This time of year you might expect us to be thinking about the Santa Claus rally, but after the beating we’ve had the last few days, lets check and see how effective this really is.

What Is a Santa Claus Rally?

I lifted this description from Investopedia

A Santa Claus rally describes a sustained increase in the stock market that occurs in the last week of December through the first two trading days in January. There are numerous explanations for the causes of a Santa Claus rally including tax considerations, a general feeling of optimism and happiness on Wall Street, and the investing of holiday bonuses. Another theory is that some very large institutional investors, a number of which are more sophisticated and pessimistic, tend to go on vacation at this time, leaving the market to retail investors, who tend to be more bullish.

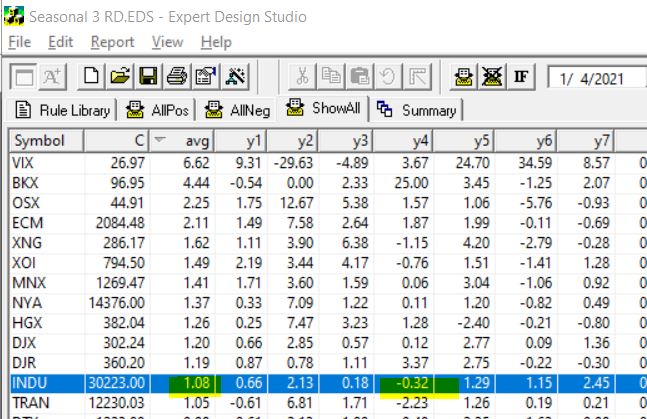

To test this in Expert Design Studio, I used the Seasonality3 ED built-in strategy. I set the Season Length days to 7 days to encompass the last 5 trading days of December and the first 2 days in the New Year.

By setting the date to 1/4/21, the rule looks back 7 trading days from January 4th, each of the last 7 years and gives us an approximate percentage return for each of those 7 days.

Some years with weekends and extra holiday days plus 252 is used as default trading days skew results a small amount. To compensate I also tested 10 trading days back from January 7. The results from the 7 days are below, I tested all the indices in my current database.

INDU is highlighted, this is the Dow 30 index. First it’s clear that in every year except for one, over the last 7 years the Dow has made gains in the Santa Claus period. The average gain Is over 1%. Not too bad for a 7 day trading period. BTW the results from the 10 days from January 7 were similar.

The NASDAQ on the contrary had 3 losing years out of the 7.

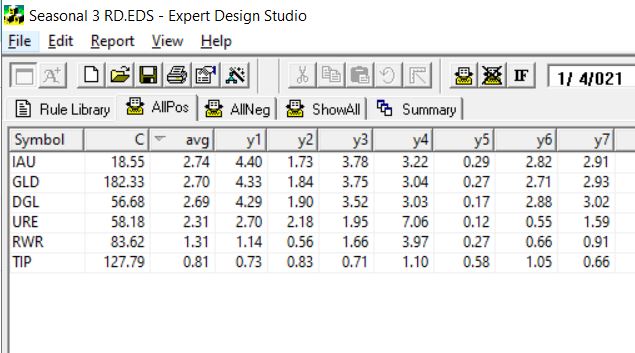

So next I decided to look at what ETFs are most likely to have a Santa Claus rally. Here’s the results using the 7 trading days back from Jan 4. This is the ETFs that had gains every year for the last 7.

The first 3 ETFS are all Gold related, the next two are real estate/REITs the last one is a bond fund. Hmm something to keep in mind.

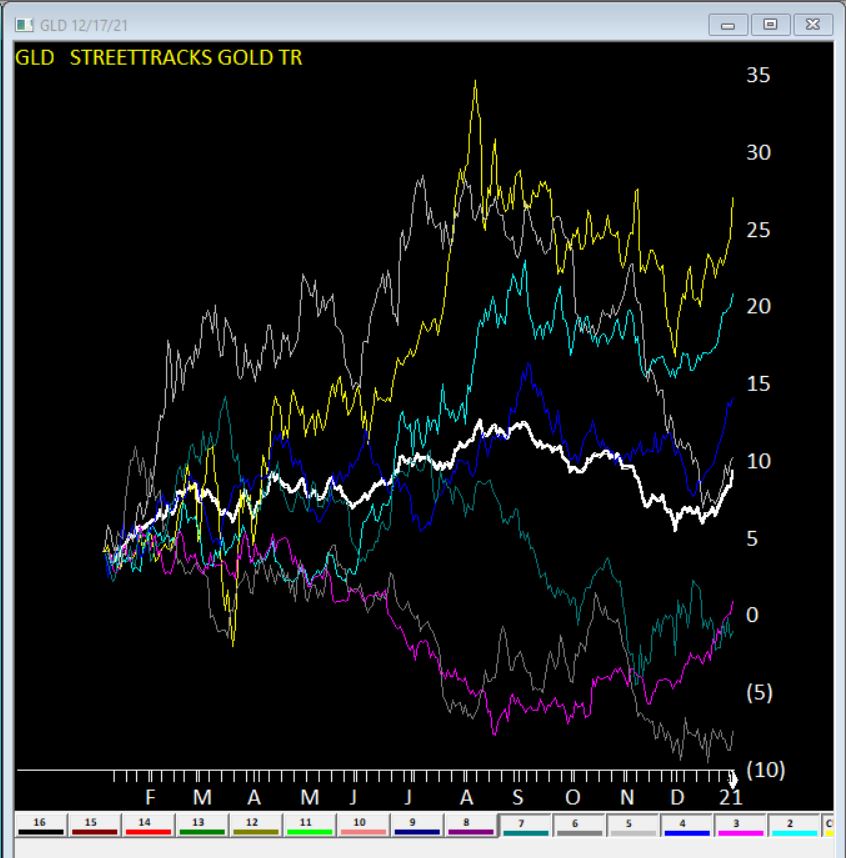

Here’s GLD seasonal charts the right hand side of each year shows the Santa Claus rally clearly. The White line is the average of all 7 years.

Clearly no guarantees what will happen this year, but something to keep in mind.

OK, for the record, I have stood in enough long lines next to impossibly sweaty people (Full Disclosure: They likely feel the same way about me) to know that all of the talk of “Disney” and “Magic” is strictly for marketing consumption. That being said – and despite the fact that you cannot attend the flagship property in sunny CA, and likely will not be able to for some time – there is something about “going to Disney” that still strikes a chord with a whole lot of people.

Of course, my interest here is more financial in nature.

Now the “rational” thing to do in the minds of most investors is to ask and answer some serious questions regarding “theme park attendance.” in the age of COVID-19. Questions like “will attendance pick up anytime soon” and “will DIS continue to be an economic powerhouse if attendance does not return to pre-Covid levels?”

Here is a link to a factual, well-researched and well-written article noting that Disney World attendance as of 8/21/20, attendance was down 80% from a year earlier. Scary stuff, right? And the snap implication is fairly obvious – theme parks are suffering and may continue to do so for the foreseeable future.

But as I mentioned, my interest is more financial in nature. And I tend to look at things from a slightly different angle than a lot of other people. Part of that is because I have come to recognize that (like a lot of other people, but sadly unbeknownst to a lot of those same people) I (and they) am not very good at accurately answering “questions about the future”, such as those posed above about theme parks.

I read that theme park attendance is “down 80%” and instantly that voice in my head loudly issues that age-old “DANGER! WARNING WILL ROBINSON” alert and I feel the urge to scurry off in the other direction. But fortunately, I have gotten pretty good at not overreacting to that initial warning and coming back for a second glance.

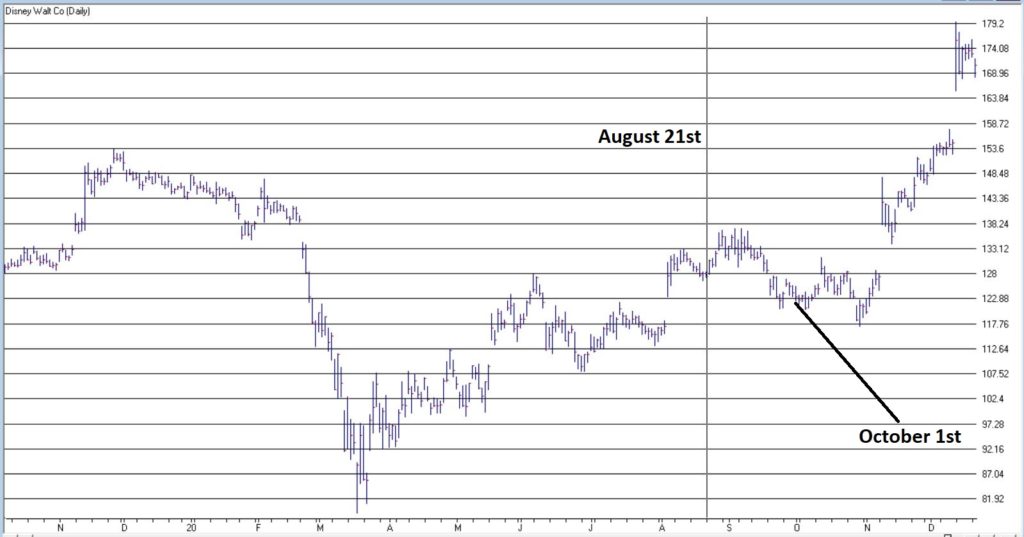

Consider Figure 1. The date marked by the vertical line is August 21, 2020, i.e., the day that the news came out that “Disney World attendance is down 80%, that heavy discounting going on, that Disney stock is down for the year and that it is lagging the major stock indexes.”

Since that “DANGER! WARNING WILL ROBNINSON” moment, DIS is up +34% in 4 months, versus +9% for the S&P 500 Index (FYI, DIS is now up 18% for 2020 vs. 14%+ for the S&P 500).

Are the financial markets a perverse beast, or WHAT!?

The “Real Magic” of Disney Stock

So, what the heck happened to make DIS stock burst higher even in the face of seemingly very bad fundamental news? Well, long story short, October 1st happened. Wait, what? October 1st? Surely it can’t be that simple!?

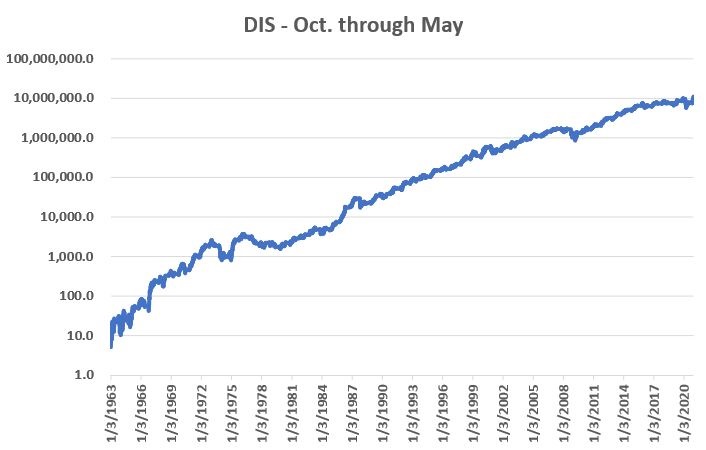

Here’s the thing: it probably should not be that simple. And there is absolutely no guarantee that it will continue to be that simple. But for the past roughly 6 decades…. it has been just about that simple. Consider Figure 2.

Figure 2 displays the cumulative % gain for DIS stock held ONLY from October 1st each year through the end of May the following year, every year since 1962.

Figure 2 – DIS % +(-) during October through May (logarithmic scale)

An initial $1,000 investment in DIS stock held only October through May starting in 1962 is worth $108,512,237 as of 12/18/2020, or a gain of +10,851,124%.

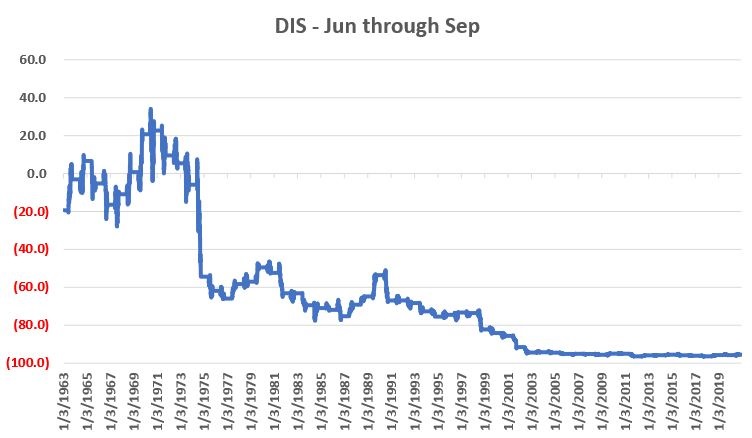

Figure 3 displays the cumulative % gain for DIS stock held ONLY from June 1st each year through the end of September that same year, every year since 1962.

Figure 3 – DIS % +(-) during June through September (non-logarithmic scale)

An initial $1,000 investment in DIS stock held only June through September starting in 1962 is worth $44.86 as of 12/18/2020, or a loss of -95.5%.

The Upshot

Many investors will ask the obvious question of “Why does this work?” And the most succinct answer I can proffer is “It beats me.” Obviously, many investors will not be satisfied with that answer. And that is perfectly OK by me. As a proud graduate of “The School of Whatever Works” I tend to value “consistency” more than I do cause and effect. Not everyone is wired that way and that’s OK.

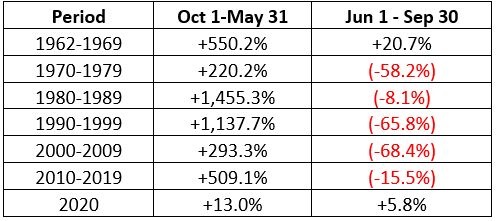

Speaking of consistency, for what it is worth Figure 4 displays decade-by-decade results for the Oct-May period versus the Jun-Sep period.

Figure 4 – DIS decade-by-decade

The key things to note are that:

*The Oct-May period showed a pretty substantial gain during each of the 6 previous decades.

*The Jun-Sep period showed a gain during the 60’s but lost money in every subsequent decade

(Note 2020 results through 12/18 are included in the table but are not a part of the commentary above).

Summary

Clearly the Oct-May period has been pretty “magical” for DIS stock investors for a long time. Will this continue to be the case in the future? Ah, there’s the rub. And as always, I must repeat once again my stock answer of “It beat’s me.”

But the real point is that in the long run investment success has a lot to do with finding and “edge” and exploiting it repeatedly. Or as I like to say:

“Opportunity is where you find it.”

Jay Kaeppel

Disclaimer: The information, opinions and ideas expressed herein are for informational and educational purposes only and are based on research conducted and presented solely by the author. The information presented represents the views of the author only and does not constitute a complete description of any investment service. In addition, nothing presented herein should be construed as investment advice, as an advertisement or offering of investment advisory services, or as an offer to sell or a solicitation to buy any security. The data presented herein were obtained from various third-party sources. While the data is believed to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Past performance is no guarantee of future results. There is risk of loss in all trading. Back tested performance does not represent actual performance and should not be interpreted as an indication of such performance. Also, back tested performance results have certain inherent limitations and differs from actual performance because it is achieved with the benefit of hindsight.

Well that got ugly quick. For the record, if you have been in the markets for any length of time you have seen this kind of action plenty of times. An index, or stock, or commodity or whatever, trends and trends and trend steadily and relentlessly higher over a period of time. And just when it seems like its going to last forever – BAM. It gives back all or much of its recent rally gains very quickly. Welcome to the exciting world of investing.

I make no claims of “calling the top” – because I never have actually (correctly) called one and I don’t expect that I ever will. But having written Part I and Part IIof articles titled “Please Take a Moment to Locate the Nearest Exit” in the last week, I was probably one of the least surprised people at what transpired in the stock market in the last few sessions.

Of course the question on everyone’s lips – as always in this type of panic or near panic situation – is, “where to from here?” And folks if I knew the answer, I swear I would tell you. But like everyone else, I can only assess the situation, formulate a plan of action – or inaction, as the case may be – and act accordingly. But some random thoughts:

*Long periods of relative calm followed by extreme drops are more often than not followed by periods of volatility. So, look for a sharp rebound for at least a few days followed by another downdraft and so on and so forth, until either:

a) The market bottoms out and resumes an uptrend

b) The major indexes (think Dow, S&P 500, Nasdaq 100, Russell 2000) drop below their 200-day moving averages. As of the close on 2/25 both the Dow and the Russell 2000 were below their 200-day moving average. That would set up another a) or b) scenario.

If the major indexes break below their long-term moving averages it will either:

a) End up being a whipsaw – i.e., the market reverses quickly to the upside

b) Or will be a sign of more serious trouble

The main point is that you should be paying close attention in the days and weeks ahead to the indexes in Figure 1.

One reason for potential optimism is that the two-month period of March and April has historically been one of the more favorable two-month periods on an annual basis. Figure 2 displays the cumulative price gain achieved by the S&P 500 Index ONLY during March and April every year since 1945. The long-term trend is unmistakable, but year-to-year results can of course, vary greatly.

Figure 2 – S&P 500 cumulative price gain March-April ONLY (1945-2019)

For the record:

S&P 500 March-April

Result

Number of times UP

55 (73%)

Number of times DOWN

20 (27%)

Average UP%

+5.0%

Average DOWN%

(-3.4%)

Figure 3 – Facts and Figures

Will March and April bail us out? Here’s hoping.

As an aside, this strategy is having a great week so far.

Jay Kaeppel

Disclaimer: The information, opinions and ideas expressed herein are for informational and educational purposes only and are based on research conducted and presented solely by the author. The information presented does not represent the views of the author only and does not constitute a complete description of any investment service. In addition, nothing presented herein should be construed as investment advice, as an advertisement or offering of investment advisory services, or as an offer to sell or a solicitation to buy any security. The data presented herein were obtained from various third-party sources. While the data is believed to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Past performance is no guarantee of future results. There is risk of loss in all trading. Back tested performance does not represent actual performance and should not be interpreted as an indication of such performance. Also, back tested performance results have certain inherent limitations and differs from actual performance because it is achieved with the benefit of hindsight.

I’ve been seeing a number of panicked missives lately regarding the retailing sector. They typically go something like this:

“Despite new highs for most of the major market indexes, the retailing sector has been struggling – and in some cases hit hard – therefore it is clearly (paraphrasing here) THE END OF THE WORLD AS WE KNOW IT, AHHHHHHHHHHHHH……………………..”

Or something along those lines. And the truth is that they may be right. But as it turns out, with the retailing sector it is typically more a question of “when” and not “what” (or even WTF

Recent Results

The concerns alluded to above are understandable given recent results in certain segments of the retailing sector. Figure 1 displays the stock price action for four major retailers. It isn’t pretty.

(click to enlarge)

Figure 1 – Major retailers taking a hit (Chart courtesy WinWayTradingExpert)

So if major retailers are performing poorly one can certainly see why someone might extrapolate this to conclude that the economy is not firing on all cylinders and that the recent rally to new highs by the major averages is just a mirage. And again, that opinion may ultimately prove to be correct this time around.

But before swearing off of retailing stocks, consider the following.

Retailers – When not What

For our test we will use monthly total return data for the Fidelity Select Retailing sector fund (ticker FSRPX). Figure 2 displays the growth of $1,000 invested in FSRPX only during the months of:

*February, March, April, May, November, December

Figure 2 – Growth of $1,000 invested in ticker FSRPX only during the “favorable” months since 1986

For the record:

*An initial $1,000 grew to $50,274, or +4,927% (this test does not include any interest earned during the months out of FSRPX).

*# of years showing a net gain = 27

*# of years showing a net loss = 4

*Average UP year = +17.0%

*Average DOWN year = (-3.4%)

*Maximum UP Year = +50.0% (1990)

*Maximum DOWN Year = (-5.9%) (1994)

The Year-by-Year Results appear in Figure 3

Year

% +(-)

1986

26.2

1987

15.8

1988

12.2

1989

16.9

1990

50.0

1991

45.5

1992

8.0

1993

4.6

1994

(5.9)

1995

3.0

1996

26.1

1997

18.1

1998

45.7

1999

4.0

2000

1.8

2001

12.5

2002

(0.1)

2003

18.5

2004

11.3

2005

10.3

2006

0.1

2007

(2.8)

2008

(4.7)

2009

44.9

2010

24.5

2011

4.6

2012

10.8

2013

16.6

2014

11.5

2015

6.1

2016

9.2

Figure 3 – Year-by-Year Results for “Favorable” Months since 1986

The Rest of the Year

If for some reason you had decided to skip the months above and hold FSRPX only during all of the other months of the year, your results appear in Figure 4.

Figure 4 – Growth of $1,000 invested in ticker FSRPX only during the “unfavorable” months since 1986

For the record:

*An initial $1,000 grew to $1,037, or +3.7% (this test does not include any interest earned during the months out of FSRPX).

Summary

Is the retailing sector guaranteed to generate a gain during our “favorable” months in 2017? Not at all. Still, given that retailing is presently beaten down a bit and the fact that the worst full year loss during the favorable months was -5.9%, it may be time to think about taking a look (although – as always, and for the record – I am not “recommending” retailing stocks, only pointing out the historical trends).

Still, as the old saying goes, the results below are what we “quantitative types” refer to as “statistically significant”.

If you follow jay Kaeppel’s posts in this blog, you’ll know that he’s the master of research on all things seasonal. This past week he posted a seasonal article on energy using FSESX – Fidelity Select Energy Services. Previously he had noted the bullish tendency for ticker FSESX during the months of February, March and April. In his follow up piece, he added one more “favorable” month and then also looked at a 6-month “unfavorable” period. The article is included at the end of this post so you can see the results.As Mutual funds are not for everyone, we went in search of alternative tickers that could closely match FSESX in performance characteristics. Using WinWay Matchmaker we compared the price action of FSESX against our universe of stocks and ETFs looking for a match.

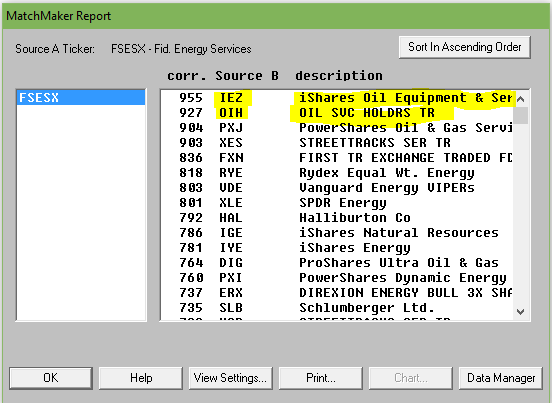

Matchmaker uses Spearman Rank Correlation analysis to identify a close match to FSESX. The closer the result to 1000, the higher the correlation. Anything over 950 is a very close match. Here’s the results.

Figure 1. MatchMaker correlation for last 4 years – FSESX vs stocks and ETFs

The ETF IEZ – iShares Oil and Equipment & Services showed a very high correlation over the 4 years we tested. OIH – Oil Service Holders, another ETF, also showed high correlation.

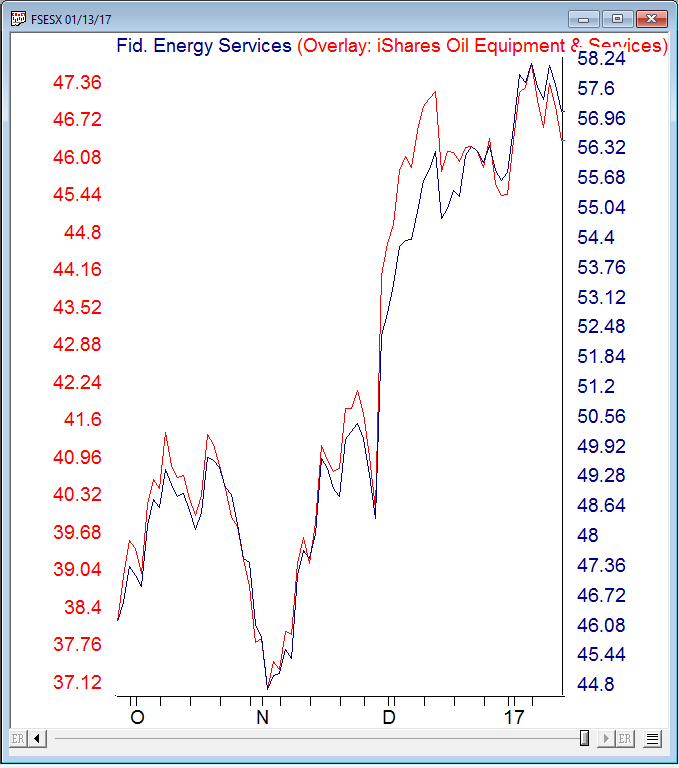

Here’s a WinWay overlay chart of recent daily price action comparing FSESX vs IEZ.

Figure 2. Recent daily price action comparing FSESX vs IEZ.

IEZ appears to be a good surrogate for FSESX at least over the last 4 years.

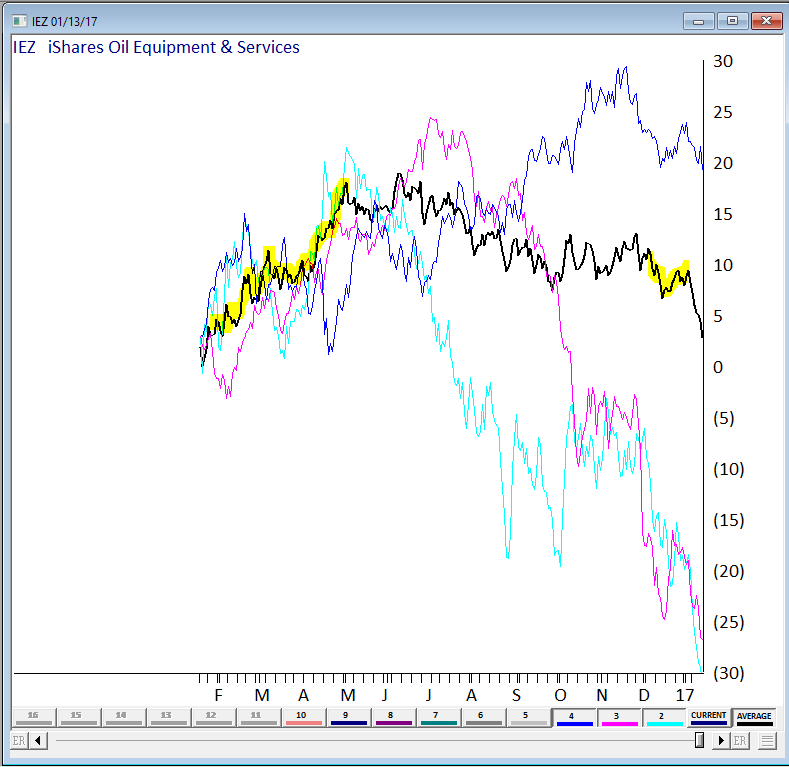

We also wanted a visual of the seasonal pattern in action. Fortunately we have a tool still in development at WinWay that’s just right for this. Basically it provides a price comparison of ‘x’ numbers of years of the same ticker overlaid on each other.

Here’s 3 of the last 4 years on IEZ, the average of the years displayed is in black. We highlighted the Feb, Mar, Apr and Dec in yellow. We could have included more years but for illustration purposes it was easier to show the 3 years (the chart gets busy with too many lines on it!)

Figure 3 – IEZ seasonal chart (beta) for 3 years with average.

The Feb, Mar, Apr period has a definite bullish tendency, the Dec period does Ok too. You’ll notice the tendency for IEZ to fall sharply in January. Conclusion? IEZ is a reasonable surrogate for FSESX if you’re contemplating this seasonal move.

The article this follow up is based upon is by Jay Kaeppel and is included below. Jay is Chief Market Analyst at JayOnTheMarkets.com and TradingExpert Pro client. http://jayonthemarkets.com/

If you are looking for a market sector with some serious seasonal trends, look no further than the energy sector. Previously I had noted the bullish tendency for ticker FSESX during the months of February, March and April. In this piece, we will add one more “favorable” month and then also look at a 6-month “unfavorable” period.

For the record, the information that follows is not being recommended as a standalone strategy. It is presented simply to make you aware of certain long-term trends that have been very persistently bullish (or bearish as the case may be) in the energy sector.

4 Favorable Months

*The four “favorable” months for our test are February, March, April and December

Figure 1 displays the growth of $1,000 invested in ticker FSESX only during these four months every year since 1986 versus simply buying-and-holding ticker FSESX.

Figure 1 – Growth of $1,000 invested in FSESX only during Feb, Mar, Apr, Dec every year since 1986

Starting in 1986, an initial $1,000 investment grew to $76,019 (or +7,500%) versus $10,237 (or 923%) using a buy-and-hold strategy.

6 Unfavorable Months

The six “Unfavorable” months are June, July, August, September, October and November.

First the “positive” news:

*This 6-month period has managed to show a gain 14 times in 31 years – so by no means should you consider this period a “sure thing” loser

*During 4 separate years – 1997, 2003, 2004 and 2010 – the “unfavorable” months registered a cumulative gain in excess of +30%.

Doesn’t sound all that “unfavorable” so far does it? But here’s the catch: Despite the occasional 30%or more gain, it is fair to refer to this 6-month period as “unfavorable” as the cumulative long-term results of buying and holding FSESX during these months has been nothing short of devastating.

Figure 2 displays the growth of $1,000 invested in ticker FSESX only between the end of May and the end of November every year starting in 1986.

Figure 2 – Growth of $1,000 invested in FSESX only during June through November every year since 1986

Starting in 1986, an initial $1,000 investment declined to just $82, or a cumulative loss of -91.8%

Figure 3 displays some comparative data between favorable and unfavorable periods as well as using a Buy-and-Hold strategy.

Measure

Buy-and-Hold

4 Favorable Months

6 Unfavorable Months

Average Annual % +(-)

12.8

16.5

(-4.2)

Median Annual % +(-)

8.7

15.5

(-1.8)

Standard Deviation

33.4

20.1

24.6

# Years UP

18

26

14

# Years DOWN

13

5

17

Worst Year

(-55.4) 2008

(-7.6) 1994

(-62.8) 2008

$1,000 becomes

$10,237

$76,019

$82

Cumulative % +(-)

+923%

+7,500%

(-92%)

Figure 3 – Comparative Results

Figure 4 displays the year-to-year results for a Buy-and-Hold approach versus holding only during the 4 “favorable” months or the “Unfavorable” 6 months.

Year

All 12 months % +(-)

4 Favorable % +(-)

6 Unfavorable % +(-)

1986

(8.9)

(5.2)

(9.2)

1987

(20.7)

22.9

(40.1)

1988

(4.2)

22.8

(16.3)

1989

50.3

27.1

16.2

1990

8.7

4.9

(11.2)

1991

(19.9)

4.1

(25.0)

1992

4.9

(1.6)

(1.3)

1993

16.4

24.5

(10.7)

1994

(0.5)

(7.6)

3.1

1995

40.0

33.7

2.0

1996

45.9

22.5

20.8

1997

43.9

(4.9)

32.9

1998

(41.4)

26.5

(50.5)

1999

80.9

74.1

7.5

2000

51.7

77.6

(21.1)

2001

(22.4)

20.8

(32.4)

2002

2.2

26.2

(18.0)

2003

13.1

15.5

(16.0)

2004

26.2

1.2

30.2

2005

47.4

4.8

34.0

2006

(9.1)

(4.1)

(1.8)

2007

58.3

25.6

16.7

2008

(55.4)

10.5

(62.8)

2009

60.4

24.5

9.6

2010

31.7

21.6

33.7

2011

(18.5)

3.1

(16.8)

2012

(3.9)

0.7

9.6

2013

14.1

0.3

11.5

2014

(19.5)

7.2

(26.7)

2015

(19.7)

2.9

(17.9)

2016

44.2

28.4

20.1

Figure 4 – Yearly % +(-) for Buy-and-Hold versus 4 Favorable Months versus 6 Unfavorable Months

Summary

There is no guarantee from year-to-year results of buying and holding ticker FSESX during the “Favorable 4” months will show a gain and/or outperform the “Unfavorable 6” months. And there is by no means any guarantee that the “Unfavorable 6” will show a loss during any given year (note that 2016 saw the Unfavorable 6 generate a cumulative gain of +20.1%!). So just remember that we are talking about some very long-term trends here.

Still, most investors can discern the difference between:

*Favorable 4 months gain = +7,500%

*Unfavorable 6 months loss = (-92%)

This type of difference is what we “quantitative types” refer to as “statistically significant.”

Recently Jay Kaeppel of Jay On The Markets posted an update on the Seasonal Bonds Strategy usingTMF. The gist of the strategy is straightforward, “Long TMF on the last 5 day of each month” I’ve posted the article below. Here’s a seasonal chart of the last 3 years with the average of the 3 years (black line). I colored the last 5 trading days of the average line in yellow to see what Jay was referring to. 8 of the 12 months were positive, 2 flat and 2 negative. Looks pretty good. At the bottom of the page you can see the returns this strategy yields. BTW this Chart type, known as a seasonality chart will be included in the next AIQ TradingExpert Pro release this fall (OK marketing bit over)

So of course the bond market rewarded my “brilliance” with a swift kick in the you know where in the months of March and April 2015 and especially in August 2015.

This would typically be enough to cause many people to go, “Well that guy’s and idiot” and to move on. But fortunately in this case, the market is a marathon and not a sprint.

Update

Figure 1 displays the results generated by:

*Holding long 1 t-bond futures contract ONLY for the last 5 days of each month since 12/30/1983

*Holding long 1 t-bond futures contract during all other days since 12/30/1983

Figure 1 – Long 1 t-bond futures contract ONLY during last 5 trading days of month (blue) versus long 1 t-bond futures contract on all other days (red); 12/31/1983-8/12/2016

The results sort of speak for themselves.

After I wrote about my aggressive TMF strategy, TMF (of course) got hit very hard (as triple leveraged ETFs will do from time to time, hence the use of the words “aggressive” and “risky”), in March 2015 (-4.5%), April 2015 (-5.3%) and especially in August 2015 (-11.5%).

Still, as you can see in Figure 2, things have rebounded nicely since (hmmm, maybe I should be worried).

Figure 2– Growth of $1,000 Long ETF ticker TMF ONLY during last 5 trading days of month (blue) versus long TMF all other days; (red); 12/9/2009-8/12/2016

So far the “Long TMF on the last 5 day of each month” strategy is up +31.8% for the year in 2016.

Year

Last 5 TDM Long TMF

2009*

+12.9%

2010

+33.4%

2011

+15.2%

2012

+35.7%

2013

+6.7%

2014

+45.7%

2015

+6.8%

2016**

+31.8%

*-Starting 4/16/2009 when TMF started trading

**-Through 8/12/2016

Summary

So did this odd little strategy “weather the storm” and “take the market’s best shot” in 2015 and now it is “smooth sailing”? Probably not. Make no mistake – this is a strategy that entails a great deal of risk. Still, for aggressive traders looking for an “edge”, it might be worth a closer look.