallied up from there. I drew the Fibonacci Retracements from the high of May 20, 2013 to the low of June 6, 2013. In this instance, as you can see in the chart below, the SPY struggled with the 61.8% retracement, before falling away. Again once the prices fall away from the retracement level, I consider that pattern over.