Oct 21, 2013 | Uncategorized

The Stock Trader’s Almanac, put out each year by the Hirsch Organization, is one of my favorite publications. Interesting ideas are one thing. Interesting ideas that actually work are entirely something else. And the Almanac is chock full of just that.

Of course, some of us are not content to leave well enough alone (Hi, my name is Jay). One system that I follow involves using the Almanac’s “Nasdaq’s Best Eight Months Strategy” with MACD Timing. However, instead of buying a stock index I focus on the top performing Fidelity Select Sector Funds.

The method works like this:

-Starting on October first, track the action of the MACD indicator for the Nasdaq Composite Index using MACD parameter values of 8/17/9.

-When the fast line crosses above the slow line – or if the fast line is already above the slow line on 10/1, a buy signal occurs.

Figure 1 displays the most recent buy signal which occurred at the close on 10/15/13.

Figure 1 – MACD Buy Signal (Chart courtesy of AIQ TradingExpert)

-Then find the five top Fidelity Select sector funds.

There are a number of different ways to do this. The method I use is to run AIQ TradingExpert Relative Strength report over the past 240 trading days. This routine looks at the performance of each fund over 240 trading days but gives extra weight to the most recent 120 days. You can use different variables, or you can simply look at raw price change over the previous 6 months to come up with a list of “Top Select Sector Performers.” The list for 10/15/13 appears in Figure 2.

Figure 2 – High Relative Fidelity Select Sector Funds (Courtesy AIQ TradingExpert)

-Buy the top five Select Sector funds the next day.

-Starting on June 1st of the next year, track the action off the MACD indicator for the Nasdaq Composite Index using MACD parameter values of 12/25/9.

When the fast line crosses below the slow line – or if the fast line is already above the slow line on 6/1, then sell the Fidelity Select sector funds on the next trading day.

Repeat.

Results

The test period used here starts in October of 1998. The year-by-year results of this system during the Favorable eight month period versus the performance of the S&P 500 Index during the same time appears in Figure 3.

Figure 3 – Year-By-Year Bullish Eight Months (System vs. SPX)

|

Measure

|

System

|

S&P 500 Index

|

|

Number of times UP

|

14 (93%)

|

11 (73%)

|

|

Number Times Down

|

1(7%)

|

4 (27%)

|

|

Number time better performer

|

11

|

4

|

|

Average % +(-)

|

+14.1%

|

+6.2%

|

|

Worst %+(-)

|

(-0.8%)

|

(-10.9%)

|

Figure 4 – System versus S&P 500 during “Bullish Eight Months”

Summary

As you can see, this relatively simple system has registered a gain in 14 of the past 15 “bullish” eight month periods. On average it has outperformed the S&P 500 by a factor of 2.27-to-1.

So does any of this mean that a portfolio of FSAVX/FBIOX/FBSOX/FSCSX/FSESX is sure to make money and outperform the S&P 500 between now and June of 2014? Sadly, no.

I guess I’ll just have to take my chances.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro client

http://jayonthemarkets.com/

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Oct 17, 2013 | Uncategorized

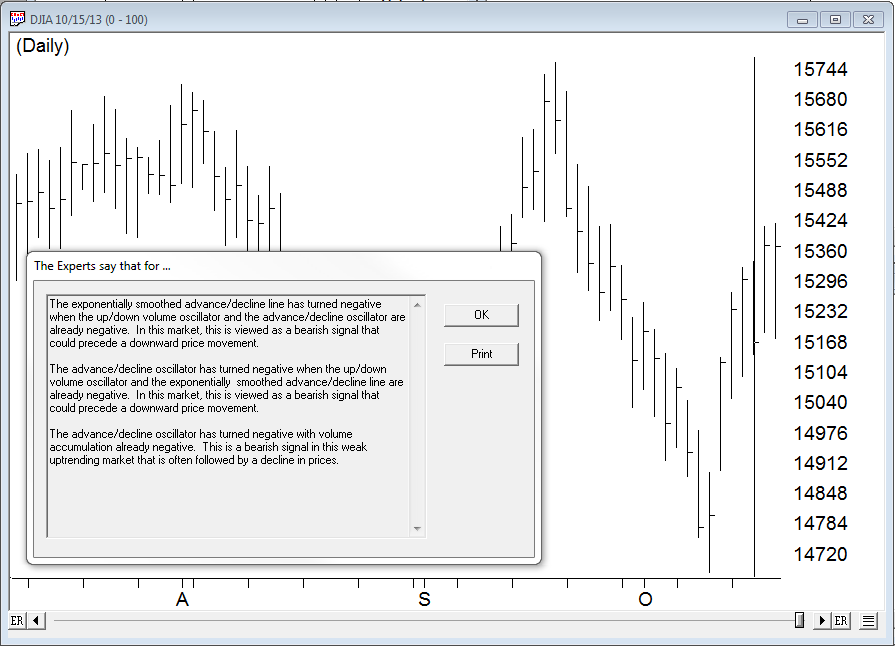

On Tuesday 10-15-2013 our AI market expert system fired a 0-100, that indicates a heavy weighting to the downside on the technical indicators. This is what the AI said

“The exponentially smoothed advance/decline line has turned negative wh…en the up/down volume oscillator and the advance/decline oscillator are already negative. In this market, this is viewed as a bearish signal that could precede a downward price movement.

The advance/decline oscillator has turned negative when the up/down volume oscillator and the exponentially smoothed advance/decline line are already negative. In this market, this is viewed as a bearish signal that could precede a downward price movement.

The advance/decline oscillator has turned negative with volume accumulation already negative. This is a bearish signal in this weak uptrending market that is often followed by a decline in prices. “

http://aiqsystems.com/

Oct 8, 2013 | Uncategorized

Well according to reports that I have read, we are a little over a week away from Financial Armageddon, or at least that is what we are told will unfold if Congress does not raise the debt limit by October 17th. For if the debt limit is not raised by that time then the Fed will be unable to pay its bills (the 17 trillion dollars of debt that we have already raked up only means that up to now we have simply been “unwilling” to pay our bills – which apparently is different than “unable”), which means the U.S. Government may default and that the whole “Full Faith and Credit” thing will suddenly become worth approximately “a bucket of warm spit.” OK, that’s the Bad (granted, Very Bad) News. But there are two pieces of good news.

First, the financial markets are so far taking financial Armageddon pretty darn calmly. Sure the stock market is down a little bit of late, but overall it appears to be doing its best Alfred E. Nuemann (“What, Me Worry?”) impersonation. As a side note, I can’t quite figure out what the “Flight to Quality” crowd will do once the treasury defaults. I can’t help but think that half of them will buy treasury bonds anyway just as a reflex and because they don’t know what else to do (Old dogs, new tricks, if you get my drift).

The other piece of good news is that our elected politicians are “hard at work” attempting to solve this problem (Granted our elected officials appear to have a “slightly” different definition of “Hard at Work” than the rest of us shlubs). Whatever else you can say about them, our politicians are definitely busy engaging in politics these days. Nothing that will do any of us any good, granted, but hey, this whole “We the People” thing is getting just about as outdated as that whole “Full Faith and Credit” thing. So perhaps they are simply planning to wipe out both of these “antiquated” concepts in one fell swoop (at least that’s the only explanation that comes to mind).

When I think of our president and Congress I keep envisioning that image of those guys playing poker in the lounge of the Titanic. Sitting there at a 45 (and ever increasing) degree angle, they remain focused on what they considered to be the most important thing – “Hey, I think I can win this hand!”

Of course as we all know, all of this is completely and entirely the fault of [your least favorite political party here]. And no one can tell anyone otherwise.

What to Do, What to Do

Needless to say, everyone is pretty much assuming that something will happen at the 11th hour that will allow us to avoid “Shock and Awe, and Not in a Good Way” to our economy. Otherwise there might be just a tad more concern being reflected in the financial markets. Still it might be wise to think things through just a bit and to avoid “the conditioned response.”

Some of you may recall the utter “fear and loathing” that preceded the heavily anticipated “Fiscal Cliff” that we were going to plunge off of on January 1st of 2013. How did that work out? With a 20%+ gain in the stock market in the ensuing 8 months, of course. So there is a certain part of us that is now conditioned to believe that “potentially economically catastrophic events” lead to “above average returns”, which I am not entirely sure is the proper lesson. If nothing else, it’s a pretty small sample size.

So should investors simply take solace and assume that “things will work out?” Or is some sort of “defensive action” in order? At this point I think it is wise to invoke that age old bit of wisdom that states, “Hope for the Best, Prepare for the Worst.” At this point there are two basic theoretical scenarios:

1. A deal is reached to avoid a U.S. default and stocks bounce and bonds do not collapse.

2. The U.S. does default and stocks and U.S. treasury securities tank.

If you are a typical investor with a typical allocation of your portfolio to stocks then you don’t really need to “do” anything to take advantage of scenario #1. So that was easy.

Scenario #2 is “a little trickier”. There is a school of thought that states (probably accurately) that if the U.S. does default on its debt there will be far bigger problems than your stock portfolio. And that may be true. But in this worst case scenario it is not like the stock market will close down for good, the economy will (immediately) grind to a halt and we will all begin just “living off the land.” So “just in case”, it might make sense to “hedge.”

One Possibility

As I have written about recently, my new favorite hedging tool (for hedging specifically against an adverse move in the stock market) are call options on ticker VXX, the exchange-traded fund that ostensibly tracks futures contracts on the VIX Index.

The bottom line is simple to understand:

-When the stock market goes down, the VIX Index goes up.

-And the harder the stock market falls, the more quickly the VIX Index “spikes”.

So if you have concerns about a stock market decline then a cheap VXX call option can offer some pretty good upside potential. A trade that I highlighted recently involving VXX call options appears in Figures 1 and 2. (http://jayonthemarkets.com/2013/09/17/looking-to-vxx-just-in-case/)

Figure 1 – VXX Nov 14 Call Option (courtesy www.OptionsAnalysis.com)

Figure 2 – VXX Nov 14 Call Option Risk Curves (courtesy www.OptionsAnalysis.com)

As you can see in Figure 3, VXX has rallied from 13.84 to 16.21, or +17%. In the same time the VXX call option shown in Figures 1 and 2 have advanced +116%. This clearly illustrates the potential benefit of leverage in the options market.

Figure 3 – Ticker VXX (exchange=traded fund) bounces recently (courtesy AIQ TradingExpert)

How high could VXX go if the U.S. somehow manages to default? Figure 4 displays the longer-term history of the VIX Index itself.

Figure 4 – The VIX Index; How High Can it Go? (courtesy AIQ TradingExpert)

Just to “go to extremes”, if we had another meltdown along the line of 2008 and if ticker VXX rallied to 80, the November 14 VXX call option would be worth $66 a contract, or a gain of about +5,000% from the initial price on 9/20 (about +2,265% from current levels).

The Irony

The ironic part is that as exciting as a potential gain of 2,000 to 5,000% sounds, we absolutely, positively hope that it doesn’t happen. In fact, in the overall best case scenario these VXX call options expire worthless as the stock market rallies and volatility subsides.

What we hope is that our esteemed elected officials will get their act together and come up with a solid long-term plan to put the U.S. back on solid financial footing.

Or at the very least, that they avoid making us Thelma to their Louise.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro client

http://jayonthemarkets.com/

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Oct 8, 2013 | Uncategorized

Well according to reports that I have read, we are a little over a week away from Financial Armageddon, or at least that is what we are told will unfold if Congress does not raise the debt limit by October 17th. For if the debt limit is not raised by that time then the Fed will be unable to pay its bills (the 17 trillion dollars of debt that we have already raked up only means that up to now we have simply been “unwilling” to pay our bills – which apparently is different than “unable”), which means the U.S. Government may default and that the whole “Full Faith and Credit” thing will suddenly become worth approximately “a bucket of warm spit.” OK, that’s the Bad (granted, Very Bad) News. But there are two pieces of good news.

First, the financial markets are so far taking financial Armageddon pretty darn calmly. Sure the stock market is down a little bit of late, but overall it appears to be doing its best Alfred E. Nuemann (“What, Me Worry?”) impersonation. As a side note, I can’t quite figure out what the “Flight to Quality” crowd will do once the treasury defaults. I can’t help but think that half of them will buy treasury bonds anyway just as a reflex and because they don’t know what else to do (Old dogs, new tricks, if you get my drift).

The other piece of good news is that our elected politicians are “hard at work” attempting to solve this problem (Granted our elected officials appear to have a “slightly” different definition of “Hard at Work” than the rest of us shlubs). Whatever else you can say about them, our politicians are definitely busy engaging in politics these days. Nothing that will do any of us any good, granted, but hey, this whole “We the People” thing is getting just about as outdated as that whole “Full Faith and Credit” thing. So perhaps they are simply planning to wipe out both of these “antiquated” concepts in one fell swoop (at least that’s the only explanation that comes to mind).

When I think of our president and Congress I keep envisioning that image of those guys playing poker in the lounge of the Titanic. Sitting there at a 45 (and ever increasing) degree angle, they remain focused on what they considered to be the most important thing – “Hey, I think I can win this hand!”

Of course as we all know, all of this is completely and entirely the fault of [your least favorite political party here]. And no one can tell anyone otherwise.

What to Do, What to Do

Needless to say, everyone is pretty much assuming that something will happen at the 11th hour that will allow us to avoid “Shock and Awe, and Not in a Good Way” to our economy. Otherwise there might be just a tad more concern being reflected in the financial markets. Still it might be wise to think things through just a bit and to avoid “the conditioned response.”

Some of you may recall the utter “fear and loathing” that preceded the heavily anticipated “Fiscal Cliff” that we were going to plunge off of on January 1st of 2013. How did that work out? With a 20%+ gain in the stock market in the ensuing 8 months, of course. So there is a certain part of us that is now conditioned to believe that “potentially economically catastrophic events” lead to “above average returns”, which I am not entirely sure is the proper lesson. If nothing else, it’s a pretty small sample size.

So should investors simply take solace and assume that “things will work out?” Or is some sort of “defensive action” in order? At this point I think it is wise to invoke that age old bit of wisdom that states, “Hope for the Best, Prepare for the Worst.” At this point there are two basic theoretical scenarios:

1. A deal is reached to avoid a U.S. default and stocks bounce and bonds do not collapse.

2. The U.S. does default and stocks and U.S. treasury securities tank.

If you are a typical investor with a typical allocation of your portfolio to stocks then you don’t really need to “do” anything to take advantage of scenario #1. So that was easy.

Scenario #2 is “a little trickier”. There is a school of thought that states (probably accurately) that if the U.S. does default on its debt there will be far bigger problems than your stock portfolio. And that may be true. But in this worst case scenario it is not like the stock market will close down for good, the economy will (immediately) grind to a halt and we will all begin just “living off the land.” So “just in case”, it might make sense to “hedge.”

One Possibility

As I have written about recently, my new favorite hedging tool (for hedging specifically against an adverse move in the stock market) are call options on ticker VXX, the exchange-traded fund that ostensibly tracks futures contracts on the VIX Index.

The bottom line is simple to understand:

-When the stock market goes down, the VIX Index goes up.

-And the harder the stock market falls, the more quickly the VIX Index “spikes”.

So if you have concerns about a stock market decline then a cheap VXX call option can offer some pretty good upside potential. A trade that I highlighted recently involving VXX call options appears in Figures 1 and 2. (http://jayonthemarkets.com/2013/09/17/looking-to-vxx-just-in-case/)

Figure 1 – VXX Nov 14 Call Option (courtesy www.OptionsAnalysis.com)

Figure 2 – VXX Nov 14 Call Option Risk Curves (courtesy www.OptionsAnalysis.com)

As you can see in Figure 3, VXX has rallied from 13.84 to 16.21, or +17%. In the same time the VXX call option shown in Figures 1 and 2 have advanced +116%. This clearly illustrates the potential benefit of leverage in the options market.

Figure 3 – Ticker VXX (exchange=traded fund) bounces recently (courtesy AIQ TradingExpert)

How high could VXX go if the U.S. somehow manages to default? Figure 4 displays the longer-term history of the VIX Index itself.

Figure 4 – The VIX Index; How High Can it Go? (courtesy AIQ TradingExpert)

Just to “go to extremes”, if we had another meltdown along the line of 2008 and if ticker VXX rallied to 80, the November 14 VXX call option would be worth $66 a contract, or a gain of about +5,000% from the initial price on 9/20 (about +2,265% from current levels).

The Irony

The ironic part is that as exciting as a potential gain of 2,000 to 5,000% sounds, we absolutely, positively hope that it doesn’t happen. In fact, in the overall best case scenario these VXX call options expire worthless as the stock market rallies and volatility subsides.

What we hope is that our esteemed elected officials will get their act together and come up with a solid long-term plan to put the U.S. back on solid financial footing.

Or at the very least, that they avoid making us Thelma to their Louise.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro client

http://jayonthemarkets.com/

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Oct 2, 2013 | Uncategorized

The AIQ code for Sylvain Vervoort’s color study and system described in his article in the October issue of Stocks and Commodities, “An Expert Of A System,” is provided at www.TradersEdgeSystems.com/traderstips.htm.

Figure 1 is a chart of Netflix (NFLX) with a color bar study that shows when the expert system is in a buy mode (green bars). A buy mode occurs when the typical price exponential moving average (typEMA) is above the heinkin-ashi close exponential moving average (haEMA), and the close is above the open after having been in the sell mode. For the sell to be true (red bars), the typEMA must be below the haEMA and the close must be below the open for the initial signal to go short after having been in the buy mode.

FIGURE 1: AIQ, TYPEMA AND HAEMA. Here is a sample chart of NFLX with typEMA (yellow) and haEMA (green), with the color study showing buys (green bars with up white arrows) and sells (red bars with down white arrows).

Figure 1 also shows the two moving averages typEMA in yellow and the haEMA in green. White arrows show the signal dates for the sample trade on NFLX. The entries & exits are the next day at the open. I simplified the system and did not code the stop-loss or the breakeven exits. I ran a test on the NASDAQ 100 from August 11, 2000 to August 9, 2013.

The long-side test results are summarized in Figure 2. The average return for all 13,295 trades is 0.64% per trade before commissions & slippage. This return assumes that all trades are taken. I tested the short side over this same period, and there were 13,256 trades averaging a loss of 1.00% per trade (summary not shown).

FIGURE 8: AIQ, BACKTEST RESULTS. Here is a summary of the backtest results of the long side on the NASDAQ 100 list of stocks from August 11, 2000 to August 9, 2013.

The code and EDS file can be downloaded from www.TradersEdgeSystems.com/traderstips.htm, and is shown below.

! AN EXPERT OF A SYSTEM

! Author: Sylvain Vervoort, TASC, October 2013

! Coded by: Richard Denning

! www.TradersEdgeSystems.com

! INPUTS:

H is [high].

L is [low].

C is [close].

O is [open].

OSD is offsettodate(month(),day(),year()).

typLen is 5.

haLen is 8.

!----------------HEIKIN-ASHI-----------------

haC is (O + H +L + C) / 4.

DaysInto is ReportDate() - RuleDate().

end if DaysInto > 30.

endHAO is iff(end,O, haO).

haO is (valresult(endHAO,1)

+valresult(haC,1))/2.

haH is Max(H,max(haO,haC)).

haL is Min(L,min(haO,haC)).

haCL is (haC + haO + haH + haL) / 4.

haEMA is expavg(haCL,haLen). !PLOT

!---------------end HEIKIN-ASHI---------------

!---------------TYPICAL PRICE ----------------

TYP is (H+L+C)/3.

typEMA is expavg(TYP,typLen). !PLOT

!-----------------end TYPICAL-----------------

!--------------COLOR STUDY--------------------

G if (typEMA > haEMA and C > O).

Gos is scanany(G,200) then OSD.

R if typEMA < haEMA and C < O.

Ros is scanany(R,200) then OSD.

GREEN if G or ^Gos < ^Ros.

RED if R or ^Ros < ^Gos.

!-------------end COLOR STUDY-----------------

!-------------TRADING SYSTEM------------------

Buy if G.

ExitBuy if R.

Sell if R.

ExitSell if G.

!-------------end TRADING SYSTEM--------------

Oct 2, 2013 | Uncategorized

The AIQ code for Sylvain Vervoort’s color study and system described in his article in the October issue of Stocks and Commodities, “An Expert Of A System,” is provided at www.TradersEdgeSystems.com/traderstips.htm.

Figure 1 is a chart of Netflix (NFLX) with a color bar study that shows when the expert system is in a buy mode (green bars). A buy mode occurs when the typical price exponential moving average (typEMA) is above the heinkin-ashi close exponential moving average (haEMA), and the close is above the open after having been in the sell mode. For the sell to be true (red bars), the typEMA must be below the haEMA and the close must be below the open for the initial signal to go short after having been in the buy mode.

FIGURE 1: AIQ, TYPEMA AND HAEMA. Here is a sample chart of NFLX with typEMA (yellow) and haEMA (green), with the color study showing buys (green bars with up white arrows) and sells (red bars with down white arrows).

Figure 1 also shows the two moving averages typEMA in yellow and the haEMA in green. White arrows show the signal dates for the sample trade on NFLX. The entries & exits are the next day at the open. I simplified the system and did not code the stop-loss or the breakeven exits. I ran a test on the NASDAQ 100 from August 11, 2000 to August 9, 2013.

The long-side test results are summarized in Figure 2. The average return for all 13,295 trades is 0.64% per trade before commissions & slippage. This return assumes that all trades are taken. I tested the short side over this same period, and there were 13,256 trades averaging a loss of 1.00% per trade (summary not shown).

FIGURE 8: AIQ, BACKTEST RESULTS. Here is a summary of the backtest results of the long side on the NASDAQ 100 list of stocks from August 11, 2000 to August 9, 2013.

The code and EDS file can be downloaded from www.TradersEdgeSystems.com/traderstips.htm, and is shown below.

! AN EXPERT OF A SYSTEM

! Author: Sylvain Vervoort, TASC, October 2013

! Coded by: Richard Denning

! www.TradersEdgeSystems.com

! INPUTS:

H is [high].

L is [low].

C is [close].

O is [open].

OSD is offsettodate(month(),day(),year()).

typLen is 5.

haLen is 8.

!----------------HEIKIN-ASHI-----------------

haC is (O + H +L + C) / 4.

DaysInto is ReportDate() - RuleDate().

end if DaysInto > 30.

endHAO is iff(end,O, haO).

haO is (valresult(endHAO,1)

+valresult(haC,1))/2.

haH is Max(H,max(haO,haC)).

haL is Min(L,min(haO,haC)).

haCL is (haC + haO + haH + haL) / 4.

haEMA is expavg(haCL,haLen). !PLOT

!---------------end HEIKIN-ASHI---------------

!---------------TYPICAL PRICE ----------------

TYP is (H+L+C)/3.

typEMA is expavg(TYP,typLen). !PLOT

!-----------------end TYPICAL-----------------

!--------------COLOR STUDY--------------------

G if (typEMA > haEMA and C > O).

Gos is scanany(G,200) then OSD.

R if typEMA < haEMA and C < O.

Ros is scanany(R,200) then OSD.

GREEN if G or ^Gos < ^Ros.

RED if R or ^Ros < ^Gos.

!-------------end COLOR STUDY-----------------

!-------------TRADING SYSTEM------------------

Buy if G.

ExitBuy if R.

Sell if R.

ExitSell if G.

!-------------end TRADING SYSTEM--------------