May 2, 2016 | indicators, options, Seasonality

Not every indicator that you look at needs to generate exact buy and sell signals. There are many useful indicators that offer “perspective” more than “precision market timing.” It can be very helpful to track some of these.

The downside of course is that the more indicators you follow the more you can be susceptible to “analysis paralysis” – plus at some point you do have to have “something” that tells you “make this trade NOW!”

But the basis for considering tracking certain “perspective indicators” is that they can help to keep you from falling for those age-old pitfalls, “fear” and “greed”. As the market falls – and especially the harder it falls – the more likely an investor is to start to feel fear. And more importantly, to start to feel the urge to “do something” – something like “sell everything” to alleviate the fear.

On the flipside, when things are going great there is a tendency to ignore warning signs and to “hope for the best”, since the money is being made so easily.

In both cases a perspective indicator can serve as – at the very least – a slap upside the back of the head that says “Hey, pay attention!”

So today let’s review one of my favorites.

The JK HiLo Index

OK, I will admit it is one of my favorites because I developed it myself. Although in reality the truth is that it simply combines one indicator developed long ago by Norman Fosback and another that I read about in a book my either Martin Pring or Gerald Appel.

The calculations are as follows:

A = the lower of Nasdaq daily new highs and Nasdaq daily new lows

B = (A / total Nasdaq issues traded)*100

C = 10-day average of B

D = Nasdaq daily new highs / (Nasdaq daily new highs + Nasdaq daily new lows)

E = 10-day average of D

JK Hi/Lo Index = (C * E) * 100

In a nutshell:

*High readings (90 or above) suggest a lot of “churning” in the market and typically serve as an early warning sign that a market advance may be about to slow down or reverse. That being said, a close look at Figure 1 reveals several instances where high readings were NOT followed by lower prices. However, as a perspective indicator note the persistently high reading starting in late 2014. This type of persistent action combined with the “churning” in the stock market could easily have served as a warning sign for an alert investor.

*Low readings (20 or below) indicate a potential “washout” as it indicates a dearth of stocks making new highs. Readings under 10 are fairly rare and almost invariably accompany meaningful stock market lows.

Figure 1 displays the Nasdaq Composite (divided by 20) with the JK Hi/Lo Index plotted since 2011.

Regarding the difference between a “timing” indicator and a “perspective” indicator, note the two red lines in Figure 2. The JK HiLo Index first dropped below 20 on the date marked by the first red line. It finally moved back above 20 on the date marked by the second red line.

Figure 2 – JK HiLo Index (red line) versus Nasdaq Composite (/20) since 2015 (Courtesy TradingExpert)

Can we say that the JK HiLo Index “picked the bottom with uncanny accuracy”? Not really. The Nasdaq plunged another 10% between the first date the indicator was below 20 until the actual bottom.

Still, can we also say that it was useful in terms of highlighting an area where price was likely to bottom? And did it presage a pretty darn good advance? I think a case can be made that the answers to those questions are “Yes” and “Yes”.

Summary

The bottom line is that while there was a great deal of fear building in the market during January and February, an indicator such as this one can help alert an investor the fact an opportunity may be at hand.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and TradingExpert Pro client

http://jayonthemarkets.com/

Jul 31, 2014 | chart patterns, Seasonality, swing trading, trading strategies, Uncategorized

It’s the beginning of the month and time to check the seasonal patterns for August 2014. First off some background.

Our study looks at 7 years of historical data and looks at the returns for all optionable stocks for the month of August from 2006 to 2013.

We filter to find two sets of criteria

– Stocks with gains in all 7 years during August

– Stocks with losses in all 7 years in August

We do make an assumption that the month is 21 trading days and work our way back from the last day of the month. If the last day of the month falls on a weekend, then we use the first trading day prior to that date.

We make no assumptions for drawdown, nor do we look at the fundamentals behind such a pattern. We do compare the stock to the market during the same period and look at the average SPY gain/loss vs. the average stock gain/loss. This helps filter out market influence. We are now including group information to identify particular segments that might display a seasonal bias.

Finally we look at the median gain/loss and look for statistical anomalies, like meteoric gains/loss in one year.

So here are the tickers that met the scan on the loss side, There was only 1 stock on the gainers side. So we’ll look at the down plays only.

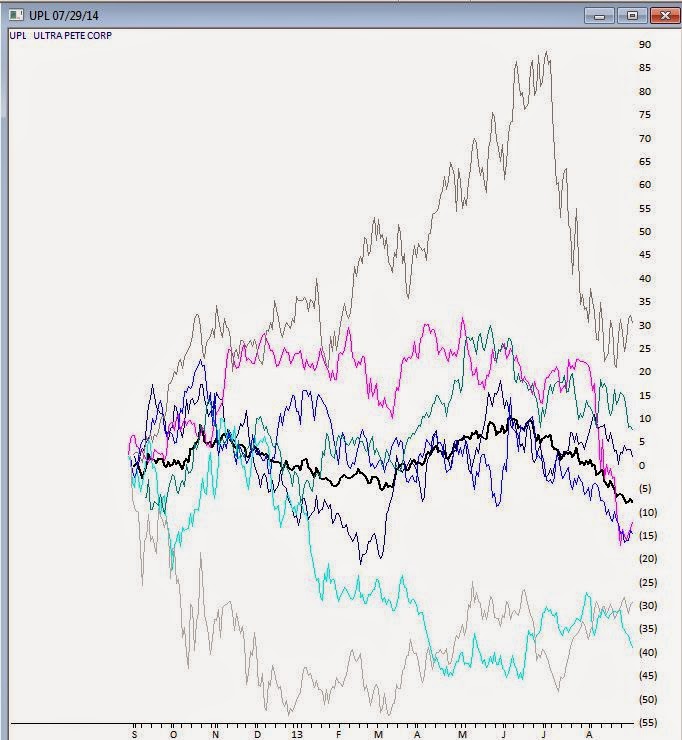

Figure 1 shows the stocks that have had losses in August, 7 years in row.

It’s almost immediately apparent that 4 of the 6 losers are in the Oil & Gas sector, one in the Drilling group, and 3 in Exploration and Production (2 US) groups. Not looking like a good month to be long this sector. The biggest loser is UPL, UltraPete Corp with an average -9.66% in August. A couple of years have seen significant losses in August, but the median is still -7.42%. Not being one to speculate on why the Oil & Gas sector has so many stocks taking a hit in August, but there it is. Here’s the seasonal chart of UPL through 8/31/2013, the prominent black line is the average of the 7 years in the study.

Figure 2 seasonal for UPL for last 7 years, average line in black

During the same period the market, as measured by SPY declined an average of -0.06, so there was no overriding market influence during this period.

Figure 3 shows SPY for the same period.

Interestingly a quick check of the Oil & Gas US Explorations and Production group for the same period revealed an average decline of -3.67% in August. The entire group was down 6 of the last 7 years in August. I have 38 stocks in this group in my database.

Figure 4 seasonal average for Oil & Gas US Explorations and Production group

We’ll keep track of the top 2 stocks in the August analysis. UPL and DNR and let you know how they preform.

In July, GLNG was the seasonal star with an average of +8.41% for the 7 years through July 30, 2013. Tracking how it performed this July, GLNG opened at 60.73 on July 1, 2014 and reached a high of 65 on July 30, 2014. Some pullback occurring on July 31, 2014 with the entire market down, but still a gain for the month.

Figure 5 shows the stocks that have had gains in July, 7 years in row.

With seasonality you have to figure out what timeframe you want to analyze before anything else. Logic would seem to dictate that one week; comparing this week to the same period over X years would be the smallest time period you might consider. However there are events that seem to be seasonally predictable that occur at the end of a month or the beginning of the month. We’ll look at some these in a future article.

We don’t draw conclusions here, just mine for information.

Jul 8, 2014 | chart patterns, group sector rotation, Seasonality, trading strategies

While looking through the seasonal trends in stocks and currencies, we decided to start running the seasonality scans on the S & P 500 groups. As a reminder here are the criteria we consider when running this.

Our study looks at 7 years of historical data and looks at the returns for all groups in the S & P 500 for the month of July from 2006 to 2013.

We do make an assumption that the month is 21 trading days and work our way back from the last day of the month. July also has the July 4th holiday and a half day trading on July 3rd. if the last day of the month falls on a weekend, then we use the first trading day prior to that date.

We make no assumptions for drawdown, nor do we look at the fundamentals behind such a pattern. We do compare the group to the market during the same period and look at the average SPY gain/loss vs. the average group gain/loss. This helps filter out market influence.

Finally we look at the median gain/loss and look for statistical anomalies, like meteoric gains/loss in one year. Here are top 5 performing groups based on average return.

Average return alone is misleading. In the seasonal analysis we need consistent patterns in the price action throughout the periods we are testing, in this case 7 years. While The S & P 500 Motorcycle manufacturers group (MTRCYCLE) looks good on average, it includes one stellar July of 37.50% back in 2010, and has 2 July’s that were negative returns. NOTE: there’s only one stock in the group (guess which one that is!).

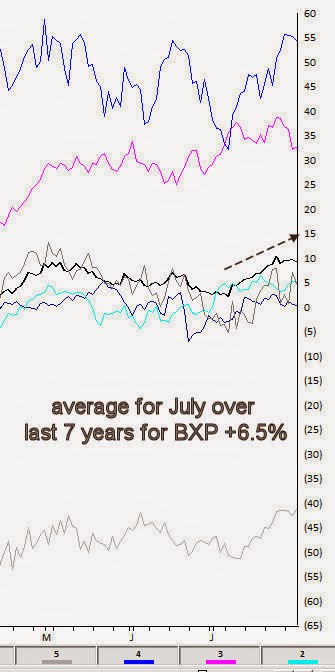

The office REITs group (REITOFC) is more consistent. It has an average return for the last 7 years in July of 6.50%, with the last 6 years Julys all positive. There are no stellar months skewing the average. The group also contains only one stock, Boston Properties [BXP].

Here’s the seasonal chart for BXP

Interestingly the other consistent group in July is another REIT, the Diversified REITs (REITDIV). It has an average return for the last 7 years in July of 6.06%, with the last 6 years Julys all positive. There are no stellar months skewing the average. The group also contains only one stock, Vonando Realty Trust [VNO].

A quick check on what the market did during the same period reveals an average return of 1.83% with 4 gaining Julys and 3 losing Julys.

The Oil & gas Equipment group (OILGASEQ) also had a decent average, but is more volatile over the past years, however the last 5 years have all been gainers.

Remember, we don’t draw conclusions here, just mine for information.

May 3, 2014 | chart patterns, Risk management, Seasonality, trading strategies

I have to admit I am a little surprised. It is the last day of April and so far I have only seen a couple hundred thousand “Sell in May and Go Away” related articles, as opposed to the usual several hundred bazillion such articles that usually make their appearance about his time each year. Still, what with May due to pop up at midnight tonight it seems like as good a time as any to chime in.

What You Probably Already Know

Historically the stock market has performed much better between the end of October and the third trading day of May that it has between the third trading day of May and the end of October. To wit, sees Figure 1 and 2.

.

Figure 1 – $1,000 in the Dow from October 31st through 3rd trading day of May (1960-present)

Figure 2 – $1,000 in the Dow from 3rd trading day of May to October 31st (1960-present)

Starting on 10/31/60:

* $1,000 invested in the Dow Industrials each year at the close of trading on the last trading day of October and held through the close of the third trading day of May grew to $47,280.

* $1,000 invested in the Dow Industrials each year at the close of trading on the third trading day of May and held through the close of the last trading day of October decreased to $599.

So to put it in blunt terms:

October to May = +4,628%

May to October = (-40%)

So clearly there is something to the “Sell in May” thing. There is a caveat, however. As you can see from a perusal of Figure 2 it is not as though the stock market declines each and every year during the May to October period. So during many years selling in May and getting back in at the end of October would cause your returns to trail that of the overall market (and we can’t have that now can we?).

So that explains why roughly half of the bazillion annual “Sell in May” related articles warn against blindly selling in May.

What You Probably Don’t Know

Like they always say, sometimes it’s not what you know but who you know that counts. Or in this case, not even someone I have personally met but do associate with. Rob Hanna is the head of Hannah Capital Management (www.QuantifiableEdges.com) and is a colleague of mine in AAPTA (American Association of Professional Technical Analysts). Rob revealed in some of his work the following “guide” for determining whether to “sell in May” or not:

-If the S&P 500 experiences a drawdown of 5% or more between December 31st and April 30th, then sell in May.

-If the S&P 500 DOES NOT experience a drawdown of 5% or more between December 31st and April 30th, then DO NOT sell in May.

Doesn’t get much simpler than that. Since 1960 there have been 14 years during which the S&P 500 did not experience a 5% drawdown and an investor would have simply remained in the market. The results appear in Figures 3 and 4.

Figure 3 – $1,000 in the Dow during bullish periods applying Hanna Sell in May Filter (1960-present)

Figure 4 – $1,000 in the Dow during bearish periods applying Hanna Sell in May Filter (1960-present)

In cold hard numbers:

* $1,000 invested in the Dow Industrials each year durung the “bullish” periods described grew to $70,244.

* $1,000 invested in the Dow Industrials each year duirng the “beairsh” periods describeed decreased to $403.

So to put it in blunt terms, applying Rob Hanna’s Sell in May Filter:

*October to May (plus May to October when no Sell in May IS NOT triggered) = +6,924%

*May to October (only during years when Sell in May IS triggered) = (-59.7%)

Here’s The Bad News

As you can see in Figure 5, the S&P 500 experienced a drawdown of -5.76% between the end of December and the end of April. And -5.76% is greater than -5% (OK, mathematically speaking -5.76 is technically LESS than 5%, but you get my drift – there was a drawdown in excess of 5%).

Figure 5 – S&P 500 for 2014

So by that rule, the Sell in May model that I prefer says to sell at the close on the third trading day of May and to buy back in at the end of October (although for the record, buying at the end of September is typically better in a mid-term election year, but that’s a topic for another article).

Summary

So because the S&P 500 experienced a -5.76% drawdown is the stock market absolutely, positively doomed to decline between May and the end of October? Of course not. But the historical odds seem to suggest that caution may be in order.

Jay Kaeppel Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://www.aiq.com) client

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Feb 8, 2014 | Seasonality

Hi, my name is Jay and I am a Seasonalaholic.

Now typically when someone confesses to being an “aholic” of some sort or another it because they recognize they have a problem and wish to correct it. That’s not the case here. In fact the “support” group that I belong to is not “Seasonalaholics Anonymous” but rather “Seasonalaholics Unanimous!” (OK, in the interest of full disclosure, so far I am the only member and yes, the monthly meetings aren’t terribly lively, but I digress).

Still I can’t help but think there are others out there who might join someday – especially after they consider things like the seasonal tendencies for retailing stocks. To whit: what would have happened had an investor invested in Fidelity Select Sector Retailing fund (ticker FSRPX):

-During the months of February, March, October and November

-And then earned 1% of annualized interest while out of the market the other 8 months.

The answer is contained in Figure 1 which displays the growth of $1,000 invested as described above.

Figure 1 – Growth of $1,000 invested in FSRPX during February, March, October, November (blue line) versus buying and holding the S&P 500 red line) since January 1988.

Figure 1 – Growth of $1,000 invested in FSRPX during February, March, October, November (blue line) versus buying and holding the S&P 500 red line) since January 1988.Now it is pretty impossible to not notice the, ahem, “slight drawdown” experienced during the October, November 2008 period. Still, despite the fact that I have tried very hard scrub that particular time period from my memory bank, I still have some vague recollection that virtually no sector of the stock market was left unscathed during that period. And the rebound has been pretty nice.

So is this really a viable strategy? Well, under the category of “Everything is Relative”, Figure 2 displays the year-by-year performance of this “system” versus buying and holding the SP 500.

|

System |

SP 500 |

|

System |

SP 500 |

|

Annual % |

Annual % |

Difference |

$1,000

|

$1,000

|

|

1988

|

18.6

|

12.4

|

6.2

|

1,186

|

1,124

|

|

1989

|

(1.0)

|

27.3

|

(28.2)

|

1,174

|

1,430

|

|

1990

|

21.3

|

(6.6)

|

27.8

|

1,424

|

1,336

|

|

1991

|

16.2

|

26.3

|

(10.1)

|

1,654

|

1,688

|

|

1992

|

20.4

|

4.5

|

15.9

|

1,992

|

1,763

|

|

1993

|

6.2

|

7.1

|

(0.9)

|

2,115

|

1,888

|

|

1994

|

(1.5)

|

(1.5)

|

0.0

|

2,083

|

1,859

|

|

1995

|

2.3

|

34.1

|

(31.8)

|

2,131

|

2,493

|

|

1996

|

17.4

|

20.3

|

(2.9)

|

2,500

|

2,998

|

|

1997

|

11.9

|

31.0

|

(19.1)

|

2,798

|

3,927

|

|

1998

|

40.1

|

26.7

|

13.4

|

3,919

|

4,975

|

|

1999

|

10.8

|

19.5

|

(8.7)

|

4,344

|

5,946

|

|

2000

|

8.5

|

(10.1)

|

18.7

|

4,714

|

5,343

|

|

2001

|

3.1

|

(13.0)

|

16.1

|

4,859

|

4,646

|

|

2002

|

12.8

|

(23.4)

|

36.2

|

5,480

|

3,561

|

|

2003

|

9.1

|

26.4

|

(17.3)

|

5,977

|

4,500

|

|

2004

|

12.8

|

9.0

|

3.8

|

6,744

|

4,905

|

|

2005

|

8.5

|

3.0

|

5.5

|

7,316

|

5,052

|

|

2006

|

9.2

|

13.6

|

(4.4)

|

7,991

|

5,740

|

|

2007

|

(2.4)

|

3.5

|

(6.0)

|

7,797

|

5,943

|

|

2008

|

(32.0)

|

(38.5)

|

6.5

|

5,303

|

3,656

|

|

2009

|

23.7

|

23.5

|

0.2

|

6,559

|

4,513

|

|

2010

|

26.0

|

12.8

|

13.2

|

8,263

|

5,090

|

|

2011

|

13.2

|

(0.0)

|

13.2

|

9,355

|

5,090

|

|

2012

|

17.3

|

13.4

|

3.9

|

10,976

|

5,772

|

|

2013

|

10.7

|

29.6

|

(18.9)

|

12,155

|

7,481

|

| |

|

|

|

|

|

| Average |

10.9

|

9.6

|

1.3

|

+1,115% |

648% |

| StdDev |

12.8

|

17.9

|

|

|

|

| Ave/SD |

0.849

|

0.540

|

|

|

|

Figure 2 – “System” versus S&P 500 Buy and Hold

Summary

The difference in the average annual return is not large (+10.9% for the system versus +9.6% for the S&P 500). But this difference adds up over time. Since January 1988 the system has gained +1,115% versus + 648% for the S&P 500 (while only being in the market 33% of the time. The true “numbers geeks” will notice that the standard deviation of annual returns for the system is only 2/3rds as large as that for the S&P 500 – i.e., much less volatility).

So I ask again, is this really a viable strategy? Perhaps. But the truth is that it can get a whole lot better – as I will detail the next time I write.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://www.aiq.com) client

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.

Jan 7, 2014 | retail stocks, Seasonality

I usually run a seasonal analysis at the beginning of the trading month to look for consistent seasonal behavior in stocks. I also run this same analysis for the Santa Claus rally and other notable seasonal times.

To be brief. I look at the remainder of the January’s trading for my database of stocks. I look back 8 years to see if there are any stocks that consistent trade the same way during the analysis period for each of the 8 years. I compare to the SPY for the same period, so I can be sure there’s little or no market bias (SPY average for this test period was -1.07%)

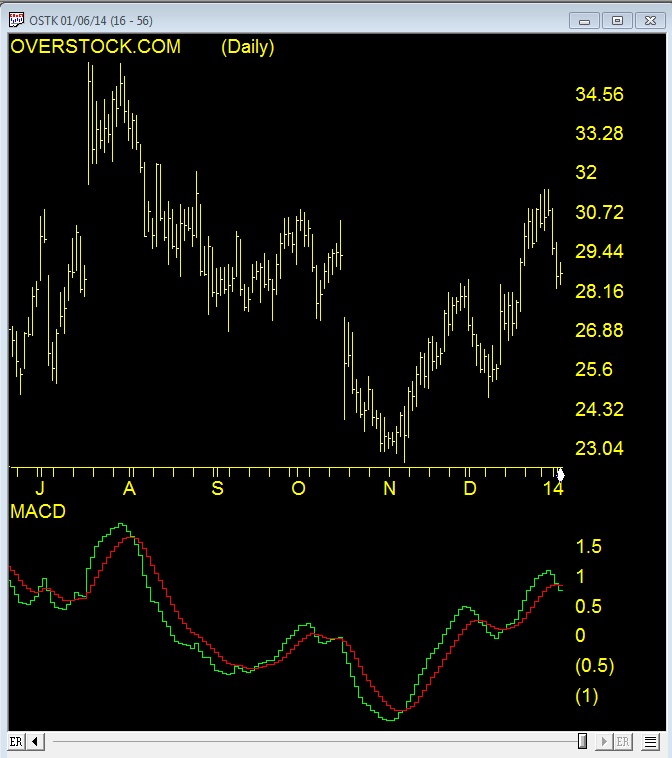

For the remainder of January, only one stock made it to the list on the negative side. This stock was down for the remainder of January for each of the last 8 years. The stock is Overstock.com [OSTK].

Here are the results

OSTK return for the remainder of January

Jan-13 -10.28

Jan-12 -13.65

Jan-11 -7.05

Jan-10 -10.99

Jan-09 -0.18

Jan-08 -30.93

Jan-07 -1.22

Jan-06 -14.13

avg -11.16

I’m always cautious when there are extreme figures in one or two years, as these distort the average. The median for OSTK though is roughly -10% so that still makes it attractive to me. Of course there are no guarantees but so far January 2014 has started as a loser for OSTK